Learning how to build business credit isn't just another item on your financial to-do list; it's a critical strategic move that creates a firewall between your company's liabilities and your personal assets. You're essentially creating a credit profile for your business that is entirely separate from your own. This crucial step allows the company to secure financing on its own merits, protecting your personal wealth from the ups and downs of the business.

Why Business Credit Is Your Greatest Financial Asset

For high-net-worth individuals and serious entrepreneurs, understanding how to build business credit is non-negotiable. It’s the move that elevates a venture from a side project into a legitimate, scalable entity.

Think of it as giving your business its own financial ID. It's an identity that can stand on its own two feet, without ever needing to lean on your personal credit score.

This separation is the ultimate form of asset protection. When your business has a strong credit profile, lenders and suppliers look at your company's financial health, not your personal savings or 401(k). This distinction becomes absolutely crucial when you're trying to land substantial funding or just navigate a rough economic patch. Your personal financial security should remain intact, regardless of your business's quarterly performance.

The Strategic Advantages of a Separate Credit Profile

Beyond just protecting what's yours, a robust business credit profile unlocks some serious growth opportunities. It's the key that opens doors to better financing terms, higher credit limits, and even lower insurance premiums. A strong score signals to partners, lenders, and potential investors that your business is stable, reliable, and a good bet.

This credibility is what helps you land large contracts or negotiate better terms with vendors. According to Equifax, establishing business credit is a powerful way to signal stability — a crucial factor when you consider that 65.3% of businesses fail within 10 years. A solid credit history proves your company can handle its financial obligations, which is a massive advantage in a competitive market.

Building a Foundation for Long-Term Success

At the end of the day, building business credit is a core piece of sound financial planning for business owners. It gives you the financial leverage needed for expansion, buying new equipment, or managing cash flow without ever putting your personal assets on the line.

As your business grows, this separation allows you to chase bigger opportunities with confidence.

For entrepreneurs, a strong business credit score is not just a number — it is a testament to the company's viability and a critical tool for scaling operations while preserving personal wealth.

This proactive approach to your finances ensures that your company has the resources and reputation to thrive on its own. It's not just a good idea; it's a strategic imperative that pays dividends for the entire life of your business.

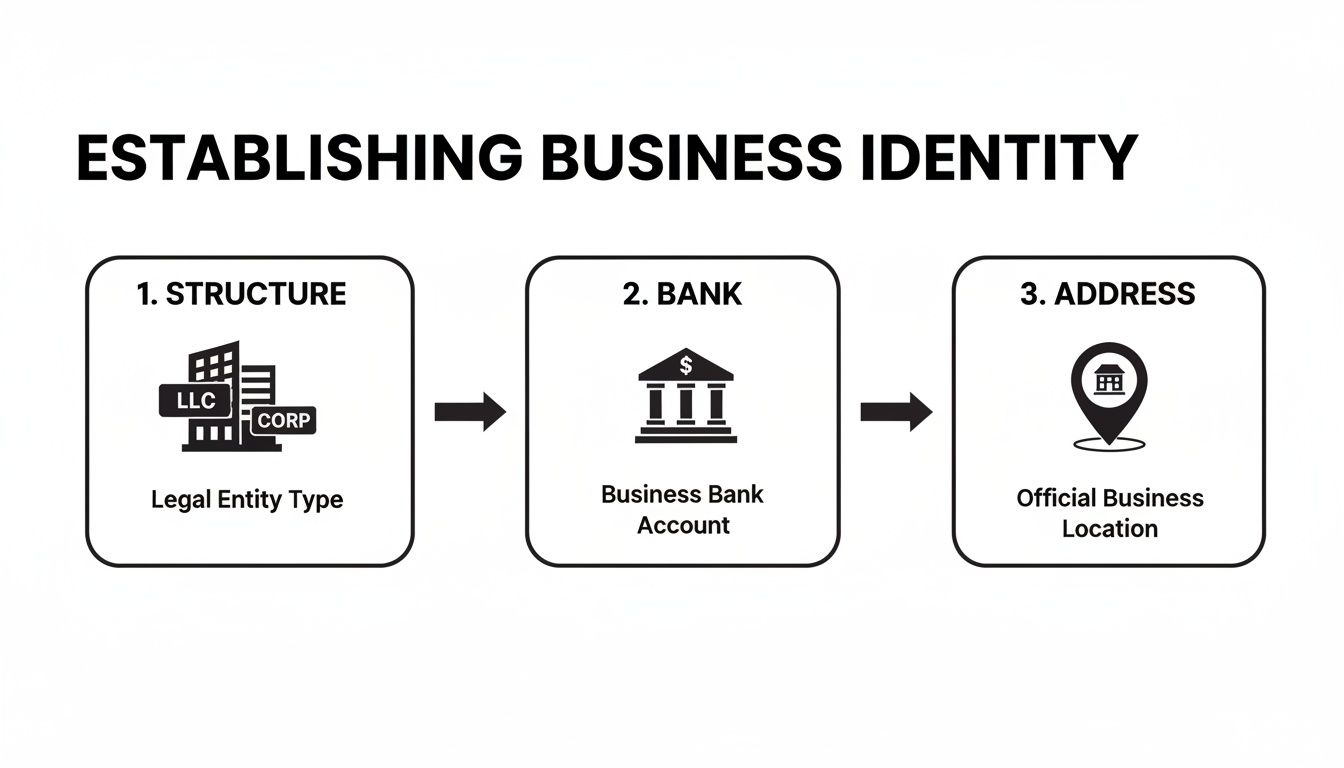

Building Your Business's Financial Identity

Before anyone will lend your business a dime, it needs to be seen as a legitimate, standalone entity. Think of this first phase as giving your company its own unique financial fingerprint, one that's completely separate from your personal life.

This isn't just about paperwork; it's about sending the right signals to credit bureaus and lenders that you're a serious, stable operation.

The first move is always to formalize your business structure. Operating as a Limited Liability Company (LLC) or a corporation is a game-changer. Why? Because these structures create a legal wall between you and your company, which is the bedrock of protecting your personal assets if the business runs into trouble.

Sole proprietorships and partnerships, on the other hand, often hit a brick wall when trying to build business credit. Lenders see them as one and the same as the owner, meaning everything gets tied back to your personal credit score. Formal incorporation is how you break that link. For a deeper dive, it's worth understanding the impact of incorporation on business credit.

Secure Your Employer Identification Number

Once you're legally structured, your next immediate task is getting an Employer Identification Number (EIN) from the IRS. It’s essentially a Social Security Number for your business — a unique nine-digit code that identifies it for all financial purposes.

You'll need this number for just about everything: filing taxes, opening a bank account, and, most importantly, applying for credit. When a lender pulls your business's credit history, they use the EIN, not your SSN.

Open a Dedicated Business Bank Account

Mixing personal and business funds is one of the fastest ways to kill your credit-building momentum before it even starts. A dedicated business bank account isn't optional; it's a requirement.

It creates a clean financial record that screams professionalism and makes your bookkeeping infinitely simpler. Lenders see a separate account as a sign of a well-managed company, and the consistent cash flow running through it builds a track record they can use to evaluate future loan applications. This simple step reinforces the legal separation you created with your LLC or corporation.

A separate business bank account does more than simplify accounting; it proves to lenders that your business operates as a serious, independent financial entity, which is a prerequisite for establishing strong credit.

Establish Your Business's Physical Presence

The final pieces of the puzzle involve creating a professional footprint. This means ditching the P.O. Box and your home address for official business filings.

- Business Address: Use a physical commercial address. This could be a leased office or even a virtual office address. Credit bureaus see a real business address as a much stronger indicator of stability.

- Business Phone Number: Get a dedicated phone line. Make sure it's a toll-free or local number that's listed in directories under your company's name.

- Professional Website and Email: A polished website and a domain-based email address (like

yourname@yourcompany.com) add another crucial layer of legitimacy.

These details might seem small, but they are absolutely critical. Bureaus like Dun & Bradstreet use this information to verify your business actually exists and is operational. Without this verification, they won't even generate a credit file for you.

Putting these foundational pieces in place is what gets the clock ticking. It typically takes about 90-120 days for your first business credit scores to even appear. From there, you enter a 'score growth phase' over the next 4-12 months as you begin establishing a history of on-time payments.

Checklist for a Credit-Ready Business Entity

Follow these essential actions to establish a business entity that credit bureaus and lenders will recognize as legitimate and trustworthy.

Completing every item on this checklist ensures you've built the proper foundation. It tells the financial world that your business is a distinct, credible entity ready to handle credit responsibly.

Opening and Managing Your First Tradelines

Once your business has a solid financial identity, it's time to start building a payment history. This is where tradelines come into the picture. A tradeline is really just any account that reports your payment activity to the business credit bureaus, and getting those first few established is a major milestone.

The game plan is to start small. You'll want to find vendors known for working with new businesses, specifically suppliers offering net-30 terms. That just means they give you 30 days to pay an invoice. But here's the most important part: you have to make sure these vendors actually report your payments to bureaus like Dun & Bradstreet, Experian Business, or Equifax Business. If they don't report, it's like the transaction never happened in the eyes of the credit world.

The flowchart below shows the essential steps you've already taken to get to this stage. You’ve created the business identity that’s your ticket to opening these accounts.

This isn’t just about ticking boxes. Structuring your entity, opening a bank account, and setting up a proper business address are the credentials you need to be taken seriously by vendors and lenders.

Finding and Applying for Starter Vendor Accounts

Let's be clear: not all suppliers report to credit bureaus. You have to be strategic. Many "starter" vendors are perfect because they sell things you probably need anyway, like office products, shipping boxes, or cleaning supplies.

When you apply, they'll use your EIN, business address, and phone number to verify you're a legitimate operation. Some might have minimum order requirements before they start reporting, so always read the fine print. A few of the most well-regarded starter vendors that have a reputation for reporting include:

- Uline: A go-to for just about any shipping or industrial supplies.

- Grainger: Offers a huge range of industrial and maintenance products.

- Quill: Specializes in office supplies, from paper and ink to furniture.

The core principle is simple but powerful: make small, necessary purchases on credit, and then pay the invoice well before the due date. Paying early is a potent signal to the credit bureaus that your business is exceptionally reliable.

The Power of Paying Early

Paying on time is the bare minimum. If you want to build an excellent score quickly, paying early has a massive positive impact.

Take the Dun & Bradstreet PAYDEX score, a key metric that lenders watch closely. It's a direct reflection of how fast you pay your bills. A score of 80 means you pay on time. But a score of 100 — the best you can get — means you pay 30 days before the due date. If you make a habit of paying early from the very beginning, you can build an impressive score in a hurry.

Leveraging Early Success for Bigger Opportunities

Think of your first few tradelines as the foundation. Once you have at least three to five of them reporting positive payment history for a few months (usually 90-120 days is enough), you’ll see a business credit score pop up. This score is your key to the next level of financing.

This early track record proves to other creditors that you're a low-risk bet. You can then take this new credit profile and apply for more substantial credit lines, like:

- Retail Credit Cards: Think store cards from places like Staples, Lowe's, or Home Depot. They're often easier to get than major bank cards and add some nice diversity to your credit file. Once they see your positive vendor payment history, they're much more willing to extend credit.

- Fleet or Gas Cards: If your business uses vehicles, cards from fuel companies like Shell or BP are another great stepping stone. They also tend to have more forgiving approval requirements for businesses that have a documented history of paying on time.

Every new account you open and manage well adds another layer of positive data to your credit report. This creates a compounding effect, where a small foundation of on-time vendor payments unlocks access to more powerful credit tools. It’s a methodical process, but this is how you go from buying office supplies to qualifying for the corporate cards and loans that fuel real growth — all without putting your personal credit on the line.

Leveling Up to Business Loans and Corporate Cards

You've diligently paid your vendors on time, and now your business isn't a financial ghost anymore. You’ve built a payment history that proves you’re reliable, and that’s the real key to unlocking the kind of financing that fuels serious growth. It’s time to graduate from starter tradelines to the big leagues.

This next phase is all about leveraging that hard-won credit profile. We're talking about securing actual business loans, lines of credit, and the holy grail for most founders: corporate credit cards that don't chain you to the business's debt. These are the tools that let you scale, buy that expensive piece of equipment, or navigate a cash flow crunch without touching your personal savings.

Navigating Different Types of Business Financing

Not all funding is the same, and what’s right for you boils down to your immediate needs and where you see the business going. Lenders are going to be scrutinizing your time in business, your revenue, and, of course, those business credit scores you've been building.

Let's break down the common options and when they make the most sense:

- Business Line of Credit: Think of this as a flexible, revolving credit line. You draw what you need, when you need it, and pay it back. It's a lifesaver for managing unpredictable cash flow, jumping on a surprise opportunity, or just handling unexpected bills without the commitment of a huge loan.

- Term Loan: This is your classic loan. You get a lump sum of cash upfront and pay it back, with interest, over a set period. Term loans are perfect for planned, big-ticket investments — think opening a new location, launching a massive marketing blitz, or even acquiring a smaller competitor.

- Equipment Financing: Need a new truck, specialized machinery, or a major tech upgrade? This loan is built for that. The equipment itself usually serves as the collateral, which can make these loans a bit easier to get, especially if you have major tangible asset needs.

Once your business credit is solid, securing one of these is the logical next step. If you want to dive deeper into the nuts and bolts, you can learn more about how to get a business loan and get yourself ready for the process.

The Ultimate Goal: Corporate Credit Without a Personal Guarantee

For so many entrepreneurs I work with, the real finish line is getting that corporate credit card that stands completely on its own. This means no personal guarantee (PG) is required. This is it — the final, most critical wall between your business and personal finances.

When you sign a personal guarantee, you're telling the bank, "If my business can't pay this, I will." Getting rid of that requirement is a massive vote of confidence in your company's financial health and a cornerstone of asset protection. Our guide on the risks of a business loan personal guarantee breaks down exactly why this is such a non-negotiable strategy for founders.

Lenders don't just hand these out. They only waive the personal guarantee for businesses that are an exceptionally low risk. That usually means a powerful combination of strong, consistent revenue, at least two years of operating history, and top-tier business credit scores.

Preparing an Application That Gets Approved

To land these higher-tier financing options, you need to show lenders a compelling story. Your application needs to be buttoned-up, professional, and paint a crystal-clear picture of a stable, growing company.

Before you even think about applying, get this file together:

- Updated Financial Statements: Lenders will want to see your balance sheet, income statement, and cash flow statement. This is your proof that the business is profitable and knows how to manage its money.

- A Solid Business Plan: Be ready to talk vision. Explain precisely how you'll use this money to generate more revenue and grow. Don't be vague.

- Clean Credit Reports: Pull your own reports from Dun & Bradstreet, Experian, and Equifax before the lender does. Find and dispute any errors and make sure every payment is listed as on-time.

Walking in with this documentation ready to go sends a powerful message. It tells lenders you're a serious, well-organized operator who respects their process. It dramatically increases your odds of getting that "yes."

Monitoring and Protecting Your Business Credit Health

Building business credit isn't something you can "set and forget." Think of it as an ongoing discipline, a continuous effort to maintain the financial credibility you've worked so hard to establish. Moving into a long-term strategy means actively keeping an eye on your business credit reports and truly understanding the story they tell lenders, vendors, and potential partners.

This proactive approach is what separates the businesses that thrive from those that struggle. It’s the key to protecting your company's borrowing power for whatever comes next.

Your business credit reports are essentially a live dashboard of your company's financial health. You absolutely need to know what's on them, what it all means, and how to fix any inaccuracies before they spiral into costly problems.

Key Metrics to Watch on Your Reports

When you pull your reports from Dun & Bradstreet, Experian Business, and Equifax Business, you'll be hit with a lot of data. Don't get overwhelmed. From my experience, a few key metrics carry the most weight and demand your regular attention.

- Payment History (PAYDEX Score): This is the big one — the single most influential factor. D&B's PAYDEX score, which runs from 1 to 100, is a direct reflection of how you pay your bills. A score of 80 means you pay on time. A perfect 100 means you consistently pay invoices 30 days early. Lenders look here first.

- Credit Utilization Ratio: This metric simply shows how much of your available credit you're actually using. If you're constantly maxing out your credit cards or lines of credit, it’s a massive red flag. High utilization tells lenders your business might be overleveraged or facing cash flow issues.

- Credit History Length: The age of your oldest accounts really matters. A long, positive credit history demonstrates stability and a proven track record. This is why it’s often smart to keep older, well-managed accounts open, even if you don't use them frequently.

Getting a handle on these scores is the first step. The different bureaus have their own models, and it helps to know what a "good" score looks like to a lender.

Understanding Your Business Credit Scores

Here’s a quick breakdown of the major business credit scores, what they measure, and how lenders use them to size up your company's financial health.

These scores give lenders a snapshot of your risk profile, so knowing where you stand with each is crucial before you apply for new financing.

Practical Tips for Long-Term Credit Health

Maintaining excellent business credit really comes down to disciplined habits. It's about building systems that ensure you never miss a beat.

One of the most common — and entirely avoidable — mistakes I see is late payments. Setting up automated payments for all your recurring bills is a simple but incredibly powerful way to prevent this. It ensures vendors and lenders are always paid on time, protecting your reputation.

Beyond that, keep a close watch on your credit utilization. A good rule of thumb is to keep your balances below 30% of your total credit limit on all accounts. If you have to make a large purchase, think about paying down the balance before your statement closing date. That simple move can keep your reported utilization low and your scores healthy.

The health of your business credit is a direct reflection of your financial discipline. Regular monitoring allows you to catch issues early, dispute errors, and make strategic adjustments that preserve your borrowing power and readiness for future opportunities.

Disputing Errors and Protecting Your Profile

Errors on credit reports are far more common than you might think. A simple clerical mistake — like a payment reported late when it was on time — can drag your scores down.

If you find an inaccuracy, you have to act immediately. Each credit bureau has a formal dispute process. You’ll need to submit your claim in writing and provide any documentation you have to back it up, such as bank statements or canceled checks. By law, they have to investigate and correct verified errors.

Regularly reviewing your reports is your best defense. Make it a quarterly routine. This ensures the information lenders see is an accurate reflection of your company's financial strength, keeping you ready for the next growth opportunity that comes your way.

Answering Your Top Questions About Building Business Credit

Once you start down the path of building business credit, a lot of questions pop up. It's totally normal. You're moving from just having an idea to managing real accounts, and you want to make sure you're getting it right. Let's clear up some of the most common points of confusion so you can sidestep the usual pitfalls.

How Long Does This Actually Take?

This is probably the number one question I get. You can get an initial credit file and score on the board surprisingly fast — often within 90-120 days after your first few vendor payments get reported. But getting to "good" or "excellent" credit? That's a longer game.

Think of the first three to six months as your proving ground. You're just trying to show you're consistent. The real momentum builds between six and eighteen months, as you stack up a solid track record of on-time payments across different types of accounts. If you're aiming for the big leagues — serious loans or corporate cards without a personal guarantee — lenders will want to see at least one to two years of clean, verifiable credit history.

Will Using My Personal Card for Business Stuff Help?

Let me be blunt: absolutely not. This is a critical mistake many new entrepreneurs make. When you use a personal credit card for business expenses, the only score you're affecting is your own.

Business credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business only care about accounts opened under your company's name and its Employer Identification Number (EIN). To build business credit, you have to use products issued directly to your business. This means net-30 vendor accounts, business loans, or true business credit cards. Mixing your finances just muddies the waters and does zero to establish your company as a separate, creditworthy entity.

By far, the most damaging thing you can do when building business credit is pay late. Business credit scores are brutally sensitive to payment history — much more so than personal scores. Just one late payment can tank your rating.

What's the Single Biggest Mistake to Avoid?

While mixing personal and business finances is a bad habit, the most destructive mistake you can make is paying late. It's that simple. Business credit scores, especially the D&B PAYDEX score, are almost entirely about your payment history. A single invoice reported 30 days late can torpedo your scores and screams "risk" to any potential lender or supplier looking you up.

The fix is straightforward: always pay on time, or even better, pay early. Set up autopay wherever you can. It’s a simple system to prevent a catastrophic error and keep your payment record pristine.

Can I Do This If My Personal Credit Isn't Great?

Yes, you can, and that’s one of the most powerful reasons to go through this process in the first place. Lenders might peek at your personal credit for your first bit of financing — that's common for a brand-new business — but the whole point is to build a business profile that stands on its own two feet.

Here’s your game plan:

- Start with Friendly Vendors: Open accounts with suppliers who are known for reporting to the business credit bureaus. Many of these "starter" vendors are less likely to pull your personal credit.

- Get a Secured Business Card: Look for business credit cards designed for new companies. Some may still require a personal guarantee at first, but it's a foot in the door.

- Be Obsessive About Payments: A perfect payment history on your business accounts is your best weapon against a weak personal score. It proves your business is reliable, regardless of your personal history.

Over time, as your business credit history gets stronger, your personal score becomes less and less relevant for business financing. That gradual separation is the key to true financial independence for your company.

Navigating the complexities of wealth management and business finance requires expert guidance. At Commons Capital, we specialize in helping high-net-worth individuals and business owners build and protect their financial futures. Discover how our tailored advisory services can support your goals at https://www.commonsllc.com.