When you’re managing significant wealth, the single most important decision you'll make is who you trust for advice. An independent financial advisor works for you, not a massive parent company. This gives them the freedom to shop the entire market to find the absolute best financial products and strategies for your specific situation.

That independence is the very foundation of objective, client-first guidance.

Why an Independent Financial Advisor Is a Smarter Choice

Choosing a financial advisor is about more than just picking stocks; it’s about finding a partner to help protect and grow your legacy. The structure of that partnership is what makes all the difference.

Think of it like this: an advisor at a big Wall Street firm is a bit like a car salesperson who can only sell you one brand. They might have good options, but they can't show you anything else on the market.

An independent advisor, in contrast, is more like a personal wealth architect. They aren't tied to any one company's products. This freedom means they can build your financial plan using the best “materials”—be it investment tools, insurance policies, or planning software—from anywhere and everywhere.

The Power of Unbiased Advice

This fundamental difference is what allows for truly unbiased advice. Since an independent advisor doesn't have a boss pushing them to meet sales quotas for in-house products, their recommendations are guided by one thing and one thing only: what is best for you. This alignment is absolutely critical, especially for high-net-worth individuals whose financial lives are often complex and interconnected.

Their role boils down to a few key things:

- Giving you an objective, clear-eyed analysis of your entire financial world.

- Building custom-tailored strategies, free from corporate restrictions or mandates.

- Acting as a fiduciary—a crucial legal standard we’ll get into next.

The real advantage of an independent advisor is their ability to sit on the same side of the table as you. Their success is tied directly to your success, not to how much of a certain product they can sell.

A Foundation Built on Fiduciary Duty

This client-first philosophy is legally formalized through what’s known as a fiduciary duty. An independent advisor who operates as a fiduciary is legally and ethically required to act in your best interest, always. No exceptions.

This creates a relationship built on trust and complete transparency, which is the only way to achieve real long-term financial security. Understanding the nuances of investing with a financial advisor and their legal obligations is the first step toward making a confident decision for your wealth. It's a distinction that sets the stage for a far more secure and prosperous financial future.

What Are the Different Types of Financial Advisors?

When you start looking for financial advice, it can feel like you've stepped into a world of confusing titles and unclear loyalties. The truth is, not all financial advisors are created equal. Who you choose to work with can dramatically change the advice you get, so it's critical to understand the different models out there.

You'll generally run into three main types: independent advisors, wirehouse advisors, and insurance agents. Let's break down what makes each one different.

An independent financial advisor, who typically operates as a Registered Investment Advisor (RIA), runs their own shop. This independence is their superpower. It means they aren't tied to any single company's products and can pull from the entire universe of investment options to build a plan that's truly right for you. Their loyalty is to their client, plain and simple.

On the other side of the coin, you have wirehouse advisors. These are the folks who work for the big-name brokerage firms you see on Wall Street. They have massive resources behind them, but they're also employees. This means they're often limited to selling their company's own investment products, which can create a conflict of interest. Are they recommending a fund because it's the best for you, or because it helps them meet a sales quota?

A Spectrum of Advice: Who Do They Really Work For?

At the end of the day, the biggest difference comes down to one question: Who does the advisor answer to? Is it you, the client, or is it their employer? This single distinction affects everything, from their legal duties to the kind of advice they can offer.

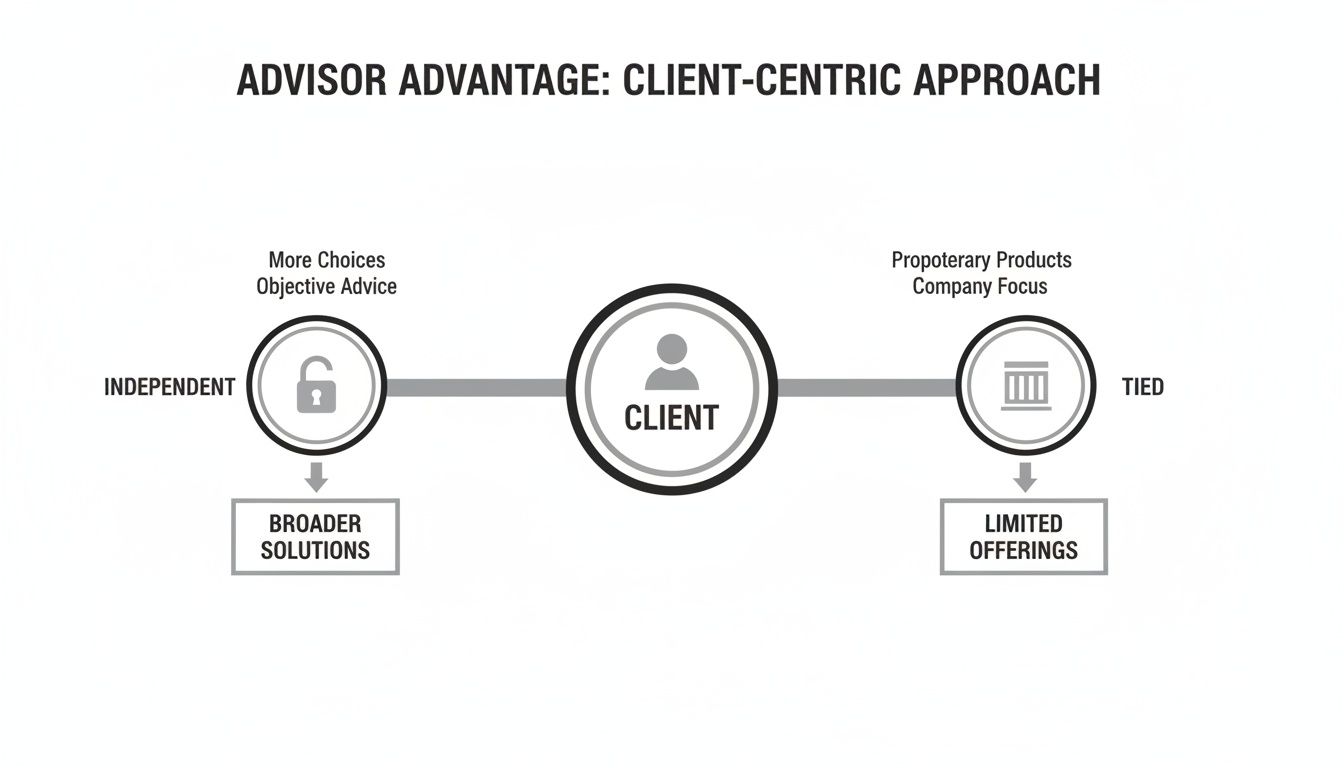

This diagram really clarifies the divide between an advisor who is tied to a company and one who is truly independent.

As you can see, an independent advisor has the freedom to explore a much wider range of solutions. A tied advisor, however, is stuck playing in a much smaller sandbox filled only with their company's proprietary toys.

Finally, there are insurance agents. They play an important role, but their focus is narrow—they specialize in insurance and annuity products. Their pay is almost always based on commissions from the policies they sell. While you might need their expertise for a specific part of your financial plan, they aren't set up to provide holistic, comprehensive wealth management.

A Head-to-Head Comparison of Advisor Models

To really grasp the differences, it helps to see these models laid out side-by-side. How an advisor is structured directly impacts their relationship with you, the products they can recommend, and the legal standard they're held to. Getting this right is absolutely essential if you're looking for truly objective advice.

This table cuts through the noise and compares the core attributes of each advisor type.

Ultimately, the advisor's business model sets the stage for everything else. An independent financial advisor is structured from the ground up to be your partner, building strategies that are aligned only with your best interests. For anyone managing significant wealth, that client-first focus and flexibility isn't just a benefit—it's a necessity.

The Fiduciary Standard: Why It’s the Gold Standard for Your Portfolio

You’ve probably heard the term fiduciary duty thrown around, but it’s so much more than financial jargon. It's a legal and ethical pledge that completely changes the game. This is the critical difference between hiring a professional who is legally required to act in your best interest and working with someone who is essentially just selling you a product.

An independent financial advisor who is a fiduciary must put your financial well-being first. Always. It’s not just a nice idea—it’s a legal mandate.

This commitment means every single recommendation, from picking an investment to mapping out your estate, is made with your goals in mind, not to pad the advisor’s commission. For high-net-worth families with complex financial lives, this alignment is the absolute foundation of a trusted, long-term partnership.

What Fiduciary Duty Looks Like in the Real World

The fiduciary standard isn't some lofty, abstract ideal. It has very real, tangible effects on how your money is managed and your wealth is protected.

Here’s what it means for you in practical terms:

- Total Transparency: A fiduciary has to tell you exactly how they get paid and disclose any potential conflicts of interest. No hidden fees, no surprises.

- Unbiased Advice: Since they aren’t pushed to sell specific company products, their recommendations are based purely on what’s best for your unique situation.

- A Duty of Loyalty and Care: Your advisor must act with the skill and diligence of a prudent professional, ensuring your portfolio is managed responsibly.

Think about it like your relationship with a doctor. You trust them to use their expertise for your best possible outcome, free from any competing agenda. The fiduciary standard brings that exact same level of professional integrity to your finances.

The Growing Demand for True Fiduciary Care

This shift toward fiduciary advice isn't a small trend; it's a massive sea change in the wealth management industry. High-net-worth investors are actively seeking out advisors who are legally bound to put them first.

The independent advisor space is booming. In fact, Cerulli Associates projects a 4% compound annual growth rate (CAGR) for independent RIAs through 2028, a pace that leaves other channels in the dust. This surge is part of a larger movement where RIAs now manage a staggering $125 trillion in assets, cementing their role as the go-to for clients who demand fiduciary-level care.

At its core, the fiduciary standard ensures that the person managing your wealth is sitting on the same side of the table as you. Their success is directly tied to your success.

This alignment is everything. It cuts through the noise and provides the peace of mind that comes from knowing your advisor is truly in your corner. As you weigh your options, understanding the differences between a fiduciary financial advisor vs. a fee-only one can offer even more clarity. For anyone with significant assets, choosing an advisor who operates under this high standard isn’t just a good idea—it’s essential.

Comprehensive Services for High-Net-Worth Needs

When you have significant wealth, your financial life isn't just a bigger version of everyone else's—it's fundamentally more complex. You’re not just managing investments; you're juggling business interests, real estate, legacy planning, and philanthropic goals. An independent financial advisor steps in to act as the quarterback for this entire landscape, offering specialized, holistic services that make all the pieces work together.

This level of coordination is about much more than just growing your portfolio. It’s about protecting what you’ve built, making it as tax-efficient as possible, and ensuring it can support your family and your vision for generations.

Beyond Investment Management

While picking the right investments is crucial, a top-tier independent firm offers a much wider range of services. The real goal is to get away from fragmented advice, where your CPA, attorney, and investment manager aren't necessarily talking to each other. Instead, you get a single, unified strategy.

This integrated approach is the key to navigating the unique challenges and opportunities that come with substantial wealth.

Key areas of specialization often include:

- Advanced Tax Planning: Proactively finding ways to minimize taxes across your entire financial life, from your investments and income to your estate.

- Multi-Generational Estate Planning: Crafting sophisticated plans that use trusts, gifting strategies, and business succession plans to preserve wealth and secure your legacy for your children and grandchildren.

- Concentrated Stock Management: Helping executives or early employees with a large amount of stock in a single company to diversify that risk without creating a huge tax bill.

- Strategic Philanthropy: Structuring your charitable giving through tools like donor-advised funds or private foundations, so you can make a meaningful impact while aligning your wealth with your values.

For many high-net-worth clients, comprehensive planning also touches on asset protection strategies, such as figuring out when to consider a prenuptial agreement.

Bespoke Planning for Niche Clientele

The financial needs of a professional athlete are completely different from those of a tech entrepreneur who just sold their company. The best independent advisors understand this and build customized frameworks for specific types of clients.

Take an advisor working with professional athletes, for example. They have to plan for a very high but often short earning window. That means strict budgeting, smart long-term investing, and strong asset protection to make sure that money lasts a lifetime.

An independent firm’s true value is in acting as your personal CFO. They coordinate with your whole team—attorneys, accountants, insurance agents—to make sure every single financial decision aligns with your bigger goals.

Likewise, entrepreneurs need specific advice on managing the wealth tied up in their business, planning for an eventual sale, and diversifying their personal assets away from the company they poured everything into.

The Family Office Model

For ultra-high-net-worth families, this holistic approach often evolves into what's known as a family office. Think of it as having a dedicated in-house team to manage every aspect of the family's financial affairs, from investments and taxes to philanthropy and family governance.

An independent advisor is perfectly positioned to deliver these comprehensive services, providing the strategic oversight needed to protect and grow a significant legacy. This is especially true for those navigating the complexities of a https://www.commonsllc.com/insights/family-office-services. Ultimately, they provide the cohesive vision required to manage a complex financial world effectively.

How to Choose the Right Independent Financial Advisor

Choosing someone to guide your financial future is a major decision—right up there with the biggest life choices you’ll make. This isn't just about finding someone who's good with numbers; it's about finding a partner you can trust with your legacy. The process requires a deliberate, thoughtful approach to find a professional whose expertise, philosophy, and even personality click with your own.

When you start this search, you're taking the reins of your financial life. You're moving past generic advice and seeking a real partnership. The goal is to do your homework with confidence, ensuring the advisor you select can truly handle your financial complexity and is in it for the long haul.

Starting Your Search and Creating a Shortlist

The best way to start is by casting a wide, but smart, net. Ask people you already trust who are in a similar financial boat—think of your CPA, your estate planning attorney, or even business partners. Personal referrals from your inner circle often yield the most solid leads.

From there, broaden your search using online tools from professional organizations. Both the National Association of Personal Financial Advisors (NAPFA) and the CFP Board have great online directories where you can find credentialed, fee-only advisors. The aim here is simple: build a shortlist of three to five advisors who look like a good match on paper.

Key Questions to Ask During Consultations

The initial meeting is your chance to really interview a potential advisor. This is where you go beyond their slick website and see if there’s a genuine connection. Having a list of questions ready helps keep the conversation on track and makes sure you get the details you need to make a smart choice.

Make sure your questions hit these key areas:

- Credentials and Expertise: "What professional designations do you hold, like CFP® or CFA®, and how do they benefit me? Have you worked with clients in a situation similar to mine before?"

- Investment Philosophy: "Could you walk me through your core investment philosophy? How do you handle risk, especially when the market gets rocky?"

- Fee Structure: "How do you get paid? Are you fee-only, and will you sign a statement confirming you'll act as my fiduciary at all times?"

- Client Experience: "What can I expect in terms of communication? How often will we meet, and who will be my main contact person at your firm?"

It's also worth considering how efficiently an advisor runs their practice. For a closer look at the types of services utilized by financial advisors to streamline their operations and better serve clients, this resource offers some good insights.

Recognizing Red Flags and Performing Due Diligence

Knowing what to look for is only half the battle; you also need to know what to look out for. A good advisor will be transparent, patient, and clear. If someone feels evasive or starts using high-pressure sales tactics, your internal alarm bells should be ringing.

A huge red flag is any hesitation to talk about fees or put their fiduciary commitment in writing. A true professional will welcome these questions as a chance to build trust, not dodge them.

Before you sign anything, do a background check. It’s a non-negotiable step. Use FINRA's BrokerCheck tool and the SEC's Investment Adviser Public Disclosure (IAPD) website to verify their credentials and see if they have any disciplinary history. This adds a crucial layer of security to your decision.

The need for thorough vetting is more important than ever. The financial advisory world is facing a bit of a talent crunch; a J.D. Power study revealed that 46% of advisors are within 10 years of retirement. This makes finding a stable, experienced advisor for a lasting partnership absolutely critical.

A Partnership with Commons Capital

Throughout this guide, we've walked through what it really means to work with an independent financial advisor—someone legally and ethically bound to put your interests first. We’ve covered how that fiduciary promise, combined with truly comprehensive services, creates the right environment for managing and growing significant wealth.

At Commons Capital, we live and breathe these principles. Our entire firm was built from the ground up on this client-first, independent model. It’s a structure designed specifically for the complex financial lives of high-net-worth individuals, families, and professionals in the sports and entertainment worlds. We’ve found that the best financial outcomes spring from a genuine partnership.

Our Fiduciary Commitment to You

As an independent firm, our loyalty is to one party and one party only: you. We are fiduciaries, which means every piece of advice and every recommendation we make is based purely on what’s best for your specific situation. This isn’t just a nice-to-have philosophy; it’s our legal and ethical duty.

We believe that objective advice, free from the conflicts of interest found in traditional brokerage firms, is the only way to build a relationship based on unwavering trust. Our success is measured by your success—period.

This commitment is the bedrock of everything we do.

A Partnership Built for Complex Needs

Managing significant wealth is about so much more than picking investments. It requires a sophisticated, 360-degree strategy that coordinates every piece of your financial puzzle. We act as the central hub for your financial world, making sure everything from your investments to your estate plan works in perfect harmony.

We’ve built our services to address the specific hurdles our clients face:

- For High-Net-Worth Families: Our focus is on multi-generational wealth preservation, sophisticated estate planning, and strategic philanthropy designed to protect and extend your legacy.

- For Sports and Entertainment Professionals: We understand the unique career arcs. We design financial plans that account for high, but often condensed, earning windows, with a sharp focus on long-term security.

- For Entrepreneurs and Business Owners: We provide seasoned guidance on managing concentrated stock positions, planning for major liquidity events, and seamlessly integrating your personal and business finances.

If you’re looking for a financial partnership built on trust and designed for your specific goals, we invite you to start a conversation. Schedule a consultation with our team, and let's explore how our independent, client-first approach can help you build the future you envision.

Your Questions Answered: Working With an Independent Advisor

Stepping into the world of wealth management can feel overwhelming, and it's natural to have questions, especially when you’re thinking about partnering with an independent financial advisor. We've put together some straightforward answers to the questions we hear most often.

Think of this as a conversation starter. We want to clear up any confusion you might have so you can make your next move with total confidence. Let’s dive into everything from account minimums to what those first few meetings actually feel like.

Is There a Minimum Account Size to Work With an Independent Firm?

This is probably the number one question we get, and the honest answer is: it depends. Some independent advisors are happy to work with clients at any stage of their financial journey and have no set minimum. Others, especially those focusing on complex services for high-net-worth families, might look for $500,000 or more in investable assets.

Don't think of these minimums as a velvet rope. They’re really about making sure the firm is a good fit for your needs. A firm that specializes in intricate tax and estate planning, for example, sets a higher minimum to ensure their clients have a level of complexity that truly benefits from that deep expertise.

How Do You Specifically Help Business Owners?

If you’re an entrepreneur, you know that your personal and business finances aren’t just connected—they’re completely tangled together. An independent advisor's job is to act as a financial co-pilot, helping you make sense of that beautiful mess.

We see our role as a strategic partner in a few critical areas:

- Planning Your Next Chapter: We help you build a real, actionable plan for your exit, whether that means selling the company or handing it down to the next generation, all while keeping taxes in mind.

- Managing Your Risk: It's common for a business owner's entire net worth to be tied up in their company. We work on strategies to carefully diversify your wealth so that all your eggs aren't in one basket.

- Connecting the Dots: We help you create a single, unified financial strategy that aligns your business cash flow, company retirement plans (like a 401(k) or SEP IRA), and your personal investment goals.

How Do Independent Advisors Get Paid?

One of the best things about the independent model is the clarity around fees. You should never have to guess how your advisor is being compensated.

The most common approach is a fee based on Assets Under Management (AUM). It’s a simple annual percentage—say, 1%—of the total assets the advisor is managing for you. This structure is powerful because it puts you and your advisor on the same side of the table. When your portfolio does well, everyone wins. Some advisors might also offer a flat annual retainer or charge a project-based fee for a specific financial plan.

The most important thing to know is that independent advisors are almost always fee-only or fee-based. This means their income doesn't rely on commissions from selling you a particular product. It’s a model built to minimize conflicts of interest and put their legal fiduciary duty to you first.

What Should I Expect When I First Get Started?

The first few steps are all about getting to know each other. It’s less of a sales pitch and more of a two-way interview to see if we're the right fit for a long-term relationship.

Here’s how it usually plays out:

- The First Chat: This is a relaxed, no-pressure conversation where we talk about your goals, what's keeping you up at night, and what you’re looking for in an advisor. It's your chance to ask us anything.

- The Deep Dive: If it feels like a good fit, we’ll schedule a deeper discovery session. This is where you’ll share the specifics of your financial life so we can see the full picture.

- The Plan Presentation: We take everything we’ve learned and come back to you with a personalized financial plan. We’ll walk you through our recommendations and explain the "why" behind every single one.

- Putting It All in Motion: Once you give the green light, our team gets to work opening accounts, transferring assets, and implementing the strategy we built together.

It's a deliberate and thoughtful process, designed to build a solid foundation of trust right from the very beginning.

At Commons Capital, our independent and fiduciary approach is designed to provide the clarity and confidence you deserve. If you're ready for a financial partnership built on trust and tailored to your unique aspirations, schedule a consultation with us today.