That old advice to save 15% of your pre-tax income for retirement? It’s a decent starting point for some, but it completely misses the mark for high-net-worth individuals.

When you're juggling variable income, business assets, or complex legacy goals, a simple percentage-based rule just won't cut it. Answering "how much should I be saving for retirement each month?" demands a much more strategic approach than any generic formula can offer.

Moving Beyond the 15% Savings Rule

Let's be honest—the standard 15% rule wasn't designed for a complex financial life. While it's a helpful benchmark for someone with a consistent salary and straightforward goals, it quickly becomes irrelevant for entrepreneurs, professional athletes, or families managing significant wealth.

These situations introduce variables that a one-size-fits-all approach simply can't handle. A business owner might reinvest heavily in their company for years, leading to a lower personal savings rate before a massive liquidity event down the road. An entertainer could have a few incredibly high-earning years followed by leaner periods.

In these cases, saving a flat 15% annually is neither practical nor optimal.

Why Generic Formulas Miss the Mark

The main problem with these simple savings rules is that they ignore the unique financial DNA of high earners. Your plan has to account for factors that go far beyond a simple slice of your income.

These are the critical components a generic rule can't see:

- Variable Income Streams: Your savings strategy needs the flexibility to handle fluctuating cash flow from business profits, bonuses, or project-based work.

- Complex Asset Allocation: High-net-worth portfolios often include illiquid assets like real estate or private equity, which don't fit neatly into traditional retirement calculators.

- Sophisticated Tax Planning: Your savings plan must be woven into a tax strategy that minimizes your liability now and in retirement, using vehicles well beyond a standard 401(k) or IRA.

- Legacy and Philanthropic Goals: If you plan to leave a significant inheritance or fund a foundation, your savings targets will need to be substantially higher to support goals that extend beyond your own lifetime.

The real question isn't just about replacing your income; it's about funding a specific, multi-faceted vision for your future. This requires moving from a simple savings percentage to a comprehensive wealth-building strategy.

So instead of asking if you're saving enough based on some generic rule, the better approach is to build a plan grounded in your personal ambitions. This means defining what retirement actually looks like for you, making realistic assumptions about the future, and structuring your savings in the most efficient way possible.

The rest of this guide will walk you through that exact process, helping you build a retirement savings plan that is truly your own.

Defining Your High-Resolution Retirement Picture

Before you can figure out a monthly savings number, you have to know exactly what you’re saving for. Answering "how much should I save?" is impossible without first painting a vivid, high-resolution picture of the life you actually want to lead. This vision is the bedrock of your entire financial strategy.

Are you picturing your golden years spent traveling the world? Maybe you’re driven to fund a philanthropic passion or ensure a substantial legacy for your family. Each of these goals comes with a vastly different price tag and, as a result, demands a completely different savings plan. Vague goals just lead to vague plans—specificity is your greatest asset right now.

Getting clear on this transforms your savings from a dull financial chore into a tangible pursuit of your future self. It’s the difference between saving "for retirement" and saving for that vineyard tour in Tuscany or for the new wing on the local hospital.

What Is Your Income Replacement Ratio?

Once you have that vision, the next step is translating it into a concrete annual income figure. This is where the concept of the income replacement ratio comes into play. It’s simply the percentage of your pre-retirement income you'll need each year to maintain your desired standard of living after you stop working.

A common rule of thumb you’ll hear is to aim for 80% of your pre-retirement income. The logic goes that certain expenses, like saving for retirement itself or paying payroll taxes, will disappear. But for many high earners, this baseline often falls short.

Think about these real-world scenarios:

- The World Traveler: If your retirement involves extensive travel, your annual spending might actually increase. In this case, a 100% or even 110% replacement ratio might be more realistic.

- The Downsized Lifestyle: On the other hand, if you plan to pay off your mortgage, downsize, and live a quieter life, you might get by comfortably on 70-75% of your former income.

- The Philanthropist or Legacy Builder: For those with major charitable goals or the desire to leave multi-generational wealth, your income needs may far exceed your personal spending, requiring a much larger nest egg.

Your target ratio is deeply personal. Think of it as the financial expression of your retirement dreams.

From Annual Income to Your Total Nest Egg

With your target annual income in hand, you can now calculate the total size of the portfolio needed to generate it. A long-standing framework for this is the 4% rule.

The rule suggests you can safely withdraw 4% of your initial retirement portfolio value each year, adjusting for inflation, without running out of money over a 30-year retirement. To use this as a quick estimate, just multiply your desired annual income by 25.

For example, if you determine you need $200,000 per year in retirement:$200,000 (Annual Income) x 25 = $5,000,000 (Target Nest Egg)

But a word of caution. For those planning longer retirements or facing today's market volatility, a more conservative withdrawal rate of 3% to 3.5% is often a smarter move. A lower withdrawal rate gives you a much larger buffer against market downturns and the risk of outliving your money. Using this more cautious approach significantly changes the target.

Take that same $200,000 annual need with a 3% withdrawal rate:$200,000 (Annual Income) / 0.03 = $6,666,667 (Target Nest Egg)

Key Takeaway: The 4% rule is a useful starting point, not an ironclad law. Modern financial planning often means adjusting this figure downward to account for longer lifespans and unpredictable markets, especially for high-net-worth portfolios.

Of course, this calculation doesn't factor in other income sources like pensions or Social Security. To see how government benefits might fit into your plan, you can learn more about how they are calculated with our guide to the Social Security benefits calculator. Knowing this helps refine how much income your personal portfolio truly needs to generate.

Ultimately, defining your retirement picture and calculating your target nest egg are the foundational steps. They give you the "why" behind your monthly savings and a clear destination to aim for.

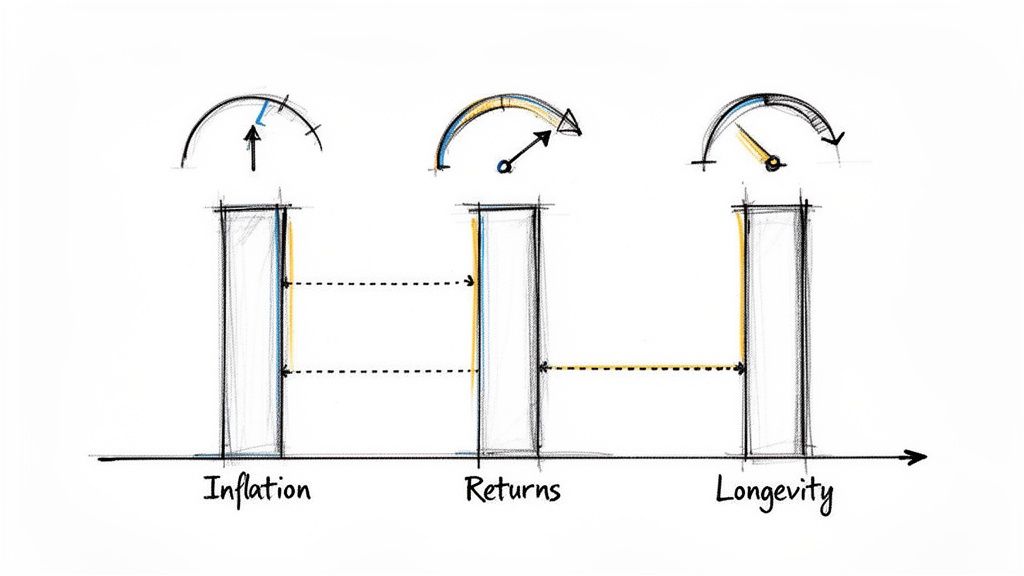

Grappling With Retirement's Three Big Unknowns

Figuring out your target nest egg is a great start, but a retirement plan built on pure math without a dose of reality is a house of cards. The road to retirement is never a straight line; it’s full of variables that can completely change the outcome. Getting a handle on these moving parts is what separates a plan that looks good on paper from one that actually works.

Three powerful forces will ultimately define your financial future: inflation, investment returns, and how long you live (longevity). If you drop the ball on any one of these, you risk letting your hard-earned wealth slowly unravel over time, turning what should be a comfortable future into a major source of stress.

Taming Inflation: The Silent Killer of Savings

Think of inflation as a quiet tax that eats away at your savings every single year. It might not feel like a big deal day-to-day, but over two or three decades, its power to erode your purchasing power is staggering. An average inflation rate of just 3% will slice the value of your money in half in about 24 years.

That means the $5 million portfolio you're aiming for today will buy a lot less by the time you actually need to start spending it. Your investment strategy has to be designed to beat inflation, not just keep pace with it. This is precisely why holding too much cash over the long haul is one of the riskiest things you can do.

Key Insight: The only number that truly matters is your real rate of return. That's what you’ve earned after backing out inflation. If your portfolio is up 7% for the year but inflation was 3%, your real return is only 4%.

Setting Realistic Expectations for Investment Returns

Projecting how your portfolio will grow is a tricky balancing act. It’s tempting to plug in high, double-digit return numbers to make the math work and lower your monthly savings target. But that's a dangerous game that can leave you with a massive shortfall down the road.

For a high-net-worth investor, a properly diversified portfolio is going to have a few key ingredients:

- Public Equities: This has historically been the engine for real growth, but it comes with plenty of volatility.

- Fixed Income (Bonds): Bonds act as the portfolio's ballast, providing stability and predictable income when the stock market gets choppy.

- Alternative Investments: Things like real estate, private equity, or venture capital can offer returns that don't move in lockstep with public markets, but they also tend to be less liquid.

For planning purposes, assuming a blended, long-term annualized return of 6-8% is a sensible and prudent place to start. Anything much higher than that means you're likely taking on a whole lot more risk. It's also a smart idea to dig deeper and learn how to stress-test your retirement portfolio against different market shocks.

Planning for a Longer Life and Longevity Risk

Ironically, one of the biggest financial risks we face today is a good problem to have: living longer than we ever expected. "Longevity risk" is the very real possibility of outliving your money. Retirements that stretch for 30 or even 40 years are becoming more and more common, and that requires a completely different planning mindset than a retirement lasting just 15 or 20 years.

A longer timeline puts incredible strain on your portfolio. It has to survive more market cycles, navigate more inflationary storms, and cover ballooning healthcare costs for a much longer period. For perspective, the estimated lifetime healthcare bill for a 65-year-old couple today is an eye-watering $315,000.

This reality is at the heart of the confidence crisis so many people are feeling. The 2025 EBRI/Greenwald Retirement Confidence Survey found that only 67% of workers feel confident about having enough money for retirement. With the median retirement savings for those aged 55-64 sitting at a meager $185,000, there's a huge gap between where people are and where they need to be—especially for business owners and families with significant assets and legacy goals. You can see more in the full retirement statistics report from Carry.

Planning for a long life means building a resilient portfolio—one designed not just to spit out income, but to preserve and continue growing capital well into your later years.

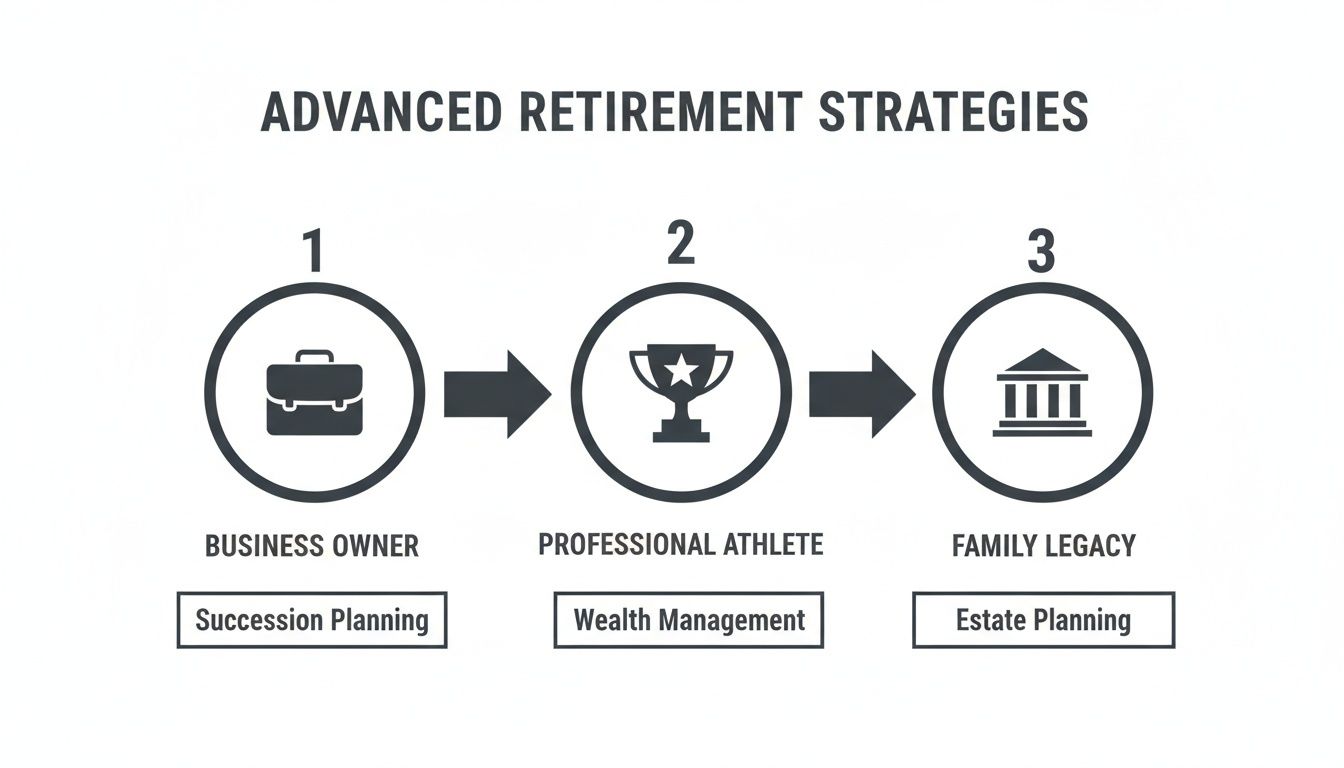

Advanced Retirement Strategies for Unique Careers

When you're a business owner, a pro athlete, or part of a family office, the standard retirement playbook goes right out the window. Your financial world just looks different.

Your income might be lumpy, jam-packed into a few peak years, or mostly tied up in business assets. Because of this, typical retirement advice about saving 15% of your income often misses the mark completely. You need a strategy built for your unique career path—one that’s designed to both create and protect serious wealth.

Supercharged Savings for Entrepreneurs

For business owners, personal and company finances are deeply intertwined. It's a constant balancing act: plowing profits back into the business to fuel growth while making sure you're not neglecting your own future. The trick is to go beyond a simple IRA and use retirement vehicles built for people like you.

These aren't your typical 401(k)s. We're talking about much more powerful tools:

- SEP IRA (Simplified Employee Pension): This lets you sock away up to 25% of your compensation, with a $69,000 cap for 2024. The real beauty is its flexibility; you can dial contributions up or down depending on how the year's cash flow looks.

- Solo 401(k): A fantastic option if you're self-employed with no employees (a spouse is okay!). You can contribute as both the "employee" (up to $23,000 in 2024) and the "employer" (up to 25% of compensation), for a combined total of up to $69,000.

- Defined Benefit Plan: If your business is consistently profitable, this is the heavyweight champion. It lets you make massive, tax-deductible contributions—often well over $100,000 a year—by essentially creating your own private pension plan.

These options are especially critical for anyone navigating the complexities of self-employment. For a deeper dive, check out this guide on how to save for retirement if you're self-employed.

Aggressive Savings for Condensed Careers

If you're a professional athlete or an entertainer, you're facing a unique challenge: your window for peak earnings can be incredibly short. You might be pulling in millions today, but that career could be over by the time you're 35.

This reality makes aggressive saving an absolute must. For you, a 15-20% savings rate isn't nearly enough. A more realistic target is somewhere between 25% to 50% (or even more) of your after-tax income. The whole game is to build the lion's share of your nest egg while your income is at its absolute peak, creating a portfolio big enough to last you for the next 50-plus years.

This front-loaded savings approach is a financial sprint, not a marathon. It requires immense discipline during peak years to set yourself up for a lifetime of security long after the spotlight fades.

This strategy is all about building a fortress against future income uncertainty. It’s about making a few great years fund a lifetime of financial freedom.

Retirement Account Options for High Earners

Choosing the right retirement vehicle can dramatically accelerate wealth-building, especially when you have a high income. Here’s a quick comparison of some of the most powerful options available.

These accounts provide powerful tax advantages that can significantly boost your long-term savings potential beyond what a standard IRA or 401(k) can offer.

Multi-Generational Planning for Family Offices

When we're talking about family offices, the concept of "retirement" expands. It becomes less about funding one person's golden years and more about the sophisticated stewardship of wealth across generations. The entire focus shifts from simple accumulation to long-term preservation.

The strategies here are on another level:

- Trust Planning: Using instruments like Grantor Retained Annuity Trusts (GRATs) or Dynasty Trusts to move wealth down the line efficiently, all while minimizing the hit from estate and gift taxes.

- Tax Minimization: Deploying advanced tactics like tax-loss harvesting, strategically locating assets in different account types, and using charitable giving to shield the family's capital from tax drag.

- Asset Protection: Structuring asset ownership in a way that protects them from creditors or legal challenges, making sure the family's legacy is locked down and secure.

By embracing the right strategies for your specific situation, you can build a financial plan that not only secures your own retirement but can also create a lasting legacy for the generations that follow.

Building Your Personalized Retirement Savings Plan

Once you've defined your goals, wrestled with the key variables, and explored some advanced strategies, it's time to pull it all together. The final step is to craft a cohesive, actionable plan. A truly great retirement strategy isn't something you create once and file away; it's a living roadmap that guides your monthly savings and adapts as your life unfolds.

Answering the big question—"how much should I be saving for retirement each month?"—ultimately boils down to a clear, repeatable process. You need to move beyond a vague idea of "saving more" and land on a specific number grounded in your own ambitions.

That means translating your long-term vision into concrete, near-term actions.

From Vision to Monthly Action

The whole point is to connect the big-picture dream to the practical, everyday habit of saving. It's a straightforward sequence when you break it down.

Here’s a quick summary of how to get to your target number:

- Picture Your Retirement Lifestyle: Start by painting a detailed picture of how you want to live. From there, you can calculate the annual income needed to fund that lifestyle, which gives you your income replacement ratio.

- Calculate Your Total Nest Egg: Armed with your required annual income, you can use a conservative withdrawal rate (like 3-4%) to figure out the total portfolio value you need to build.

- Factor in the Unseen Forces: Don't forget to adjust your numbers for realistic long-term inflation and investment returns. It's also critical to plan for a long life to avoid the risk of outliving your money.

- Choose the Right Accounts: Pick the most effective retirement vehicles for your situation. That might be a Solo 401(k) if you're an entrepreneur or a series of sophisticated trusts for a family office.

- Land on Your Monthly Contribution: With your target nest egg, timeframe, and assumed rate of return, you can work backward to calculate the exact amount you need to save each month to hit your goal.

This process transforms an overwhelming question into a manageable calculation. It provides a clear, data-driven answer you can act on.

Your Plan Must Be a Living Document

One of the most common mistakes I see is people treating their financial plan as a one-time event. But your life, the markets, and your goals are anything but static. Your plan shouldn't be either. Think of it as a dynamic guide that needs regular check-ups to keep you on course.

Life events are obvious triggers for a review. Getting married, having a child, selling a business, or receiving an inheritance are all moments that demand a hard look at your savings strategy. Market conditions also play a huge role; a prolonged bear market or a spike in inflation might mean you need to adjust your savings rate or reassess your portfolio. For a deeper dive on portfolio structure, you can explore the best asset allocation by age to see how it shifts with different risk tolerances.

Key Takeaway: Schedule an annual or semi-annual review of your retirement plan. This disciplined check-in ensures your savings strategy remains aligned with your life and on track to meet your long-term objectives.

The infographic below touches on a few of the specialized strategies that demand this kind of ongoing attention, especially for those with unique career paths.

Whether you're a business owner navigating succession, an athlete with a short earnings window, or a family managing generational wealth, your retirement plan is never a "set it and forget it" tool.

Knowing When to Partner with a Professional

While it's certainly possible to build a basic plan on your own, the complexity that comes with a high-net-worth financial picture often warrants professional guidance. The journey to a secure retirement is littered with intricate decisions that can have multi-million-dollar consequences over time.

As you start building your plan, deciding who to trust with your financial future is critical. Understanding the nuances between a Broker vs Financial Advisor can make all the difference. A true fiduciary advisor helps you navigate the complexities of tax planning, estate considerations, and investment management, making sure all the pieces of your financial life work together seamlessly.

Bringing in a professional isn't a sign of failure. It’s a strategic move to optimize your outcome and gain real confidence in your financial future.

Got Questions About Retirement Savings? We've Got Answers

Even the most meticulously crafted financial plan can leave you with a few nagging questions. That’s just the nature of planning for a future that’s decades away. It’s smart to tackle these common sticking points head-on.

Here are a few of the questions we hear most often from high-net-worth clients trying to dial in their monthly retirement savings number.

How Much Should I Have Saved by Age 40 or 50?

While there's no magic number that fits everyone, financial benchmarks can be a helpful gut check. You’ve probably seen the guideline from Fidelity, which suggests aiming to have 3x your annual salary saved by age 40, and 6x your salary by age 50.

For a high earner making, say, $400,000 a year, that looks like:

- Target by Age 40: $1.2 million in retirement assets.

- Target by Age 50: $2.4 million in retirement assets.

If you’re looking at those numbers and you’re not there yet, don't panic. They're just guidelines. For people with high or lumpy incomes, the real key is focusing on a consistently aggressive savings rate to catch up or even pull ahead.

What's the Difference Between Saving and Investing?

This is a fundamental concept, but it's one that trips up more people than you'd think. The two are not the same, and you absolutely need both.

Saving is all about putting money aside in a safe, easy-to-reach place for your short-term needs. Think of it as your financial safety net. The goal here isn't growth; it's just making sure the capital is there when you need it. A classic example is an emergency fund that covers 3-6 months of your non-negotiable living expenses.

Investing, on the other hand, is about putting your money to work in assets like stocks, bonds, or real estate. The goal is long-term growth. This is how you build real wealth and outpace inflation, but it comes with the unavoidable risk of market ups and downs. Your retirement portfolio is the prime example of investing.

You need both. Savings keep you from having to raid your investments when the car breaks down. Investments are what will actually pay for your retirement.

Should I Pay Off My Mortgage Before I Retire?

The thought of walking into retirement completely mortgage-free is a powerful one. Psychologically, it feels like a massive win, and it slashes your monthly overhead. But the math isn't always so clear-cut.

From a purely financial perspective, it boils down to a simple comparison: your mortgage interest rate versus the potential returns you could get by investing that money instead.

If you’re locked into a low-interest mortgage (think 3-4%) and you're confident your investment portfolio can generate a long-term average return of 7-8%, it might make more sense to keep your money working in the market.

However, if your mortgage rate is higher, or if you just really value the peace of mind that comes with being debt-free, paying it off can be a brilliant move. It's a personal decision as much as a financial one.

Is It Too Late to Start Saving for Retirement?

The best time to start was yesterday. The second-best time is today.

Sure, starting late means you've missed out on years of compounding—the most powerful force in wealth creation. But it doesn't mean a secure retirement is off the table. It just means you have to get serious, and fast.

If you're playing catch-up in your 40s or 50s, you’ll need to ramp up your savings rate dramatically, potentially to 25% of your income or even more. You’ll also want to max out every advantage available, including "catch-up contributions." For 2024, that means people age 50 and over can put an extra $7,500 into their 401(k) and an extra $1,000 into their IRA.

At Commons Capital, we help high-net-worth individuals, families, and business owners find clear answers to these complex questions every day. If you’re ready to move from guessing to having a personalized roadmap for your financial future, we invite you to connect with our team.

Explore how we can help at https://www.commonsllc.com.