Ever heard of a collective investment trust, or CIT? Think of it as a wholesale club for your retirement savings. It's a type of pooled investment vehicle designed almost exclusively for qualified retirement plans, like the 401(k) you have through work. By bundling assets from many different retirement plans, CITs gain institutional buying power, which often translates into significantly lower fees for investors like you.

This cost-saving structure is a big reason why collective investment trusts are becoming such a popular alternative to the mutual funds many of us are more familiar with.

What Are Collective Investment Trusts?

At its heart, a collective investment trust pools money from multiple retirement plans into a single, massive fund. A bank or trust company then manages this fund—or trust—with a specific investment goal in mind, whether that’s tracking the S&P 500 or managing a portfolio for a specific retirement date.

This "strength in numbers" approach is what makes them so cost-efficient. Unlike mutual funds, which are sold to the general public and have to cover hefty marketing and distribution costs, CITs are only available to institutional investors. That focused, no-frills structure allows them to operate with a much leaner expense profile.

To give you a clearer picture, here’s a quick rundown of what defines a CIT.

Collective Investment Trusts at a Glance

This table highlights the key features that set CITs apart. Now, let’s dig into the regulatory side, which is a crucial piece of the puzzle.

The Regulatory Framework

One of the biggest differences between collective investment trusts and mutual funds is who’s watching over them. CITs aren’t registered with the Securities and Exchange Commission (SEC) like mutual funds are. Instead, they fall under the regulation of banking authorities, like the Office of the Comptroller of the Currency (OCC), and must follow strict trust law.

This is a critical distinction. It means you won’t find a CIT with a public ticker symbol you can look up on Yahoo Finance, nor will you get a glossy prospectus in the mail. But don't mistake that for a lack of oversight. The trust structure legally binds the managing bank to act as a fiduciary—meaning they must act in the best interests of the plan participants.

A collective investment trust operates under a fiduciary standard. This means the manager has a legal and ethical obligation to prioritize the financial interests of retirement plan investors above all else, providing a foundational layer of protection for your savings.

The industry has seen explosive growth, which speaks volumes about its increasing appeal. The collective investment trust market in the U.S. has ballooned to over $6.1 trillion in assets under management. This surge signals a clear trend: plan sponsors are actively looking for more cost-effective ways to help their employees save for retirement.

Understanding the Valuation

To grasp how a CIT is valued, you need to understand a core concept in the fund world: its Net Asset Value (NAV). The NAV is simply the per-share market value of the fund, calculated once at the end of each trading day. This daily pricing keeps things transparent and ensures fair valuation for all the retirement plans invested in the trust.

While CITs serve a specific corner of the market, they operate in ways that are similar to other financial products, including various types of alternative investments. If you're curious to learn more, you can check out our guide that explains in detail what is an alternative investment.

How Collective Investment Trusts Work

To really get a feel for collective investment trusts, it helps to look under the hood. The best way to think of a CIT is as a meticulously engineered vehicle designed for one specific purpose: efficiently managing retirement assets. It isn't something just any investment firm can launch; a bank or trust company must establish and maintain it, stepping into a critical legal role.

That bank acts as the trustee and primary fiduciary. This is a massive distinction from most other investment products. As a fiduciary, the bank is legally required by the Employee Retirement Income Security Act of 1974 (ERISA) to act solely in the best interests of the retirement plan participants. It's a powerful layer of investor protection that's hardwired right into the CIT’s structure.

The Role of the Trustee and Plan Sponsor

The trustee's job is all-encompassing. They handle everything from managing the trust's investments to keeping up with regulatory compliance. They are the ultimate stewards of the assets, legally on the hook for safeguarding the money and hitting the stated investment goals.

On the other side of the table is the plan sponsor—the company offering the 401(k) or other retirement plan. The sponsor’s own fiduciaries are responsible for selecting and monitoring the investment options they make available to their employees. When they add a CIT to the menu, they are effectively entrusting their employees' retirement savings to the bank that manages that trust.

The whole process usually unfolds like this:

- Establishment: A bank or trust company creates a CIT with a specific investment strategy, like tracking the S&P 500 or managing a target-date fund.

- Due Diligence: A retirement plan sponsor vets the CIT, checking its performance, fees, and whether it’s a good fit for their employees.

- Adoption: If it all checks out, the sponsor signs a participation agreement and officially adds the CIT to their plan’s investment lineup.

- Participant Investment: Employees can then put a portion of their 401(k) contributions into the CIT, just as they would with a mutual fund.

Fiduciary Oversight and Investment Goals

This fiduciary framework is the bedrock of how CITs operate. Unlike mutual funds—where managers aren't typically subject to ERISA’s tough fiduciary duties for the funds they run—CIT trustees operate under a standard of care that courts have called the "highest known to the law."

A key feature of the CIT structure is its tailored oversight. The entire regulatory framework, from banking laws to ERISA, is designed specifically for the retirement plan market, ensuring that every decision is aligned with the long-term financial well-being of plan participants.

This singular focus allows for incredible precision. Because CITs aren't marketed to the general public, they can be customized to meet the very specific needs of institutional investors, which is a huge advantage.

For instance, a large corporation might partner with a trust company to build a custom target-date CIT series designed around its unique employee demographics. Another might simply pick an off-the-shelf CIT that passively tracks a bond index at an extremely low cost. This blend of customization and strict fiduciary oversight makes collective investment trusts a powerful and secure tool for building a rock-solid retirement plan.

The Key Advantages of Investing in CITs

The rise of collective investment trusts isn't some fleeting trend. It’s a direct result of powerful advantages that perfectly align with what long-term retirement savers need. Both plan sponsors and their employees are catching on, recognizing that CITs offer a compelling mix of efficiency, oversight, and flexibility.

The most talked-about benefit—and for good reason—is their incredible cost-efficiency. This isn't just a small perk; it’s a core feature that can dramatically change how much a participant has saved by the time they retire.

A Focus on Lower Costs

Unlike mutual funds, which are sold to the general public, CITs are built exclusively for institutional retirement plans. That single distinction makes all the difference.

CITs don't have to spend a dime on splashy public marketing campaigns, large sales teams, or the glossy prospectuses you get in the mail. They simply operate on a much leaner model, sidestepping many of the administrative and distribution costs baked into a mutual fund's expense ratio. Those savings get passed directly to the retirement plan and its participants.

Over an investor's career, the power of lower fees is immense. Even a tiny difference in an expense ratio compounds over decades, potentially adding tens or even hundreds of thousands of dollars to a final nest egg.

This cost advantage is a huge reason why CITs now dominate popular strategies like target-date funds (TDFs). In fact, CITs now hold about $2.02 trillion in TDF assets, pulling ahead of mutual funds, which hold $1.95 trillion.

This shift shows just how seriously fiduciaries take cost savings. Research has found that a mere 1% increase in fees can wipe out more than $280,000 of a participant's savings over a 35-year career.

Flexibility in Design and Fees

Beyond their low-cost structure, CITs bring a level of flexibility that plan sponsors love. Since they aren't one-size-fits-all products for the retail market, they can be designed with very specific investment goals in mind.

What’s more, larger retirement plans can often negotiate fees directly with the trust company. This creates a competitive landscape where plans with significant assets can lock in even lower expense ratios—an option that’s almost unheard of with retail mutual funds. This flexibility is a critical part of managing portfolio costs, a topic you can learn more about in our guide to understanding investment management fees.

This adaptability allows sponsors to build smarter, more efficient investment lineups for their employees. Here’s how that flexibility plays out:

- Custom Mandates: A large plan can work with a bank to create a CIT with a unique investment mandate built just for its participant demographics.

- Tiered Pricing: Fee structures can be scaled, offering lower costs as the plan's assets in the CIT grow.

- Negotiated Rates: Direct negotiation lets large plans use their size to secure institutional pricing that benefits every single participant.

Robust Fiduciary Oversight

Another major advantage of CITs is the fiduciary protection that’s baked right in. The bank or trust company managing a CIT is legally required by ERISA to act as a fiduciary. In simple terms, this means they must always act in the best interests of the plan participants.

This provides a powerful layer of oversight that you don't automatically get with mutual funds, whose managers typically aren't held to ERISA's strict fiduciary standard. This legal duty ensures every decision, from picking investments to managing fees, is made with one goal in mind: benefiting the retirement savers. For those exploring broader strategies for finding investment opportunities, understanding the value of built-in protections like these is key to evaluating any investment vehicle.

CITs Versus Mutual Funds: A Head-to-Head Comparison

When it comes to building a retirement plan, the choice between collective investment trusts and mutual funds is a common crossroads for plan sponsors. While both pool investor money to buy securities, that’s where the similarities end. Their underlying structures, costs, and the rules they play by are worlds apart.

At its core, the difference is simple. Think of a mutual fund as a retail product you'd find on a shelf at a big-box store—available to everyone, with marketing and distribution costs baked in. A CIT, on the other hand, is more like a wholesale product sold directly to businesses—in this case, exclusively for institutional retirement plans. That streamlined model allows it to operate far more efficiently.

Regulation and Oversight

One of the biggest distinctions is who’s watching over them. Mutual funds are registered with the Securities and Exchange Commission (SEC) under the Investment Company Act of 1940. This puts them under a microscope, requiring strict public disclosures, a detailed prospectus, and making them available to any retail investor.

CITs follow a different path. They are regulated by federal or state banking authorities, like the Office of the Comptroller of the Currency (OCC). More importantly, they fall under the Employee Retirement Income Security Act of 1974 (ERISA). This isn't just a technicality; ERISA imposes a strict fiduciary duty on the managing trustee, legally obligating them to act solely in the best interests of the plan participants. It's a powerful, built-in layer of protection.

Fee Structures and Cost Efficiency

This split in regulation has a direct and significant impact on cost. Because CITs aren’t marketed to the general public, they get to sidestep a lot of the expenses that come with running a mutual fund.

These avoided costs include:

- Marketing and advertising budgets

- SEC registration fees

- Public shareholder servicing expenses

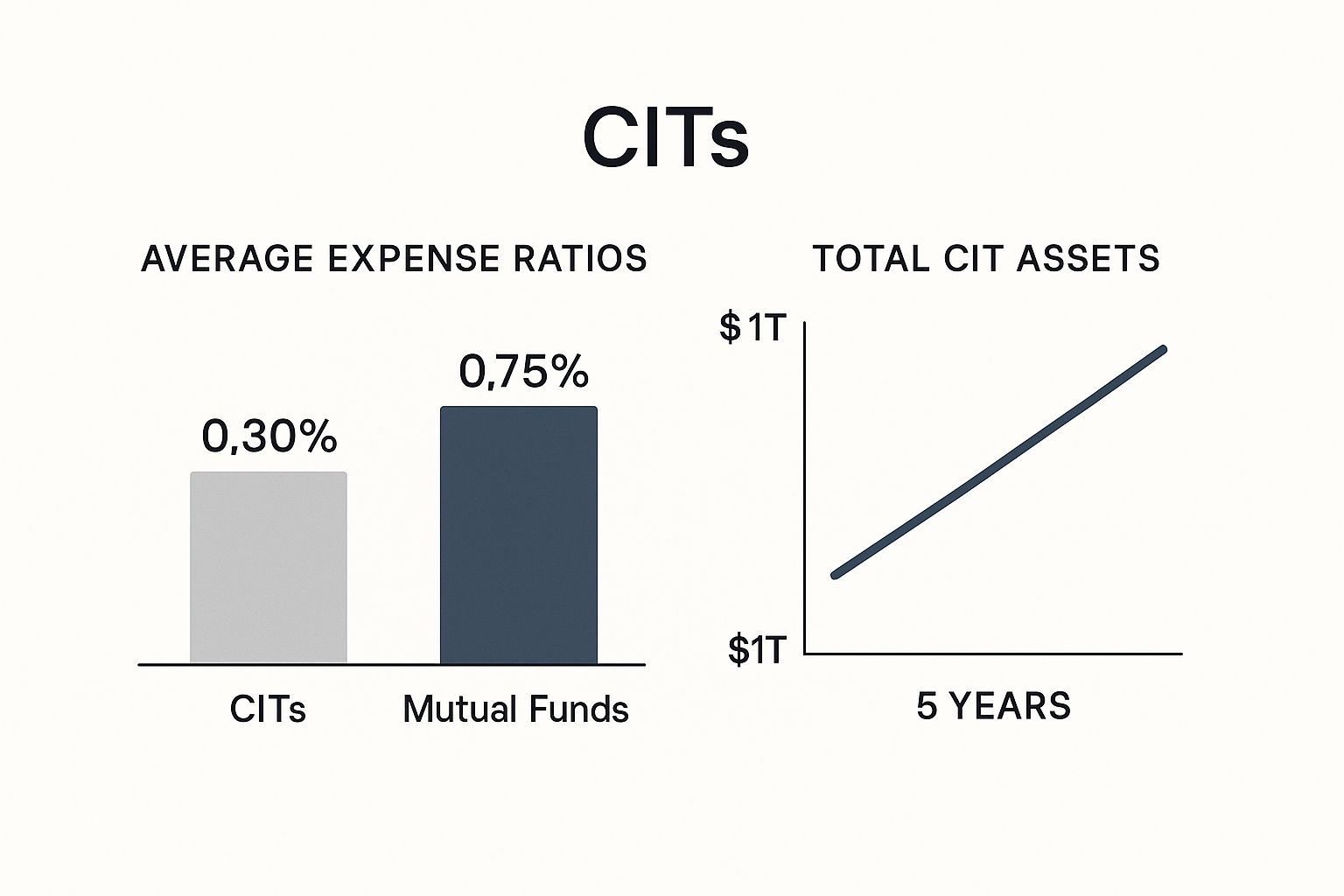

Those savings get passed right back to the retirement plan and its participants, and the difference can be dramatic. According to Morningstar, when you compare similar investment strategies, CITs are cheaper than their mutual fund counterparts an incredible 88% of the time. For plan sponsors who are also looking into alternative assets, the cost advantages of CITs make other institutionally-focused products, like those detailed in our overview of direct lending funds, even more appealing.

This infographic paints a clear picture of just how stark the cost differences are and why CITs have become so popular.

As the data shows, CITs don't just offer lower fees; they're also attracting a huge and growing slice of retirement assets.

Transparency and Availability

Years ago, a common knock against CITs was their supposed lack of transparency. Since they don’t have public ticker symbols, you can’t just look them up on Yahoo Finance. But that’s largely an outdated view.

Today, Department of Labor regulations require plan sponsors to give participants standardized disclosures for all investment options, CITs included. These reports detail everything that matters: performance, benchmarks, and fees.

While mutual funds offer public visibility via ticker symbols, CITs deliver essential transparency directly to the plan and its participants through standardized fact sheets and federally mandated disclosures, ensuring fiduciaries have the data they need to make informed decisions.

This direct-to-plan reporting gives fiduciaries all the necessary information without the overhead of public reporting.

To make it even clearer, here’s a simple table breaking down the key differences between these two investment vehicles.

Collective Investment Trusts vs. Mutual Funds: Key Differences

This table offers a side-by-side look at what truly separates CITs and mutual funds, helping plan sponsors quickly see which structure might better align with their goals.

As you can see, while both aim to grow capital, their design and purpose are fundamentally different. For retirement plans focused on cost-efficiency and fiduciary responsibility, the advantages of a CIT are hard to ignore.

What Are the Downsides? A Clear-Eyed Look at CIT Risks

While collective investment trusts bring some serious benefits to the table, especially on costs, they aren't a perfect fit for every situation. Like any investment vehicle, they have their own quirks and limitations that you need to understand before diving in. Knowing where they shine—and where they don't—is key to making a smart decision.

First off, CITs are exclusive. You can't just go out and buy one in your brokerage account like you would a mutual fund. They're built specifically for qualified retirement plans, think 401(k)s and pension funds. That means individual investors can't access them directly.

The Transparency Question

In the past, CITs got a bit of a bad rap for being opaque. Because they aren't registered with the SEC and don’t have a public ticker symbol, you can't just punch them into a financial news site to check their daily performance. For anyone used to the constant, real-time feedback of mutual funds, this can feel like a step backward.

But a lot of that is old news. Today, the Department of Labor has rules in place that require standardized disclosures for all plan investments, CITs included.

Participants get detailed fact sheets and disclosure documents that lay out everything: the CIT's performance, expense ratios, investment goals, and all its holdings. This gives fiduciaries and employees all the info they need to make a solid decision, even without a ticker symbol.

Even so, the lack of public reporting is a fundamental difference. If you're an investor who loves to do your own independent research and track funds on public websites, this aspect of CITs might feel like a genuine drawback.

Liquidity and Taking It with You

Another thing to think about is what happens when you leave your job. While CITs are priced every day just like mutual funds, they have one major limitation: you can't roll them over "in-kind" to an IRA or your next company's 401(k).

This forces your hand. You have to liquidate your holdings in the CIT—basically, sell your units for cash—before you can roll the money into your new account. For a long-term investor, this might not seem like a big deal, but it does create a couple of snags:

- Time on the Sidelines: You'll be out of the market for a brief period between selling the CIT and reinvesting the cash. That time lag could mean missing out on market gains.

- Starting Over: Instead of a simple transfer, you have to actively choose new investments for your IRA or new 401(k).

This small detail really highlights the institutional DNA of a collective investment trust. It’s built for the plan, not necessarily for the individual investor's portable portfolio. That distinction becomes crystal clear the moment you change jobs. Understanding these realities is crucial for getting the full picture of how CITs really work.

Where Collective Investment Trusts Are Headed

The world of collective investment trusts is quietly undergoing a major shift. What was once an exclusive tool for the largest corporate retirement plans is now breaking into the mainstream, thanks to a potent mix of surging demand and newfound accessibility. This isn't just a minor trend; it's a fundamental change positioning CITs as a dominant force in the future of retirement investing.

A big part of this story is the growing adoption of CITs by smaller retirement plans. For years, steep investment minimums kept these vehicles out of reach for small businesses. Now, as those barriers have fallen—or disappeared altogether—even the smallest companies can tap into the institutional-grade pricing and fiduciary oversight that CITs provide. It’s a leveling of the playing field, plain and simple.

Pulling Back the Curtain on Transparency

Perhaps the most significant change shaping the future of CITs is the industry-wide push to shed their old reputation for being opaque. The long-standing criticism of CITs as a "black box" is fading fast, as new platforms and reporting standards bring them into the light.

Take the Nasdaq Fund Network, for example. This service now offers daily performance data and key fund information for a growing number of CITs. This makes it far easier for plan sponsors and their advisors to analyze and monitor these trusts right alongside their mutual fund counterparts. This move toward greater visibility is tackling one of the last major hurdles to wider adoption.

The ongoing evolution in transparency isn’t just about data; it’s about confidence. By making performance and holdings information more readily available, the industry is building greater trust among plan fiduciaries and participants, solidifying the role of collective investment trusts as a mainstream retirement solution.

This shift is also part of a larger global embrace of well-regulated, collective investment structures. The market for these vehicles is booming worldwide. Luxembourg, a major hub for investment funds, recently reported total net assets of EUR 5,950 billion, a 5.52% jump in just one year. This global reliance on collective vehicles just goes to show how critical they are for meeting diverse investor needs. You can dig into more details on the global situation of collective investment undertakings.

Expanding into New Territory

Looking ahead, one of the most exciting developments is the potential for CITs to move into other types of tax-advantaged savings plans. Right now, bipartisan legislation is on the table to allow 403(b) plans—the retirement accounts used by teachers, non-profits, and healthcare workers—to invest in CITs.

If this legislation passes, it would be a game-changer. It could unlock a massive new market and bring the cost-saving power of CITs to millions more American workers, representing one of the most significant expansions for these trusts in decades. All signs point in one direction: collective investment trusts aren't just here to stay; they're actively building a more efficient and cost-effective future for retirement savers everywhere.

A Few Common Questions About CITs

When you start digging into the world of retirement investing, you're bound to have some questions—especially about powerful but less common options like collective investment trusts. Here are a few of the most frequent things we hear from plan participants and fiduciaries.

So, Who Can Actually Invest in a CIT?

This is usually the first question people ask, and it gets to the heart of what makes a CIT different. Unlike mutual funds that are open to the public, CITs are built exclusively for qualified retirement plans.

Think of them as a private club for institutional investors. You can’t just open a brokerage account and buy one. Access is limited to plans like:

- 401(k)s

- Defined benefit pension plans

- Certain government retirement plans

Bottom line: Your ability to invest in a CIT depends entirely on whether your employer has decided to include one in your company's retirement plan lineup.

How Do I See How a CIT Is Performing?

Another common sticking point is tracking performance. You won't find a ticker symbol for a CIT on public market websites, which can be confusing at first. But that doesn’t mean the information is hidden.

The Department of Labor requires plan sponsors to give participants clear, standardized disclosure documents for every investment option.

This is your go-to source. You should receive a detailed fact sheet that lays out the CIT's investment goals, historical performance (usually compared to a benchmark), its expense ratio, and its top holdings. It’s all there to help you make an informed choice.

And to make things even easier, most plan recordkeeper websites now display all of this information right inside your online retirement account portal, so you can check in on your investments anytime.

What Do Plan Sponsors Look for When Picking a CIT?

A plan sponsor has a fiduciary duty to act in the best interests of their employees, which means their selection process for any fund is incredibly thorough. They aren't just hunting for the cheapest option; they’re looking for the best overall value for everyone in the plan.

Here’s a peek into their decision-making process. They’re weighing several key factors:

- Cost-Effectiveness: The expense ratio is a huge deal. They’ll put a CIT’s fees head-to-head with similar mutual funds to see where the value is.

- Performance Track Record: Fiduciaries want to see a solid history. Has the CIT consistently met or beaten its benchmark over the long run?

- Manager Expertise: They dig into the bank or trust company running the fund. They want to see a stable team, a sound investment philosophy, and deep experience.

- Alignment with Plan Goals: Does the CIT’s strategy fit the plan’s overall mission and the needs of its employees? A fund that’s perfect for a young tech startup might not be right for a company with an older workforce nearing retirement.

In the end, the goal is always to find high-quality, low-cost collective investment trusts that give participants the best possible shot at reaching their retirement goals.

At Commons Capital, we specialize in helping high-net-worth individuals and families navigate complex financial landscapes. If you're looking to optimize your financial strategy and achieve your long-term goals, we invite you to explore our tailored wealth management services. Learn more about how we can help at https://www.commonsllc.com.