At its core, understanding how to calculate net worth is deceptively simple: you just subtract your total liabilities from your total assets. That straightforward formula, Assets - Liabilities = Net Worth, gives you the clearest possible snapshot of your financial health at any given moment. This guide will walk you through each step to ensure you get an accurate and meaningful result.

Why Your Net Worth Is Your Most Important Financial Metric

Before you start tallying up numbers, it's worth taking a step back to understand why this single figure is so powerful. Your net worth isn't just an entry in a spreadsheet; it’s the ultimate key performance indicator (KPI) for your entire financial life. For high-net-worth individuals, families, and business owners juggling complex finances, getting this number right is the bedrock of intelligent wealth management. It's the starting point that informs everything from multi-generational legacy planning to spotting the next big investment opportunity.

Beyond the Basic Formula

While the "Assets - Liabilities" equation looks easy on the surface, its real power is in the details. When your portfolio is a mix of private equity, real estate ventures, and maybe even a few unique collectibles, a quick, back-of-the-napkin calculation just won't cut it.

Nailing down this figure with precision allows you to:

- Actually Track Your Progress: See if your wealth-building strategies are paying off or if it's time to pivot.

- Secure Better Financing: A well-documented, strong net worth statement opens doors to more favorable loan terms.

- Make Smarter Decisions: It brings clarity to major choices around estate planning, retirement goals, and philanthropy.

This need for a precise calculation has never been more relevant. We just saw global wealth climb by 4.6%, with the average wealth per adult in North America hitting USD 593,347—the highest of any region. In a single year, the world saw a 1.2% increase in USD millionaires, and the US alone was responsible for creating over 379,000 of them. You can dig into these trends in the latest UBS wealth report, but the takeaway is clear: as assets grow, so does the need for meticulous tracking.

Before we dive into the "how," let's quickly outline the key pieces you'll need to pull together for your own net worth statement.

The Core Components of a Net Worth Statement

This table is just a high-level overview, but it sets the stage for the detailed inventory we're about to build.

A Holistic View of Your Finances

Ultimately, your net worth gives you a panoramic view that an income statement simply can't provide. It cuts through the noise of monthly cash flow to reveal your true financial position.

Your net worth isn’t about how much money you make—it’s about what you’ve managed to keep after everything you owe is paid off. It tells the real story of your financial decisions over a lifetime.

This perspective is what truly matters for building lasting wealth. By getting a firm handle on this core metric, you can have far more productive conversations with your financial advisors to protect and grow what you’ve built. The next sections will walk you through each step of this critical process, from inventorying your assets to making sense of the final number.

Building a Complete Inventory of Your Assets

The first real step in figuring out how to calculate net worth is taking a detailed inventory of everything you own. This isn't just about glancing at your bank account balance. For anyone with a complex financial life, creating a precise and comprehensive list of assets is the bedrock of an accurate calculation.

To get started, it’s best to split your assets into two main camps: liquid and illiquid. This distinction is crucial. It tells you not just about your total wealth, but also about your financial flexibility when you need it.

Cataloging Your Liquid Assets

Let’s start with the easy stuff. Liquid assets are things you can turn into cash quickly and easily without taking a major hit on their value. Their market values are usually pretty clear-cut, which makes them simple to tally up.

Your list of liquid assets should include:

- Cash and Cash Equivalents: This is the money sitting in your checking accounts, savings accounts, and money market funds.

- Publicly Traded Securities: Grab the current market value of your stocks, bonds, mutual funds, and ETFs from your brokerage statements.

- Vested Stock Options: Don't forget to include the in-the-money value of any vested employee stock options or restricted stock units (RSUs) you hold.

Getting these items organized is usually the most straightforward part of the process. If you need a hand structuring your data, our collection of financial planning worksheets offers a solid framework to make sure nothing slips through the cracks.

Valuing Your Illiquid and Tangible Assets

Now for the tricky part. Valuing illiquid assets is where things get more nuanced and, frankly, more challenging. These are items that can’t be sold in a hurry without potentially slashing the price. Getting these numbers right is absolutely critical, as a miscalculation can dramatically skew your final net worth figure.

This category is often where your most significant holdings live:

- Real Estate: List the current fair market value of your primary residence, vacation homes, and any investment properties. You can get a ballpark number from real estate websites, but for a more precise figure, a professional appraisal is the way to go.

- Private Business Equity: Valuing a stake in a private company is a complex beast. Methods can range from discounted cash flow analysis to comparing it with similar public companies. More often than not, you'll need a professional business valuation to get an accurate number.

- Retirement Accounts: Add up the total value of your 401(k)s, IRAs, and other tax-advantaged retirement plans. Just remember, these are pre-tax values.

- Collectibles and Personal Property: This bucket includes fine art, antiques, jewelry, and luxury vehicles. The key here is to value them at what a buyer would pay today, not what you originally paid for them.

When you're trying to figure out what physical items like collectibles are worth, it's essential to be realistic; this guide offers some great tips on how to find the value of antiques. For high-value pieces, professional appraisals are almost always your best bet to ensure your net worth statement is defensible.

Key Insight: The goal is to assign a realistic fair market value to every single asset. This isn't an emotional exercise; it's a practical assessment of what each item would realistically fetch if you sold it today. Over- or under-valuing your assets can lead to some seriously flawed financial decisions down the road.

Understanding the bigger picture can also add some helpful context. The simple formula for net worth—assets minus liabilities—is playing out on a massive global scale. A recent report noted that private household financial assets hit a staggering EUR 269 trillion, an 8.7% jump. North America holds about half of all private financial assets and drove 53.6% of that global growth in just one year.

Once you have a complete and accurately valued list of every single asset, you've knocked out the first—and often most demanding—half of the net worth equation. The next step is to apply that same diligence to the other side of the ledger: your liabilities.

Tallying Up the Other Side of the Ledger: Liabilities

Once you’ve got a handle on every asset you own, it’s time to face the other side of the equation: everything you owe. Getting a true snapshot of your net worth means creating an equally thorough list of your liabilities. It’s one of the most common places people make mistakes, and even small omissions can seriously skew your final number.

This isn’t just about scribbling down a couple of loan balances. For anyone with a complex financial life, liabilities can be layered and intricate. Just like we did with assets, let's break them down into a few key categories to make sure nothing slips through the cracks.

Secured vs. Unsecured Debt

Most of what you owe will fall into one of two buckets. Secured debts are tied directly to an asset—think a mortgage on a house or a loan on a car. If you don't pay, the lender has a claim on that specific property. On the flip side, unsecured debts aren't backed by any collateral. This is where things like credit card balances and personal loans come in.

Let’s start with the most common culprits:

- Mortgages and HELOCs: For every property you own, you need the current outstanding mortgage balance. Don't forget any second mortgages or home equity lines of credit (HELOCs) you've tapped into.

- Auto Loans: Add up the remaining balance on any car, boat, or other vehicle you’re financing.

- Student Loans: This includes the full amount you owe on any educational debt, whether it’s for you, your spouse, or your kids.

- Credit Card Balances: Go through every single card and list the total outstanding balance. We're not talking about the minimum payment here; you need the full payoff amount.

- Personal Loans: Any other unsecured loans from a bank, credit union, or online lender belong on this list.

For the most part, you can find these numbers by pulling up your latest statements online. Keeping good records makes this whole process infinitely easier. If you're wondering what to keep and what to toss, our guide on how long to keep financial documents can help you get organized.

Don't Forget the Less Obvious Liabilities

For many people, the list of debts goes well beyond the basics. These nuanced and often-overlooked obligations are absolutely critical for getting an accurate net worth figure and understanding your real financial exposure. It’s time to dig a little deeper.

Think about any of these more sophisticated liabilities:

- Investment-Related Debt: Have you borrowed against your portfolio with a margin loan? That’s a liability that directly offsets the value of your investments and absolutely must be included.

- Looming Tax Bills: If you sold some stock and realized a big capital gain or have other unpaid tax obligations coming due, you need to estimate that amount. It’s a real debt, just one you owe to the government.

- Personal Guarantees on Business Loans: This is a big one. If you’ve personally guaranteed a loan for your business, you've created a contingent liability. While the business is supposed to pay the debt, your personal assets are the backstop if it can’t. This has to be noted on your personal balance sheet.

- Other Financial Pledges: This category can include any other binding financial commitments you've made. Think capital calls you’ve promised for a private equity fund or a formal, multi-year pledge to a charity.

A Critical Point: Your liabilities reveal your financial leverage. A high debt-to-asset ratio can signal a much riskier financial position, even if your net worth looks impressive on paper. Understanding that balance is just as important as the final number.

Being brutally honest and thorough here is what separates a vague guess from a true financial picture. This diligence prevents you from operating with a falsely inflated net worth and gives you a clear-eyed view of your commitments. With a complete list of both assets and liabilities in hand, you're finally ready to put it all together.

Putting It All Together With a Real-World Example

You’ve done the hard work of meticulously listing your assets and liabilities. Now comes the moment of truth: the math. Theory is one thing, but seeing the numbers come together in a practical, real-world scenario is what really brings your personal balance sheet to life.

Let's walk through a detailed example for a hypothetical high-net-worth individual—a business owner with a diverse portfolio. This exercise will show you exactly how to organize your financial data to arrive at that all-important final figure.

Meet Our Example: Alex, a Business Owner

Alex is a successful entrepreneur with a significant stake in a private manufacturing company. Beyond the business, Alex has a mix of real estate holdings, a public stock portfolio, and a few other assets. On the other side of the ledger, Alex is carrying mortgages and some business-related debt.

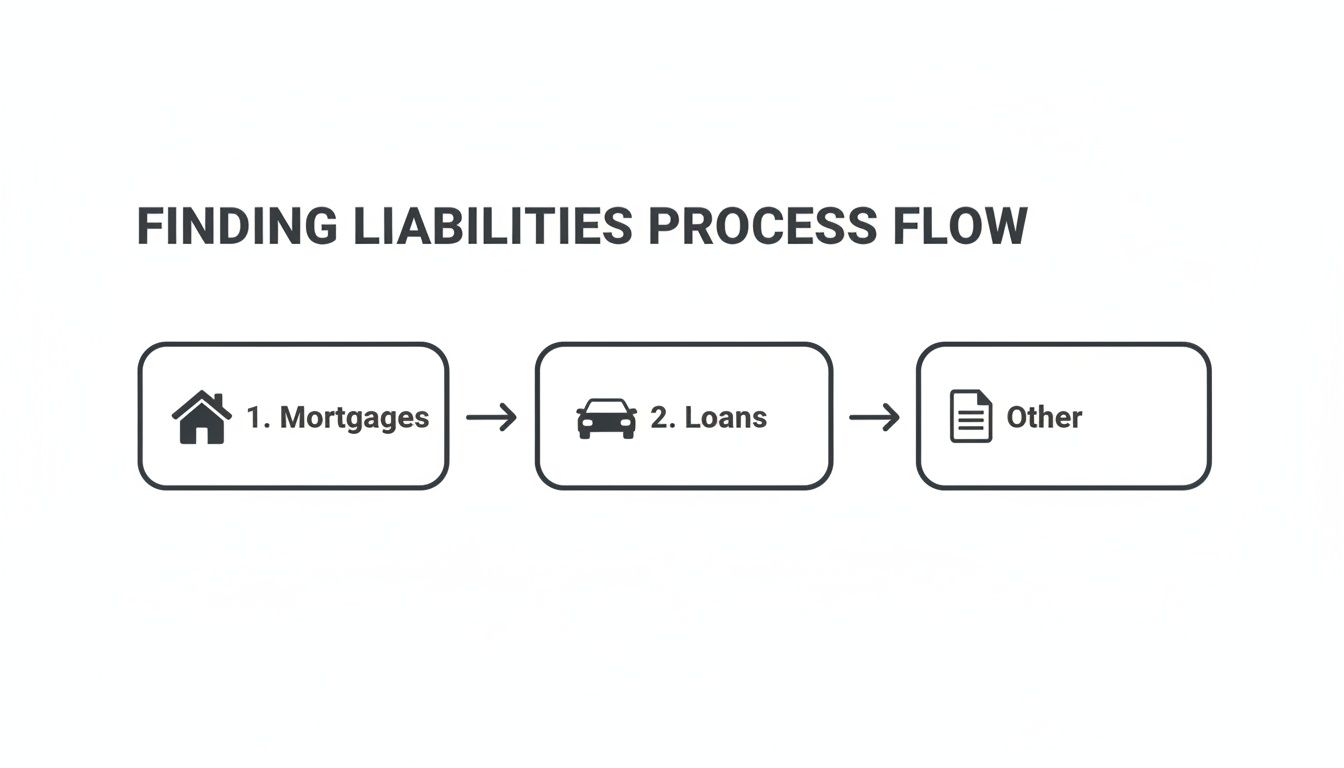

This flow chart gives you a simple visual for identifying the key liability categories we'll be digging into, from property-related debt to other financial obligations.

Breaking down liabilities into core groups like mortgages and loans simplifies what can feel like a daunting task, making it much easier to gather all the necessary figures for an accurate calculation.

Building the Balance Sheet: The Data

With all the numbers collected, it's time to build the personal balance sheet. Below is a sample statement that organizes all of Alex’s financial information. Notice how every asset and liability is clearly categorized—this is essential for both accuracy and for any future analysis. This is the exact structure you should aim to replicate.

Here's the detailed breakdown for Alex:

Sample Net Worth Calculation for a High-Net-Worth Family

This table shows just how important it is to include everything. Valuing private business equity is often the most challenging part of the puzzle. For a deeper dive into this complex process, you can check out our comprehensive guide on how to value your business.

Analyzing the Final Calculation

With the math done, Alex's net worth clocks in at $10,265,000. But the real work doesn't stop with that number. This statement is a powerful tool for understanding your financial health on a much deeper level.

One of the most common pitfalls I see is people forgetting to account for nuanced liabilities, like accrued taxes on investment gains. Alex wisely included an estimated $120,000 for potential capital gains taxes. This small step makes the final net worth figure a far more realistic representation of "liquidatable" wealth.

A personal balance sheet is more than an accounting exercise. It's a strategic tool that highlights your financial strengths and potential risks, empowering you to make more informed decisions about your wealth.

We can also quickly calculate a key metric like the debt-to-asset ratio. Just divide total liabilities by total assets:

- $2,685,000 (Liabilities) / $12,950,000 (Assets) = 0.207 or 20.7%

This ratio tells us that for every dollar of assets Alex owns, there are about 21 cents of debt. From my experience, this is a healthy level of leverage. It shows a strong financial position that isn't overly dependent on borrowing. Tracking this ratio over time is a great way to monitor any shifts in your financial risk profile.

By moving beyond a simple sum and creating a structured statement like this, you gain invaluable clarity. You're now equipped to see your finances not just as a random collection of accounts, but as a cohesive picture of your progress toward your long-term goals.

What Your Net Worth Actually Tells You

Calculating your net worth isn't just an accounting exercise. Too many people see it as getting to a final number, closing the spreadsheet, and feeling either good or bad about it. But that figure is really just the opening line of a much deeper conversation about your financial future.

Think of it as a dynamic tool, not a static score. The real power comes from tracking this number over time. A single calculation is just a snapshot, a single frame in a long movie. Watching your net worth evolve, however, reveals the underlying trends. Is your wealth truly compounding, or are you treading water? This perspective shift is what moves you from just knowing a number to understanding the story it tells.

From a Number to a Narrative

That single number—your net worth—ends up shaping some of the most critical financial decisions you'll ever make. It’s the bedrock of a solid estate plan, giving you a clear inventory to build effective wealth transfer strategies. It’s also the most honest benchmark for retirement readiness, helping you and your advisor gut-check if your current path actually lines up with the life you want to live down the road.

It also brings a dose of reality to your ambitions. Whether you’re eyeing a major new investment, looking to expand your philanthropic giving, or considering a significant purchase like a vacation home, your net worth tells you what’s truly possible. It grounds your decisions in objective data, clarifying your financial leverage and risk tolerance.

Connecting Your Finances to Broader Trends

Stepping back, understanding your own net worth also helps place your financial situation in the context of the wider economy. This is especially true for high-net-worth families planning across generations, where tracking wealth distribution and growth patterns can offer invaluable insight. The simple formula of assets minus liabilities, when applied globally, reveals some stark realities.

The latest research shows that ultra-high-net-worth (UHNW) individuals—those with over $30 million—now number around 510,810. It’s a tiny club. This group, just 1.1% of all high-net-worth individuals, controls an astonishing $59.8 trillion, or 32.4% of all HNW wealth. What’s more, the UHNW population has grown seven times faster than the global adult population since 2004. For clients in sports, entertainment, or running family offices with significant assets, these stats highlight why a precise net worth assessment is so crucial. As you can see in the full Altrata wealth report, accurate tracking is fundamental to joining or staying in those top tiers and pulling off long-term legacy goals.

Your net worth statement is your personal economic report card. It doesn’t just show where you are today—it provides the data needed to chart a more intentional and successful path forward.

When you can connect your personal numbers to these global trends, you're in a much better position to navigate market shifts and spot opportunities that others might miss.

A Tool for Effective Collaboration

Ultimately, the most practical reason to get a firm handle on your net worth is that it makes conversations with your financial team infinitely more productive. When you walk into a meeting with a clear, well-documented personal balance sheet, you skip the guesswork and get straight to strategic planning.

This clarity empowers your wealth advisors to:

- Identify Opportunities: A detailed statement can quickly reveal if you're over-concentrated in one asset class or highlight smart ways to diversify.

- Manage Risk: It gives a clear picture of your debt-to-asset ratio and overall financial leverage, which is essential for building better risk management strategies.

- Optimize for Taxes: You can't have an effective tax plan without first understanding the exact composition of your assets and liabilities.

Your net worth is far more than a vanity metric. It's the most honest and comprehensive measure of your financial health. By treating it as a living document, you transform it from a simple chore into your most powerful tool for building and preserving lasting wealth. It’s the starting point for every meaningful financial strategy you will ever implement.

Common Questions About Calculating Net Worth

Even with a step-by-step guide, the real world is messy. When you actually sit down to crunch the numbers on your net worth, specific questions always pop up. The details really matter, especially when your financial picture has a few moving parts.

Think of this as your quick-reference guide for those finer points. Getting these details right is what turns a simple number into a reliable foundation for smart financial planning.

How Often Should I Tally Everything Up?

For most people with a diverse portfolio, doing a deep dive once a year is a great rhythm. It gives you a clear, big-picture review that's perfect for annual meetings with your financial advisor to see how you're tracking against your long-term goals.

But if a big chunk of your wealth is tied up in volatile markets, or if you're navigating a major life change, a quarterly check-in can be incredibly valuable. Things like selling a business, getting an inheritance, or buying a large piece of real estate can shift your balance sheet dramatically. Calculating more often during these times lets you stay agile and make smarter moves when it counts.

Key Takeaway: The right timing depends on your financial complexity and what's happening in your life. Start with an annual review, but don't hesitate to ramp it up to quarterly when things are in flux.

What About Personal Stuff Like Cars and Jewelry? Do I Count That?

Yes, but you have to be brutally honest about their value. While your home is a major asset, things like luxury cars, art collections, and jewelry fall into a category often called 'personal use assets'. Their value can be tough to nail down, and finding a buyer isn't always quick or easy.

The rule of thumb is to include them at their current fair market value—what a real buyer would actually pay for them today, not what you paid a decade ago. For any significant collections, it’s absolutely worth getting a professional appraisal. This makes sure your net worth statement is based on a defensible, accurate figure, not an emotional or inflated one.

How in the World Do I Value My Stake in a Private Company?

This is easily one of the trickiest parts of the calculation for any business owner. Unlike a public stock, there's no ticker symbol you can look up for a daily price. The most common valuation methods involve a discounted cash flow (DCF) analysis or applying valuation multiples from similar public companies.

Frankly, this is such a specialized area and has such a massive impact on your total net worth that you should bring in a pro. Working with a business valuation expert will give you a realistic number that can stand up to scrutiny—which is critical for everything from estate planning to securing a loan.

Do I Need to Subtract Potential Capital Gains Taxes from My Assets?

If you want the most precise and conservative number, the answer is a definite yes. A basic calculation often uses pre-tax asset values, and that’s fine for a quick snapshot. But a more sophisticated approach looks at the 'after-tax' value.

This means you estimate the capital gains tax you’d owe if you sold an asset, like your stock portfolio or an investment property. Factoring this in gives you a much more realistic view of your liquidatable net worth—the actual cash you'd have left after settling up with Uncle Sam. This level of detail is non-negotiable for high-level retirement and estate planning.

Many people wonder which software is best for keeping track of all these moving parts. A comparison between Quicken vs QuickBooks can be helpful, as both are designed to track the assets and liabilities you need for this calculation.

At Commons Capital, we help high-net-worth individuals and families navigate these complexities every day. If you're ready to move beyond just the numbers and start building a real strategy for your wealth, we're here to help. Contact us to learn how our tailored financial advisory services can bring clarity and confidence to your financial life at https://www.commonsllc.com.