Figuring out how to value your business is far more than a simple calculation; it's a deep-dive analysis into your company's financial health, market position, and future growth potential. The true art lies in blending quantitative data—like revenue and assets—with qualitative factors like brand reputation to arrive at a defensible economic worth. A clear understanding of your business's value is essential for strategic planning, securing financing, or preparing for an exit.

Why Knowing Your Business's Worth Is So Critical

For high-net-worth individuals and families, understanding your company's value is the bedrock of smart financial management. This goes way beyond just prepping for a potential sale. A precise valuation is a strategic tool that sharpens your most critical decisions.

It gives you the clarity you need for effective wealth management, estate planning, and even spotting new opportunities for growth. Without it, you're essentially flying blind into your financial future.

A formal valuation has plenty of practical uses, too. It’s the defensible number you need when you're talking to lenders, trying to attract serious investors, or setting up an employee stock ownership plan (ESOP). It’s also invaluable during major personal milestones, like divorce settlements or building a solid succession plan. Seeing how valuation fits into your long-term goals is a key part of developing a successful business exit strategy.

Before diving into the how, it's crucial to understand the why. A formal valuation isn't just a box-ticking exercise; it’s a strategic necessity driven by specific goals.

Here’s a quick summary of the most common reasons business owners seek a valuation.

Table: Key Reasons for Business Valuation

Each of these scenarios demands a clear, objective assessment of value. Without it, you’re simply guessing.

The Strategic Edge of a Professional Valuation

In today’s complex economic climate, the need for accurate business valuations is exploding. The global market for financial modeling and valuation is expected to jump from USD 7.8 billion in 2025 to USD 15.0 billion by 2032.

This isn't just a random trend. It shows just how vital these precise financial check-ups have become, especially as M&A activity continues to heat up.

A professional valuation does more than just stamp a price tag on your company. It uncovers hidden strengths and shines a light on potential weaknesses. This kind of objective analysis can show you where you can tighten up operations, bolster your market position, and ultimately, grow your company’s value over time.

A business valuation is not merely a snapshot in time. It is a comprehensive diagnostic tool that empowers owners to make smarter, more strategic decisions that protect and grow their most significant asset.

Ultimately, knowing your business's worth gives you leverage and confidence. It doesn't matter if you're at the negotiating table with a buyer, planning your financial legacy, or just checking in on your own progress—a clear, credible valuation is your roadmap. It turns abstract goals into real, actionable strategies, ensuring you’re always operating from a position of strength.

Valuing Future Potential with the Income Approach

When you’re trying to figure out how to value your business, the income approach gives you the most forward-looking perspective. Other methods might get bogged down in past sales or the current value of your assets, but this one cuts right to the chase: a business’s ability to make money in the future.

For any smart investor or potential buyer, that’s really the only thing that matters.

The idea is straightforward. A business is worth the present value of all the cash it's expected to generate down the road. This forces you to put on a buyer's hat and focus on future returns, not just what the company has done historically. We typically do this in one of two ways: the Discounted Cash Flow (DCF) method or the Capitalization of Earnings method.

Unpacking the Discounted Cash Flow Method

The Discounted Cash Flow (DCF) method is the gold standard, especially for businesses with predictable, growing earnings. It's all about projecting future cash flows over a set period—usually 5-10 years—and then discounting them back to what they’re worth today. This is crucial because it accounts for the time value of money. A dollar in your pocket now is worth more than a promise of a dollar next year.

A bulletproof revenue forecast is the engine of a good DCF analysis. If your projections are shaky, the whole valuation falls apart. For a great breakdown of this process, especially if you're running a subscription-based business, Altior & Co. has a fantastic guide on Revenue Forecasting: A B2B SaaS Guide to Predictable Growth.

To run a proper DCF analysis, you need to nail down three key pieces:

- Forecasting Future Cash Flows: This is where you put on your analyst hat. You'll need to create realistic financial projections for revenue, operating costs, and capital expenditures. This isn't guesswork; it requires a deep understanding of your market, your competitive advantages, and your growth strategy.

- Determining a Discount Rate: The discount rate is how you account for risk. It reflects the uncertainty of actually receiving those future cash flows. It’s often based on the Weighted Average Cost of Capital (WACC), which is a blend of a company's cost of equity and debt. A riskier venture demands a higher discount rate, which brings its present value down.

- Calculating Terminal Value: A business doesn't just stop existing after your 10-year forecast. The terminal value is an estimate of the company's worth at the end of that period, assuming it continues to operate. You then discount that value back to the present and add it to your sum.

Remember, strong projections are built on solid ground. This is why having your financial house in order is non-negotiable. Mastering the fundamentals of cash flow management for small business is a prerequisite for any valuation you can stand behind.

The Capitalization of Earnings Method

While DCF is perfect for businesses on the rise, the Capitalization of Earnings method is a much better fit for mature, stable companies with a history of consistent cash flow. I’m talking about the well-established manufacturing firm or the local service business that’s been a community staple for decades.

This method is much simpler than DCF. It takes a single, representative period's earnings (like EBITDA) and divides it by a capitalization rate to arrive at a value.

Valuation = Annual Earnings / Capitalization Rate

The capitalization rate is just the inverse of a valuation multiple. It represents the rate of return an investor would expect for taking on the risk. You find it by taking the discount rate and subtracting the long-term, sustainable growth rate. A lower cap rate—which implies lower risk or higher growth—results in a higher valuation. Simple as that.

Putting It Into Practice with Real Scenarios

Choosing the right income-based method always comes down to the specific business you're looking at.

Let's take a high-growth SaaS company. Its current profits might be tiny, or it might even be losing money because it's pouring cash into acquiring customers. The Capitalization of Earnings method would be a disaster here; it would dramatically undervalue the business. Instead, a DCF analysis is essential. It’s the only way to capture the future potential locked inside its recurring revenue model and growing user base.

Now, picture a different scenario: a family-owned manufacturing business that has reliably grown at 5% a year for the past 20 years. Forecasting some wild, hockey-stick growth would be completely unrealistic. For a business like this, the Capitalization of Earnings method is far more appropriate. You can use a single, representative earnings figure to get a straightforward valuation based on its proven, steady profitability.

The biggest mistake I see people make with the income approach is getting carried away with overly optimistic projections. Your forecasts have to be defensible. Ground them in reality with market data, historical performance, and a clear, actionable strategic plan. At the end of the day, a valuation is only as credible as the assumptions that hold it up.

Benchmarking Against Peers with the Market Approach

While the income approach is all about forecasting the future, the market approach pulls us firmly back into the present. It helps answer the one question every business owner I’ve ever met asks: “So, what are other companies like mine actually selling for?”

At its heart, this method values your company by seeing what similar businesses have recently sold for or what comparable public companies are worth.

Think of it like selling your house. You wouldn’t just pluck a number out of thin air. You’d look at the sale prices of similar homes on your street. This same real-world logic applies to your business, giving your valuation a critical dose of reality.

The whole process hinges on finding relevant comparable companies—or "comps," as we call them. This is where experience really pays off; it's as much an art as it is a science. You have to look past the surface and find businesses that are truly similar where it counts.

Identifying the Right Comparable Companies

Getting the comps right is everything. If you pick the wrong ones, your entire valuation will be built on a shaky foundation. The goal is to create a small, curated group of companies that are a near-perfect mirror of your own.

Here's what I look for when building a list of comps:

- Industry and Niche: You can't compare apples to oranges. A software company is a world away from a manufacturing firm. Even within tech, a B2B SaaS business has a completely different model than a gaming app developer.

- Size: Revenue, employee count, and market position are key. A local, family-owned machine shop just isn't in the same league as a multinational industrial conglomerate.

- Geography: Market dynamics are local. A company in a booming city like Austin will have a different growth trajectory and cost structure than one in a quiet rural town.

- Growth Profile: Are you a high-octane startup or a stable, mature cash cow? The market pays a premium for growth, so comparing the two directly would be a mistake.

Once you’ve put together a solid list of comps, you can start using valuation multiples to connect their value to yours.

Applying Valuation Multiples

Valuation multiples are simply financial ratios that create a standardized way to compare companies, even if they're different sizes. They tie a company's total value back to a core financial metric.

The two workhorses of valuation are:

- Price-to-Earnings (P/E) Ratio: This is the go-to for established, profitable companies. It compares the total value (or stock price) to the company's net earnings.

- EV-to-EBITDA Ratio: This one is more versatile. It compares Enterprise Value (EV) to Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). It’s my preferred multiple for businesses with heavy debt or large capital investments because it gives a much cleaner look at pure operational performance.

The real power of the market approach is that it reflects what actual buyers are willing to pay for businesses like yours, right now. It’s the ultimate reality check for the more theoretical, forward-looking methods.

Let's say you find three private companies in your sector that recently sold for an average of 6x EBITDA. If your own company’s EBITDA is $2 million, you can quickly see that the market might value your business somewhere in the neighborhood of $12 million.

Lessons from the Public Markets

Private company sales data can be tough to come by, but the public markets are an open book. Watching the valuations of giants like Microsoft and Nvidia gives us incredible insight into what the market values, and those trends always trickle down.

For example, look at what happened on July 9, 2025, when Nvidia rocketed past a $4 trillion market cap. Over the past 15 years, U.S. giants like Nvidia and Microsoft have blown past their global peers, thanks to incredible growth and expanding P/E multiples. This has created a massive valuation gap, with international stocks now trading at a 39% discount to the S&P 500. You can get a better feel for these market forces by seeing how the biggest companies are valued.

This matters to your private business. We’re seeing AI-focused tech companies command multiples of 30-50x forward earnings, while a steady manufacturing business might trade for a solid 10-15x EBITDA. Knowing where the broader market is heading helps you craft a believable story for your own valuation.

But a raw multiple is just the start. The final, critical piece is adjusting that number for what makes your business unique. If you have higher growth, a "stickier" customer base, or a rock-star management team, you deserve a premium. On the flip side, things like customer concentration or outdated tech will mean a discount. This is where a simple calculation becomes a truly accurate assessment of what your business is worth.

Getting Real with the Asset-Based Approach

While income and market approaches are great for looking at potential earnings or how you stack up against the competition, the asset-based approach brings the valuation conversation right back down to earth. It answers a simple, powerful question when you’re trying to figure out how to value your business: if we sold off every single thing the company owns today, what would be left in the bank?

This method is all about calculating your company’s Net Asset Value (NAV). You do this by making a meticulous list of every asset, then subtracting every liability. The result is a solid floor for your valuation—a baseline that's absolutely critical in certain situations, like for holding companies with significant real estate or if you’re ever facing a liquidation scenario.

The whole process starts with a deep dive into your balance sheet. You can’t get an accurate number without knowing how to read these documents inside and out. If you need a refresher, our guide on how to analyze financial statements is a great place to start.

The Tangible vs. The Intangible

First things first: you need to build a complete inventory of what you own, and that means separating your assets into two very different buckets. This isn't just about accounting; it's about seeing the full picture of what makes your business valuable.

Tangible assets are the easy part—the physical stuff you can see and touch. Valuing these is usually pretty straightforward. We’re talking about things like:

- Real Estate: The office buildings, warehouses, or land the company owns.

- Equipment and Machinery: Everything from heavy manufacturing equipment and company cars to the laptops on everyone's desks.

- Inventory: All the raw materials, works-in-progress, and finished goods waiting to be sold.

- Cash and Securities: The liquid assets sitting in bank accounts or tied up in short-term investments.

Then there are the intangible assets. These don't have a physical form, but in today's economy, they can be unbelievably valuable. Quantifying them is definitely trickier, but ignoring them means you're missing a huge piece of the puzzle.

I've seen it time and time again: ignoring intangible assets is one of the biggest mistakes business owners make during valuation. A powerful brand or a game-changing patent can easily be worth more than all the physical equipment a company owns combined.

Don't forget to identify and place a value on these key intangibles:

- Intellectual Property: Think patents, trademarks, copyrights, and any proprietary software you've developed.

- Brand Recognition: This is the value of your company's name and reputation in the market.

- Customer Lists and Relationships: That loyal customer base and the contracts you've secured are a major asset.

- Goodwill: The premium value tied to your company’s established operations and standing.

Two Sides of the Same Coin: Going Concern vs. Liquidation

The reason you're doing the valuation completely changes how you look at these assets. The asset-based approach can be applied in two very different ways, and each one tells a unique story about what your business is worth.

1. Going Concern ValuationThis is the optimistic view. It assumes the business will keep running for the foreseeable future. Here, assets are valued at their "fair market value," which is what they’d fetch if sold as part of a healthy, operating company. This approach gets that assets working together in a functioning business are almost always worth more than if they were sold off one by one.

2. Liquidation ValuationThis is the "fire sale" scenario. It calculates the net cash you’d get if you shut the doors and sold everything off as quickly as possible. This number is almost always lower than the going concern value because it strips away all the synergistic value of an operating business. Think of it as the absolute rock-bottom baseline for your company's worth.

For a healthy, growing company, the going concern approach is what matters most. But the liquidation value is essential for lenders who are sizing up collateral or for shareholders of a distressed company staring down bankruptcy. Your balance sheet is the map, and understanding the difference between these two destinations ensures you end up with a valuation that makes sense for your specific circumstances.

Bringing It All Together for a Final Valuation

You’ve run the numbers using three different lenses—income, market, and asset-based. Now comes the real art of valuation: combining these distinct perspectives into a single, defensible number.

Let’s be clear, this isn’t about just averaging the results and calling it a day. That's a rookie mistake. The final step is a thoughtful process of weighing each method based on the DNA of your company, the industry it lives in, and the specific reason you’re doing this valuation in the first place.

Think of it as building a compelling case that justifies your final number, whether you're sitting across the table from a potential buyer, an investor, or your own family for estate planning.

Strategically Weighing Each Method

So, how do you decide which method gets the most weight? It all comes down to the nature of your business. A profitable, fast-growing software company is valued on a completely different basis than an asset-heavy manufacturing firm.

Here’s a quick guide based on what I’ve seen work in the real world:

- For Service-Based or Tech Companies: The Income Approach is almost always king. Buyers aren't purchasing your office furniture; they're buying a stream of future cash flow. A well-constructed Discounted Cash Flow (DCF) analysis will carry the most weight here, with the Market Approach acting as a strong reality check.

- For Asset-Heavy Businesses: If you're in manufacturing, real estate, or distribution, the Asset-Based Approach is your foundation. It sets a critical floor for your valuation. While earnings are still important, the tangible value of your machinery, inventory, and property is a huge piece of the puzzle.

- For Mature, Stable Businesses: Companies with a long, steady track record of profits benefit most from a blended approach. The Market Approach gives you that real-world context of what similar businesses are selling for, while the Capitalization of Earnings method offers a solid, straightforward view based on your profits.

When you're ready to put it all together, understanding the specific business valuation formulas can give you a clear framework. This helps you translate your strategic weighting into a concrete mathematical process.

Valuation Method Weighting by Industry

To make this more tangible, here’s a table showing how you might weigh the different valuation methods depending on your industry. This isn't set in stone, but it’s a solid starting point based on common practice.

This systematic weighting helps ensure your final valuation is grounded in the economic realities of your specific business and market.

Adjusting for External Market Forces

A valuation done in a bubble is basically worthless. The best, most accurate assessments always account for what’s happening in the broader economy and your specific industry. These outside forces can dramatically change what a buyer is willing to pay.

Take the current M&A landscape, for instance. A recent PwC Global Investor Survey found that over 75% of investors expect M&A activity to pick up. But they’re also wary of inflation and geopolitical risk. In an environment like this, a company with tight operations can command a valuation premium of up to 20%. Even better, businesses that have shored up their supply chains to be more resilient and local could see their value jump by 15-25%.

A credible valuation has to be forward-looking. It needs to reflect not just your company's potential but also the market's current mood—both its appetite for deals and its anxieties. Ignoring these external factors is a common and very costly mistake.

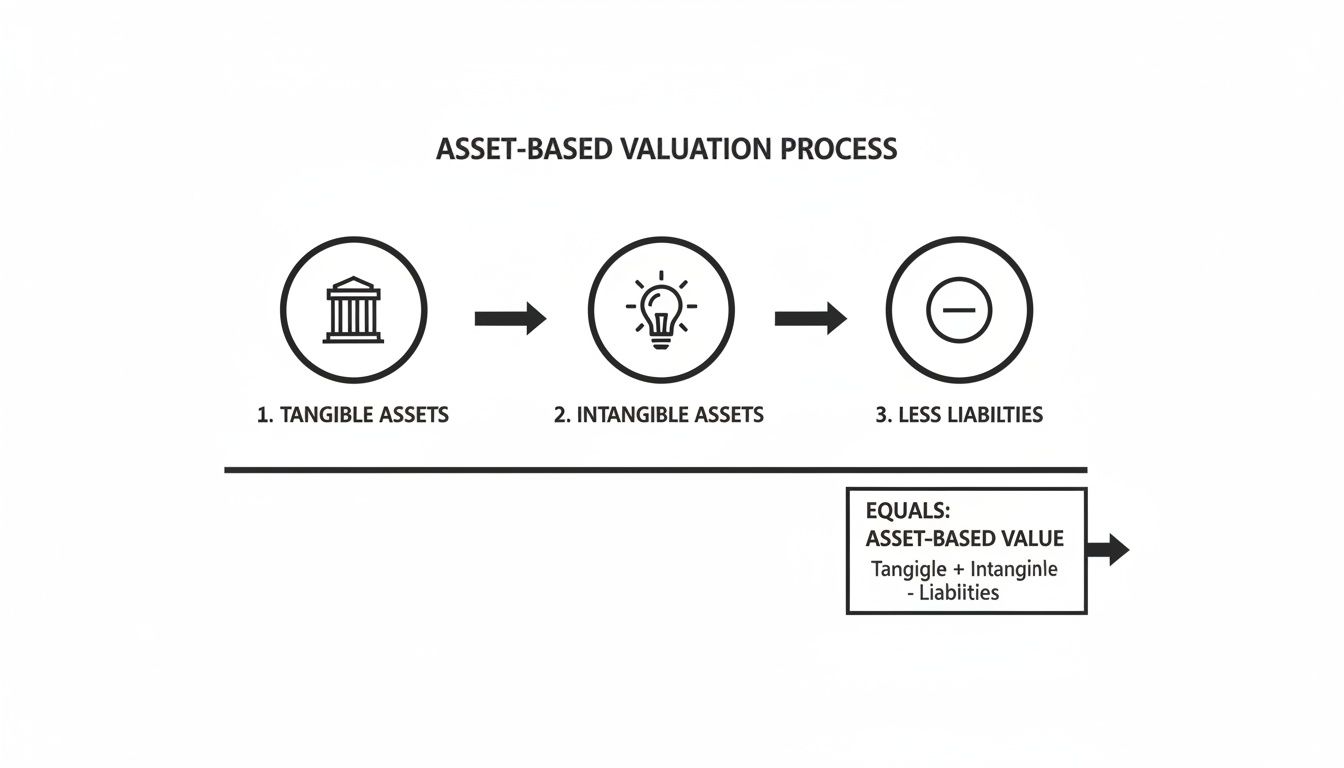

This diagram helps visualize the foundational Asset-Based approach, showing how tangible and intangible assets are tallied up before liabilities are subtracted.

As you can see, this method requires a thorough accounting of everything the company owns—both physical and non-physical—before backing out what it owes.

Building a Defensible Valuation Narrative

Your final valuation isn’t just a number on a spreadsheet; it’s the punchline to a well-reasoned story. The last step is to document everything and build a narrative that any outsider can follow and, most importantly, believe.

This means clearly laying out your assumptions, explaining why you chose certain comparable companies or discount rates, and justifying the weight you gave each method. This transparency is what turns a simple calculation into a powerful tool for negotiation.

A well-documented valuation report shows you’ve done your homework and gives buyers or investors the confidence they need to take the next step. It’s the final piece of the puzzle that ensures the value you've calculated is the value you ultimately get.

Common Questions About Business Valuation

Even after getting a handle on the core valuation methods, the practical questions start to surface. Figuring out how to value your business isn't just about the formulas; it's about navigating the real-world situations where that number really matters.

Let's walk through some of the most common—and critical—questions that come up when owners get serious about understanding their company's worth.

How Often Should I Value My Business?

For general strategic planning, getting a formal valuation done every one to two years is a smart move. Think of it as a regular financial health screening for your company. It’s a discipline that helps you track performance, pinpoint what’s really driving value, and make proactive decisions about your growth strategy.

But then there are the trigger events. These are the moments when an updated valuation isn't just smart—it's essential. You should never go into a major transaction or strategic shift without a fresh, defensible number.

These critical moments include:

- Seeking Investment: You need to justify your company's worth to people writing the checks.

- Planning a Sale: This is how you establish a credible asking price and walk into negotiations from a position of strength.

- Setting Up an ESOP: An employee stock ownership plan isn't just a great incentive; it legally requires a formal, defensible valuation.

- Estate and Gift Planning: A professional valuation provides a defensible number for tax filings and ensures your assets are distributed equitably among heirs.

Keeping your valuation current means you’re always operating with the most accurate information when the stakes are highest.

What Are the Biggest Valuation Mistakes to Avoid?

I’ve seen many well-meaning business owners fall into the same traps, which can seriously undermine the credibility of their valuation. Knowing what these pitfalls are is the first step to making sure your final number can actually withstand scrutiny.

The single most damaging error? Relying on just one valuation method. A truly comprehensive valuation is always a synthesis, drawing insights from multiple approaches to paint a complete picture.

Other frequent mistakes include using outdated or poorly prepared financial statements, which poisons the entire analysis from the very start. Equally problematic are wildly optimistic financial projections that aren't grounded in reality. Your forecasts have to be defensible, backed by market data and a clear, achievable plan. And finally, a lazy approach to selecting "comparable" companies can lead you far astray; applying valuation multiples from businesses that aren't truly similar will give you a meaningless result.

Can I Value My Own Business or Do I Need a Professional?

Sure, you can use online valuation calculators and simple formulas to get a rough, back-of-the-napkin estimate. But let’s be clear: those numbers are insufficient for any serious purpose. These tools just can't capture the nuance of your specific business, the dynamics of your industry, or the intangible assets—like brand reputation or intellectual property—that often hold significant value.

For any formal transaction, whether it’s a sale, a legal matter, or a tax filing, a valuation from a certified professional is non-negotiable.

A professional appraiser brings three critical elements to the table that you just can't replicate on your own: objectivity, access to proprietary transaction data, and a deep understanding of complex valuation methodologies. Their report isn't just a number; it's a critical investment that protects and maximizes your asset's value.

Attempting a DIY valuation for a major financial decision is like performing surgery on yourself. It’s a risk that simply isn’t worth taking.

How Does Debt Affect My Business Valuation?

Debt plays a huge role in determining what a business is ultimately worth to its owners. It directly hits the final equity value—the amount you would actually pocket after all obligations are settled.

When using the Discounted Cash Flow (DCF) method, for example, debt is a key input for calculating the Weighted Average Cost of Capital (WACC), which is your discount rate. Generally, more debt increases the WACC, which in turn can lower the present value of all your future cash flows.

With the market approach, you often start by calculating the Enterprise Value. This is the total value of the company's core business operations (think of it as the value of equity plus debt). But to get to the Equity Value—what your stake is truly worth—you have to subtract the company's total debt from its Enterprise Value. The formula is simple but powerful: more debt means less equity value for the owners.

Navigating the complexities of business valuation requires expertise and a deep understanding of financial markets. At Commons Capital, we specialize in providing comprehensive wealth management and financial advisory services to help high-net-worth families and business owners achieve their most critical financial goals. Whether you are planning for a sale, managing your estate, or seeking strategic financial guidance, our team is here to help you protect and grow your legacy. Learn more about how we can support your financial journey.