Deciding to convert a traditional IRA to a Roth IRA is a strategic financial move that involves paying income taxes on your retirement savings now in exchange for a future of tax-free growth and withdrawals. This can be a powerful wealth strategy, especially for individuals who anticipate being in a higher tax bracket during retirement or wish to leave a tax-free inheritance for their beneficiaries.

Is a Roth IRA Conversion the Right Wealth Strategy for You?

Let's be clear: converting a traditional IRA to a Roth isn't just shuffling papers. It's a major wealth management decision. You're making a calculated trade-off — swallowing a one-time tax bill today for decades of tax-free financial flexibility down the road. This move isn't for everyone, but for the right person, it can be a total game-changer.

This is particularly true for high-net-worth investors, business owners with fluctuating income, and professionals in sports and entertainment. For these individuals, the ability to control when they pay taxes is a significant advantage. By converting during a lower-income year — perhaps between major projects, after selling a business, or before a career jump — you can dramatically reduce that initial tax hit.

The Power of Tax-Free Growth

The real magic of a Roth IRA is its tax treatment. Once your money is converted, it grows completely sheltered from future income taxes. Imagine your investments doubling or even tripling over the next 20 years. In a Roth IRA, that entire gain is yours to keep, tax-free, when you retire.

A great way to think about it is you're paying taxes on the "seed" (your conversion amount) so you can keep the entire "harvest" (all the future growth) without ever owing the IRS another dime. This simple shift can mean having substantially more spendable cash in your retirement years.

To really see the difference, it helps to compare the two account types side-by-side after a conversion takes place.

Traditional IRA vs Roth IRA Post-Conversion

The table makes it obvious: the long-term tax advantages of the Roth are compelling, especially if you can manage the upfront tax cost.

Gaining Control and Simplifying Your Legacy

Another huge win for the Roth is the absence of Required Minimum Distributions (RMDs). With a traditional IRA, you are forced to start withdrawing funds — and paying taxes on them — once you reach age 73. Roth IRAs have no such rule for the original owner.

This gives you two key advantages:

- Greater Control: You can leave your money invested to grow for your entire life, tapping it only if and when you actually need it. This keeps your nest egg working for you and provides a powerful safety net.

- Simplified Estate Planning: When your heirs inherit a Roth IRA, they generally receive the funds completely tax-free. This removes a significant tax headache from your beneficiaries and makes passing on your wealth much cleaner and more efficient.

Before you jump in, it’s critical to understand the full picture of Roth conversion tax implications. A Roth conversion is all about smart, forward-thinking tax planning. It’s a deliberate choice to take control of your tax destiny, locking in a more predictable and tax-efficient financial future for yourself and your loved ones.

Making the Most of Your Conversion in Today's Tax World

When it comes to the decision to convert a traditional IRA to a Roth IRA, timing is everything. We currently find ourselves in a strategic, but likely brief, window of opportunity to pull the trigger on a conversion at a lower tax cost than we will likely see for a long time. It all comes down to understanding how today's tax rates can play to your advantage.

The decision really boils down to one question: Do you want to pay taxes now, at rates that are relatively low, or risk paying them later at unknown — and almost certainly higher — rates? For the high-net-worth individuals, business owners, and sports and entertainment professionals we work with, acting now is simply smart, long-term wealth preservation.

A Closing Window of Tax Opportunity

A huge factor driving the urgency around Roth conversions is the ticking clock on current tax laws. Converting your traditional IRA funds to a Roth before the end of 2025 could lock in the historically favorable tax rates set by the Tax Cuts and Jobs Act (TCJA) of 2017.

As it stands, federal income tax brackets top out at 37%. But after 2025, they’re scheduled to snap back to pre-TCJA levels. That change would push the top rate back to 39.6% and bump lower brackets up, making any future conversions a lot more expensive.

This isn’t just a worry for the wealthiest, either. For example, the 22% bracket for a married couple filing jointly could jump to 25% and kick in at a lower income level. Paying 22% on a conversion today sounds a whole lot better than paying 25% or more on that same amount in a few years.

The core strategy is to pay taxes on your retirement funds while they are "on sale." By converting during this period of lower rates, you are effectively buying tax-free growth for your future at a discount.

The Art of Partial Conversions

For anyone with a hefty traditional IRA balance — we're often talking $500,000 or more — converting the whole thing in one year would be a tax nightmare. That kind of massive, one-time income spike would launch you straight into the highest federal and state tax brackets, completely defeating the purpose of careful tax planning.

This is where partial conversions become an indispensable tool. The idea isn't to convert everything at once. Instead, you convert just enough each year to "fill up" the lower and middle tax brackets without spilling over into the top ones.

Let’s walk through a real-world scenario:

- Client Profile: A married couple, both 60 and recently retired. They’re sitting on $2 million in a traditional IRA, and their other income sources put them in the 12% federal tax bracket.

- The Goal: Shift the IRA to a Roth to create tax-free income for themselves and their heirs, all while keeping the tax hit as low as possible.

- The Strategy: Rather than convert the full $2 million at once, they opt for a series of partial conversions. Each year, they convert around $150,000. This amount uses up their remaining room in the 12% and 22% brackets but stops short of pushing them into the 24% bracket or higher.

By repeating this move over several years, they systematically transfer their assets into the tax-free haven of a Roth IRA. They pay a manageable tax bill each year at a controlled, blended rate instead of getting slammed with a huge, inefficient tax bill in a single year. This methodical approach can literally save hundreds of thousands in lifetime taxes. To play with the numbers for your own situation, our Roth conversion calculator is a great resource.

This forward-thinking strategy is especially powerful for family offices and anyone focused on legacy planning. By converting now, you not only shield your own retirement from future tax hikes but also ensure your wealth can be passed down as a tax-free inheritance, maximizing its impact for the next generation.

How to Execute Your Roth IRA Conversion

Actually starting the process to convert a traditional IRA to a Roth IRA can feel a bit overwhelming, but the mechanics are surprisingly simple once you get the hang of it. If you have a clear plan, you can get it done efficiently and, more importantly, sidestep common mistakes that might stick you with a surprise tax bill.

At the end of the day, it's all about picking the right method for moving the money and fully understanding how your other accounts might affect the final tax bill.

There are really only three ways to get your money from a traditional IRA over to a Roth IRA. They all accomplish the same goal, but each one comes with its own quirks and potential headaches.

Choosing Your Conversion Method

The method you choose dictates how the funds move and how much paperwork you'll have to deal with.

- Trustee-to-Trustee Transfer: This is where your current IRA custodian sends the money directly to your new Roth IRA custodian. You never actually touch the funds, which makes it the cleanest and safest route by far.

- 60-Day Rollover: With this method, your traditional IRA custodian cuts you a check. You then have exactly 60 days to deposit that money into a Roth IRA. If you miss that deadline for any reason, the entire amount could be treated as a taxable distribution, and you might get hit with a 10% early withdrawal penalty. It's a risky game.

- In-House Conversion: If your traditional IRA and Roth IRA are both at the same company (like Fidelity or Schwab), you can usually just ask them to move the assets internally. This is just as easy as a trustee-to-trustee transfer, but it all happens under one roof.

Our strong advice? Stick with the trustee-to-trustee transfer or an in-house conversion. These direct methods completely eliminate the risk of missing that 60-day window. It's a simple mistake that can be incredibly expensive and can wipe out the very benefits you're trying to achieve.

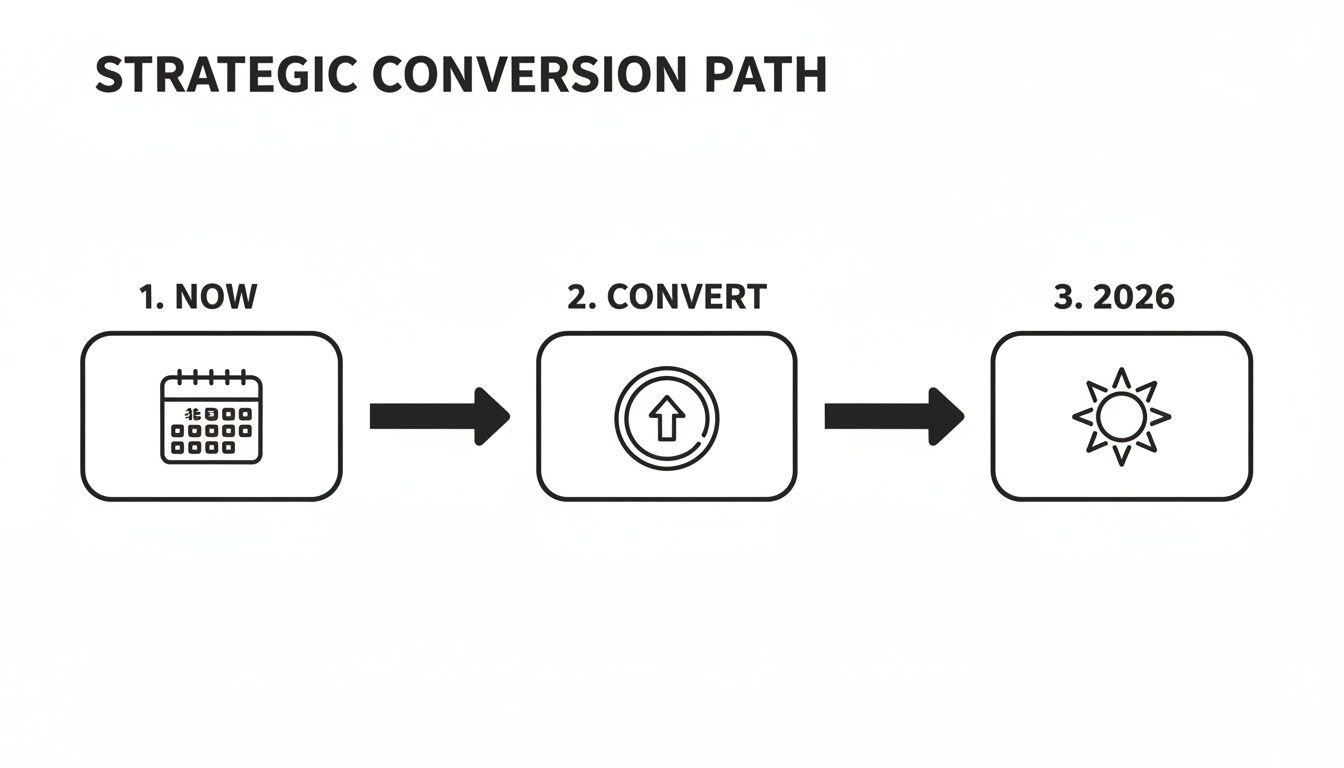

This is a great visual for thinking about the timing. It shows a simplified path for a strategic conversion, highlighting the current window of opportunity before tax laws are expected to change in 2026.

It’s a good reminder that acting now, while tax rates are relatively low, could be a smart move before they're set to go up.

Navigating the Pro-Rata Rule

Okay, here is where a lot of people get tripped up. The pro-rata rule is absolutely critical to understand if you have any after-tax (non-deductible) contributions in any of your traditional, SEP, or SIMPLE IRAs.

Here's the rub: The IRS views all your IRAs (except Roths) as one big pot of money. You can't just cherry-pick the after-tax dollars to convert tax-free. Any conversion you make is considered a proportional mix of your pre-tax and after-tax funds.

Let's walk through a real-world example:

- Total IRA Value: You have $200,000 spread across all your traditional IRAs.

- Basis: Inside that total, $40,000 came from after-tax, non-deductible contributions. This is your "basis." The other $160,000 is a mix of pre-tax contributions and investment growth.

- The Calculation: This means your IRA pool is 80% pre-tax ($160,000 / $200,000) and 20% after-tax ($40,000 / $200,000).

Now, say you decide to convert $50,000 to your Roth IRA. You don't get to just use your $40,000 of after-tax money plus $10,000 of pre-tax money. The pro-rata rule forces you to take a proportional slice.

So, 80% of your $50,000 conversion ($40,000) will be taxable income. Only 20% ($10,000) will be a tax-free return of your basis. This is how people end up with a much larger tax bill than they planned for.

Because of this complexity, many investors find it easier to just convert their entire traditional IRA balance. It ensures all the pre-tax money gets moved and taxed at once, giving you a clean slate for all that future tax-free growth.

Advanced Conversion Strategies for High-Net-Worth Investors

For investors with significant assets, a simple, one-time move to convert a traditional IRA to a Roth IRA is often just the opening act. The real strategic value comes from weaving conversions into a broader, multi-year wealth plan. Sophisticated techniques can unlock benefits that go far beyond basic tax-free growth, especially for anyone planning an early retirement or trying to manage complex income streams.

These advanced methods are a world away from a simple "all or nothing" conversion. They demand precise timing, thoughtful asset selection, and a clear understanding of how all the financial puzzle pieces fit together. For high-net-worth families, business owners, and successful professionals, getting these strategies right is the key to maximizing long-term, tax-free wealth.

Building a Roth Conversion Ladder

One of the most effective tools in the early retiree’s playbook is the Roth conversion ladder. The entire point of this strategy is to create a predictable pipeline of funds you can tap into both tax-free and penalty-free well before you hit age 59½.

Here’s the concept: Every dollar you convert from a traditional IRA to a Roth IRA starts its own five-year clock. Once that five-year period is up, you can withdraw the converted amount (the principal) without owing a 10% early withdrawal penalty. By converting a chunk of money each year, you're essentially building a "ladder," with a new set of funds becoming accessible every year after the first five-year wait is over.

Here’s what that looks like in practice:

- Year 1 (Age 50): You decide to convert $50,000. The five-year clock starts.

- Year 2 (Age 51): You convert another $50,000. A new five-year clock starts on this amount.

- Year 3 (Age 52): You convert yet another $50,000.

- The Payoff: In Year 6, when you're 55, that first $50,000 from Year 1 is now available to you, penalty-free. A year later, the second $50,000 is ready. This creates a reliable, tax-free stream of cash to fund your life before traditional retirement age.

Backdoor and Mega Backdoor Roth IRA Strategies

What happens when you earn too much to contribute to a Roth IRA directly? The IRS has pretty strict income limits, but fortunately, there are well-established workarounds for high-income earners.

- Backdoor Roth IRA: This is the go-to move for individuals whose income is above the threshold. You make a non-deductible (after-tax) contribution to a traditional IRA and then quickly convert that same amount to a Roth IRA. As long as you don't have any other pre-tax money sitting in other traditional, SEP, or SIMPLE IRAs, the conversion itself is usually a tax-free event.

- Mega Backdoor Roth IRA: This is a far more powerful strategy, but it’s only available if your employer’s 401(k) plan has the right features — specifically, it must allow for both after-tax contributions and in-service withdrawals or conversions. If it does, you can contribute money after-tax, far beyond the normal 401(k) limits, and then roll that money directly into a Roth IRA or a Roth 401(k). This can let you funnel tens of thousands of extra dollars each year into a tax-free growth account.

The Mega Backdoor Roth is an absolute game-changer for super-savers. While a standard backdoor might let you sneak in a few thousand dollars, the mega version allows you to put your tax-free savings into overdrive — if your employer’s plan is on board.

Strategic Timing and Asset Selection

Beyond these specific tactics, when you convert and what you convert are just as critical.

Timing Your Conversion

The best time to execute a conversion is almost always during a "gap year" or a period when your income is temporarily lower than usual. Think about the year after you sell a business, a period between jobs, a sabbatical, or those early retirement years before Social Security and Required Minimum Distributions (RMDs) kick in. Converting in one of these income dips means you'll pay the conversion tax at a much lower marginal rate.

Selecting the Right Assets

When you convert, don't just think in terms of cash. It's often far smarter to convert assets with the highest potential for future growth. By moving stocks or funds that you expect to appreciate significantly, you ensure all of that future growth happens inside the tax-free Roth account. You pay the tax on the asset's current, lower value, effectively locking in tax-free gains on all its future performance. This is a powerful way to maximize the long-term benefit of the conversion.

This is a slightly different calculation than for those looking to convert a 401(k) to a Roth IRA, as the investment choices within a 401(k) plan are often more constrained.

When you decide to convert a traditional IRA to a Roth IRA, the immediate tax bill is the obvious hurdle. But for retirees, or those getting close, a much stealthier cost can pop up two years later.

This hidden expense catches people completely by surprise, and it can turn what seemed like a smart tax move into a costly mistake.

The culprit is the Medicare Income-Related Monthly Adjustment Amount, better known as IRMAA. It’s a surcharge tacked onto your Medicare Part B and Part D premiums if your income goes over certain thresholds. And since a Roth conversion counts as ordinary income, a big one can easily push you into IRMAA territory.

The IRMAA Trap: How It Works

Here’s where it gets tricky. Medicare looks at your tax return from two years prior to determine your premiums. This two-year lookback is what trips so many people up. A large conversion you do this year will inflate your modified adjusted gross income (MAGI), and that higher number will be used to calculate your Medicare premiums two years from now.

You might be surprised how low the income thresholds are to trigger IRMAA, especially for those with significant assets. Going just one dollar over a tier can cost you thousands in extra premiums over the year. And it's not a one-time thing — those higher premiums typically stick around for a full 12 months.

The most frustrating part? IRMAA can dramatically inflate the effective tax rate of your conversion. A move you thought was happening in the 22% or 24% bracket could suddenly feel more like 30% or higher once you factor in these delayed surcharges.

How a Conversion Triggers the Surcharges

Let's look at a real-world scenario. The IRMAA surcharges for your 2026 premiums will be based on your 2024 MAGI. The first tier kicks in at $218,000 for joint filers or $109,000 for single filers, potentially adding hundreds of dollars to your monthly premiums for both Part B and Part D.

Imagine a retired couple with a $200,000 MAGI. They decide to make a $50,000 Roth conversion, thinking it's a smart way to fill up their 22% tax bracket. But that conversion pushes their MAGI to $250,000, blowing past the $218,000 threshold and triggering the first tier of IRMAA.

Suddenly, their "22% conversion" costs a lot more once you account for the higher Medicare premiums that will hit them two years down the road. It’s a classic example of why you can't plan for conversions in a vacuum.

Strategies to Stay Under the IRMAA Thresholds

The key to avoiding this expensive surprise is all about proactive planning. It's not that you shouldn't do conversions, but you need to be strategic about the size and timing to keep your income just under that IRMAA cliff.

1. Model Your Income Impact

First, you absolutely have to know your numbers. Before converting a dime, work with your financial advisor to project your MAGI for the year. Tally up everything — pensions, Social Security, investment income — and then run the numbers to see how different conversion amounts will affect your total income.

2. Use "Surgical" Partial Conversions

Instead of one massive conversion, think smaller and more strategic. Once you know the exact IRMAA income tiers, you can convert just enough to fill up your tax bracket while staying a few dollars under the next threshold. This "bracket-filling" approach lets you systematically move money to a Roth without triggering the surcharges.

3. Time Conversions During Low-Income "Gap Years"

The perfect time for conversions is often during your "gap years" — that sweet spot after you retire but before Social Security and Required Minimum Distributions (RMDs) kick in. Your income is naturally lower, giving you more headroom to convert before you risk hitting those IRMAA limits.

For affluent retirees, managing the IRMAA impact isn't a minor detail. It’s a critical step in making sure your decision to convert a traditional IRA to a Roth IRA truly protects your wealth and doesn’t create an expensive, long-lasting headache.

Navigating the Critical Five-Year Rules

When you’re thinking about a Roth IRA conversion, the five-year rules are something you absolutely need to get your head around. They're a common tripwire for even savvy investors, but understanding them is the key to sidestepping penalties and actually getting the benefits you’re after.

There are actually a couple of different five-year rules, but the one we're focused on here governs when you can touch your converted money.

Here's the deal: a separate five-year clock starts ticking for every single Roth conversion you make. Think of it as the IRS's way of preventing people from using a conversion as a quick-and-dirty way to raid their retirement funds early. If you pull out any of your converted principal before its specific five-year clock runs out and you're under age 59½, you'll get hit with a 10% penalty.

Your Conversion Clock and Withdrawal Ordering

It’s really important to know how these clocks work in practice. Thankfully, the IRS has a specific withdrawal order that works in your favor. When you take money out of your Roth IRA, it’s always assumed to come from these sources in this exact order:

- Direct Roth Contributions: Your regular, annual contributions come out first. You can always pull these out tax-free and penalty-free, no questions asked.

- Converted Principal: Next up is the money you converted. This also comes out tax-free (you already paid tax on it during the conversion). But this is where that 10% early withdrawal penalty can bite you if it’s been less than five years since that specific conversion and you're not yet 59½.

- Earnings: The very last dollars to come out are your investment earnings. To get these tax-free and penalty-free, you need to be over 59½ and have had any Roth IRA open for at least five years.

This ordering is a huge deal. It means you can always get to your original contributions first, which gives you a ton of flexibility.

The most powerful takeaway here is that each conversion gets its own five-year holding period. This is what makes strategic "laddering" possible — where you do a series of annual conversions to create a future pipeline of penalty-free funds you can tap into before traditional retirement age.

The five-year rule for converted funds is a persistent source of confusion and costly errors. In fact, IRS data shows that roughly 25% of Roth conversions have early withdrawal attempts that trigger penalties, costing investors an average of $5,000 per incident.

As you map out your own conversion strategy, it pays to dig deeper into this rule and see how it applies to different accounts to stay prepared.

Common Questions on Roth IRA Conversions

Thinking about a Roth IRA conversion always brings up plenty of questions. Let's walk through some of the most common ones we hear from clients to clear up the details.

Can I Convert Just a Piece of My Traditional IRA?

Absolutely. In fact, this is one of the smartest ways to approach a Roth conversion. You don't have to move the entire account balance at once.

Instead, you can execute partial conversions, shifting smaller chunks of money into a Roth IRA over several years. This is a highly strategic move. It gives you precise control over your tax bill, helping you stay in a lower tax bracket each year instead of one massive conversion pushing you into a much higher one. It's also a great way to carefully manage your income to sidestep those pesky Medicare IRMAA surcharges.

Where Should the Money for the Taxes Come From?

This is a critical detail. You should always aim to pay the conversion taxes from a non-retirement account — think a checking, savings, or regular brokerage account.

If you pull money from the IRA itself to cover the taxes, that amount is treated as a withdrawal. If you're under age 59½, you'll likely get hit with a 10% early withdrawal penalty on top of the income tax. Using outside funds also means more of your money gets into the Roth to grow tax-free, which is the whole point.

The cardinal rule is to pay the tax with "outside money." Withdrawing from the IRA to pay the tax defeats a major purpose of the conversion — getting the maximum amount possible into a tax-free growth environment.

Can I Undo a Roth Conversion If I Regret It?

No, you can't. The Tax Cuts and Jobs Act of 2017 did away with the ability to "recharacterize," or reverse, a Roth conversion.

Once you convert funds from a traditional IRA to a Roth IRA, the decision is permanent. This change in the tax code means it's more important than ever to do your homework before you act. Careful planning and modeling the tax impact are non-negotiable.

At Commons Capital, we specialize in guiding clients through complex financial decisions like these. If you're considering a Roth conversion and have investable assets of $500,000 or more, we can help you create a strategy that aligns with your long-term goals. Contact us today to learn how we can help.