What are direct lending funds? In simple terms, these specialized investment vehicles provide capital directly to businesses, bypassing the traditional banking system. Think of them as bespoke financial partners for companies that are often caught in the middle—too large for a standard small business loan but not quite big enough to tap into public debt markets. This guide explores how they operate and their growing role in modern finance.

The Rise of Private Credit and Direct Lending

Let's paint a picture. Imagine a successful, mid-sized manufacturing company that needs a significant cash infusion to build a new factory or acquire a smaller competitor. A decade or two ago, their first call would have been to a major commercial bank.

However, the financial world has changed dramatically, especially since the 2008 financial crisis. New, stricter regulations made it more difficult and expensive for banks to lend to all but the most blue-chip companies. As a result, many banks pulled back from lending to the middle market, leaving a massive financing gap.

Filling the Void Left By Banks

This is precisely where direct lending funds saw their opportunity and stepped in to fill that void. As a major component of the burgeoning private credit market, these funds do not operate under the same heavy regulations as traditional banks. They pool capital from sophisticated investors like pension funds, university endowments, insurance companies, and high-net-worth individuals.

Armed with this capital, the fund’s managers effectively act as the bank. They source promising companies, perform rigorous risk evaluation (underwriting), and manage the loans themselves. This direct relationship often leads to more flexible terms and faster financing for businesses that desperately need it.

By providing customized debt solutions, direct lending funds have become an essential engine for growth in the middle-market economy, funding everything from acquisitions to operational improvements.

As the private credit market has matured, direct lending funds have become crucial business loan alternatives for companies seeking more than a one-size-fits-all loan. Their ability to tailor terms to a borrower's specific needs is a significant part of their appeal.

To better understand their unique position, let's compare them side-by-side with traditional bank loans.

Direct Lending Funds vs. Traditional Bank Loans

This table offers a clear comparison, highlighting the key differences in how direct lending funds and traditional banks approach business financing.

As you can see, it's a trade-off. Businesses gain speed and flexibility but typically pay a higher interest rate for this tailored financing.

Understanding Their Role In Modern Finance

Direct lending is a form of private debt, which itself is a major category within what are known as alternative investments. This category includes asset classes outside of public stock and bond markets, such as private equity and real estate. Understanding this context helps explain why so many sophisticated investors are drawn to this space.

Ultimately, these funds serve two distinct purposes:

- For businesses: They provide access to vital capital with terms that are often far more adaptable than what a bank can offer.

- For investors: They offer the potential for attractive, steady income that is not necessarily tied to the volatile swings of the public markets.

Now, let's dive deeper into how these funds actually work, the benefits they offer, and the risks you need to keep in mind.

How a Direct Lending Fund Actually Works

So, how does one of these funds really operate day-to-day? To get a real feel for direct lending funds, you have to look under the hood at the engine. While the concept of lending money is straightforward, the process within a fund is a carefully orchestrated journey, from raising capital to putting it to work.

It all begins with fundraising. The fund manager—the expert at the helm—reaches out to potential investors to secure capital commitments. These are not average retail investors; the participants are typically large institutions like pension funds, insurance companies, and university endowments, along with wealthy individuals and family offices seeking alternative income streams. This is a long-term partnership where investors commit capital that the manager can "call" upon when a suitable lending opportunity arises.

Once a substantial pool of capital is committed, the real work begins.

Sourcing and Vetting Potential Borrowers

The absolute core of a direct lending fund’s operation is deal sourcing and origination. Fund managers don’t just wait for businesses to call. They actively build and leverage a deep network of contacts—including private equity firms, investment banks, and M&A advisors—to find promising middle-market companies that need financing and either can't or prefer not to get it from a traditional bank.

When a potential borrower is identified, the fund’s team initiates an exhaustive due diligence process. This goes far beyond a simple credit check. The team dives deep, analyzing the company from every angle:

- Financial Health: They scrutinize financial statements, examining everything from revenue streams and profit margins to cash flow and existing debt.

- Business Model: How strong is their market position? Is the management team solid? Does the business have long-term viability?

- Growth Prospects: Why do they need the loan? The team evaluates the specific purpose, whether it’s for an acquisition, operational expansion, or a major recapitalization.

This intense vetting is all about minimizing credit risk—the very real possibility that a borrower won’t be able to repay their loan. This is where a skilled fund manager earns their fees and proves their value to investors.

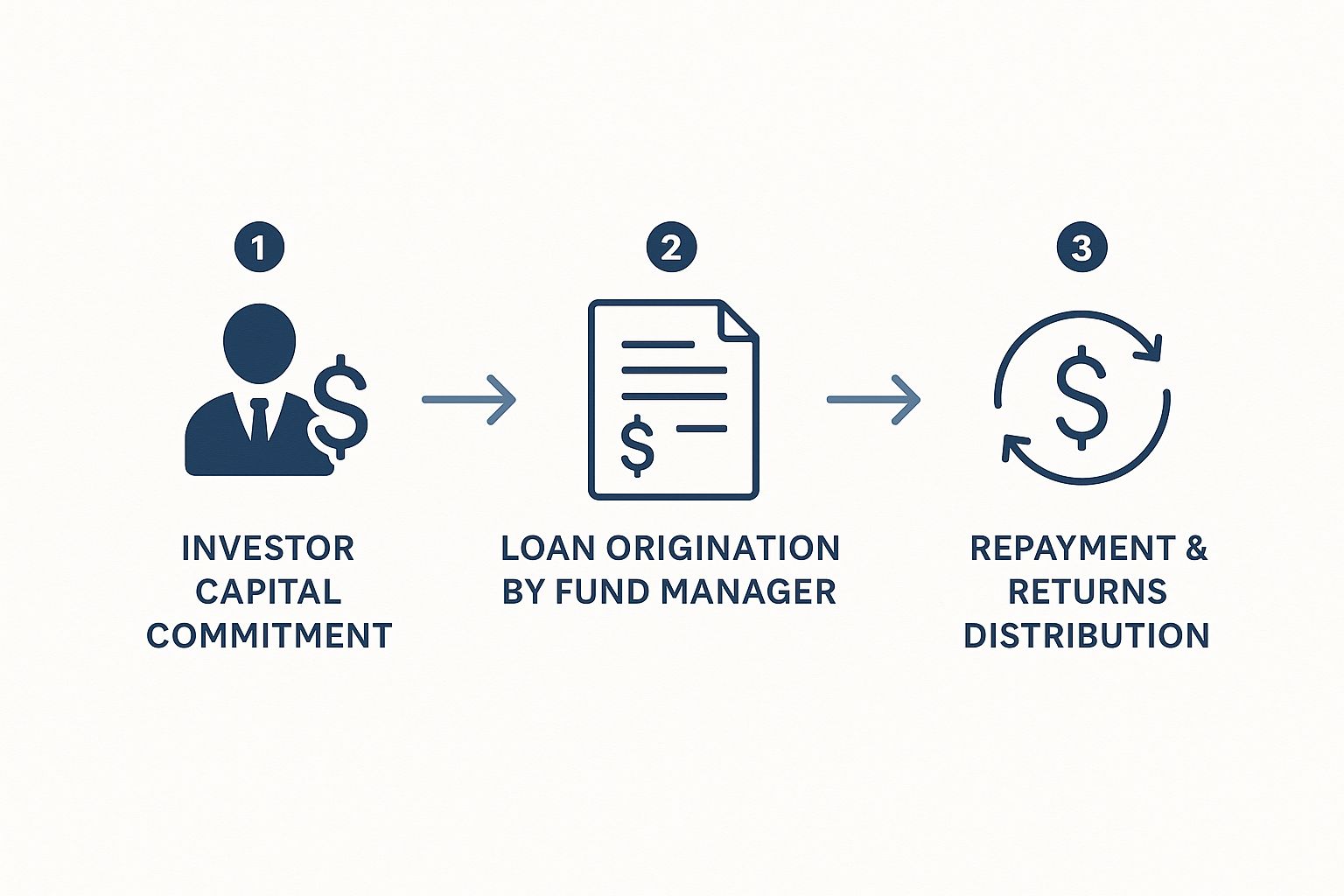

The entire cycle, from raising capital to generating returns, is a continuous flow.

This image provides a bird's-eye view of the process. You can see how investor capital is converted into loans, which then produce interest and principal payments that flow back to investors as returns.

Structuring the Loan and Monitoring Performance

Once a borrower receives the green light, the next stage is loan structuring. This is where the direct lending model truly excels. Unlike the rigid, one-size-fits-all loans from a large bank, a direct lender can tailor every detail of the loan to match the borrower's unique circumstances and the fund's risk tolerance.

During this phase, they negotiate the key terms:

- Interest Rate: Often a floating rate, typically a benchmark like SOFR plus an additional percentage (the "spread"), for example, SOFR + 6%. This structure helps shield investor returns from the impact of inflation.

- Covenants: These are financial guardrails or protective clauses requiring the borrower to maintain certain performance metrics, such as a specific debt-to-EBITDA ratio. Covenants serve as an invaluable early warning system if a company begins to struggle.

- Repayment Schedule: This outlines precisely when and how the principal and interest will be repaid over the life of the loan.

However, the fund manager's job doesn't end once the deal is signed and the money is transferred. In fact, it's just beginning. From that point on, they are in a constant portfolio monitoring mode.

This active management involves regular check-ins with the company's leadership, reviewing quarterly financials, and ensuring all loan covenants are being met. It’s a hands-on approach that allows the manager to identify potential issues early and work with the borrower to resolve them before a default becomes a serious risk.

For investors, the final piece is receiving returns. As borrowers make their interest payments, that cash flows into the fund and is then distributed to investors, typically on a quarterly basis. The fund manager earns a management fee for this work, and often a performance fee if the fund performs well, aligning everyone's interests toward success.

The Global Market for Direct Lending

Direct lending isn't just a niche trend—it's a global force that has fundamentally reshaped how businesses access the capital they need to grow. What started as a small, specialized strategy has exploded into a major pillar of the financial world.

This growth is not accidental. It's the result of a perfect storm: mid-sized companies are perpetually hunting for funding, while investors are simultaneously searching for reliable, attractive returns. To truly grasp why direct lending funds are so significant today, you must understand the sheer size and momentum of this market. It is no longer an "alternative"; it's a core part of the global credit system.

North America: The Undisputed Leader

When it comes to direct lending, North America is the largest and most mature market. The growth here has been staggering. Between 2010 and 2024, the market more than tripled, swelling to an estimated $1.5 trillion in assets under management (AUM). Projections suggest it could reach $2 trillion by the end of the decade.

This market is no longer exclusive to large institutional players like pension funds. The investor base has broadened significantly.

A major reason for this expansion is the rise of Business Development Companies (BDCs). These are publicly-traded vehicles that essentially provide everyday investors with a ticket into the private credit world.

By 2024, BDC assets under management in North America surpassed $300 billion. That figure alone demonstrates how much they have done to make this asset class more accessible.

Europe and Asia Are Catching Up Fast

While North America leads, Europe is following closely. The European direct lending scene is rapidly maturing, with AUM estimated between $500 billion and $1 trillion. The story is much the same: as traditional banks retreat from lending to mid-sized companies due to tighter regulations, private credit funds are stepping in to fill the gap.

The Asia-Pacific region is at an earlier stage, but its potential is enormous. It's currently a smaller market—around $28 billion in AUM for developed Asia—but the runway for growth is extensive. As these economies continue to expand, the demand for flexible, non-bank financing will only increase, setting the stage for direct lending to flourish.

While our focus is on corporate debt, it's insightful to examine dynamics in other areas like the personal loans market to get a comprehensive picture of private credit's reach.

Key Factors Fueling the Global Expansion

What is fueling this global growth? A few powerful forces are working in concert to drive the worldwide expansion of direct lending.

- Investors Are Chasing Yield: Traditional fixed-income investments have offered low returns for years. Direct lending gives investors the opportunity to earn higher, more compelling yields. Additionally, most of these loans have floating rates, which acts as a built-in hedge against inflation.

- Companies Always Need Capital: The middle market is the engine of most economies, and that engine requires fuel. These companies constantly need cash for acquisitions, expansion, and day-to-day operations. Direct lenders have become a go-to source.

- Speed is a Competitive Advantage: When a company is trying to close an acquisition or seize a strategic opportunity, time is of the essence. Direct lenders can move much faster and with more certainty than traditional banks, which are often slowed by bureaucracy.

This powerful combination of factors makes it clear that direct lending is not a passing fad. It is a permanent, structural part of the global financial system, connecting investors who have capital with growing businesses that need it.

Why Investors and Businesses Choose Direct Lending

So, why has direct lending exploded in popularity? It's not just that banks have pulled back. The real story is that these funds offer a win-win for both investors seeking steady income and businesses that need flexible capital to grow.

Direct lending fills a gap left by traditional finance, creating a powerful synergy. Borrowers get the customized financing they can't find elsewhere, and investors get access to a unique investment with attractive return potential. It is this two-sided appeal that is fueling the market's incredible expansion.

Let's unpack what makes it so compelling from each perspective.

The Investor's Perspective: Attractive Yields and Diversification

For investors, the primary attraction is clear: the opportunity to earn higher, more predictable returns than what is typically available in public debt markets. The yields from direct lending funds often outshine those from broadly syndicated loans or high-yield bonds.

Of course, that extra return comes at a price—it's the trade-off for tying up capital in less liquid, more complex private loans. But for those building an income-focused portfolio, the features are hard to ignore.

- Floating Interest Rates: The vast majority of these loans have floating rates, meaning they adjust with the market. This acts as a natural buffer against inflation. When interest rates rise, so does the income from these loans, helping to protect purchasing power.

- Lower Volatility: Since these loans are not traded on public exchanges, they aren't subject to the daily mood swings of the stock and bond markets. This can lead to a smoother investment experience and less volatility in an overall portfolio.

- True Diversification: Private credit tends to have a low correlation to traditional stocks and bonds. Adding a slice of direct lending can genuinely improve a portfolio's risk-adjusted returns. It's interesting to see how this debt-focused approach compares to various private equity investment strategies, which focus on taking ownership stakes.

Put it all together, and you get a source of consistent, contractual cash flow. The returns are generated from regular interest payments, creating a steady income stream that can be a fantastic anchor in a well-rounded investment plan.

The Borrower's Perspective: Speed, Certainty, and Flexibility

Now, let's look at the other side. For the middle-market companies that are the backbone of our economy, working with a direct lender can be a game-changer. Many find the traditional bank loan process to be painfully slow, inflexible, and fraught with uncertainty. Direct lenders are designed to solve these exact problems.

The primary advantage is obtaining financing that is actually built for their specific needs. Banks tend to use one-size-fits-all underwriting models and often become hesitant when a company has a complex history or is pursuing a strategic acquisition.

A direct lender, on the other hand, operates differently, offering:

- Speed of Execution: In a fast-moving M&A deal, waiting is not an option. Direct lenders have nimble teams and streamlined approval processes. They can deploy capital in weeks, not the months it can take with a bank.

- Certainty of Close: When a direct lender gives a thumbs-up, you can be confident the money will be there. That level of certainty is invaluable for a business owner trying to execute a major growth plan.

- Customized Solutions: This may be the single biggest advantage. Direct lenders are renowned for their flexibility. They can craft loan terms—covenants, repayment schedules, and more—that fit the borrower's business cycle and cash flow. It’s a true partnership, a world away from the rigid, impersonal nature of big-bank lending.

Weighing the Pros and Cons for Investors

While the benefits are compelling, it's crucial to approach direct lending with a clear-eyed view of both the upsides and potential downsides. No investment is without its trade-offs.

Here’s a balanced look at what investors should consider before allocating capital to this asset class.

Ultimately, a direct lending fund can be a powerful tool for the right investor, but understanding this balance is the first step toward making an informed decision.

Navigating the Risks of Private Credit

While direct lending funds appear attractive, it's crucial to approach them with your eyes wide open. Like any investment, they come with a unique set of risks. Ignoring these risks is not an option if you want to make prudent decisions in the private credit market.

The risks here are different from those in the public stock market. We're talking about the challenges inherent in private, negotiated deals held for the long term. Understanding these specific hurdles is the first step toward building a solid private credit allocation.

Let's pull back the curtain on the main risks you need to consider.

The Challenge of Credit Risk

At its core, lending is all about credit risk—the chance that the borrower cannot repay the loan. It is the most fundamental risk of all. Since direct lending focuses on middle-market companies, which can be more vulnerable during economic downturns than large corporations, this risk is always front and center.

A borrower can get into trouble for various reasons, from a sudden industry shift to poor business decisions. This is where a fund manager truly earns their keep. Their ability to perform deep due diligence and properly vet a company’s financials, market position, and leadership team is the primary defense.

So, how do the best managers mitigate this risk?

- Rigorous Due Diligence: They don't just look at credit scores. They analyze cash flow statements, dissect business models, and map out the competitive landscape.

- Protective Covenants: These are financial tripwires built into the loan agreement. If a company's performance begins to falter, these covenants give the lender a seat at the table early on.

- Senior Secured Position: Most loans are structured as "senior secured." In simple terms, this means the fund is at the front of the line to be repaid and has a claim on the company’s assets if things go wrong.

Understanding Illiquidity and Lock-Up Periods

You cannot sell an investment in a direct lending fund with the click of a button. It's illiquid, and that is by design. Your money is typically committed for a "lock-up period" that can last anywhere from seven to ten years.

This long-term commitment gives managers the stability to be patient partners with the companies they back, free from the pressure of daily market fluctuations. For you, the investor, it means you cannot access your cash on a whim.

Before committing capital, you must be absolutely certain you won’t need that money in the near future. This asset class is designed for patient investors who are willing to trade immediate liquidity for the potential of higher, steadier returns over time.

That trade-off is the essence of private credit investing.

The Importance of Manager Selection

In private credit, your fund manager can make or break your returns. Manager risk is significant. You are betting on their skill, their strategy, and their discipline. An inexperienced manager might pursue bad deals, cut corners on due diligence, or structure loans poorly, putting your capital at risk.

You must evaluate their track record, investment philosophy, and the depth of their team. A top-tier manager sources unique deals, performs institutional-grade underwriting, and knows how to work with a company if it encounters trouble. The performance gap between the best and worst managers is vast, so vetting the manager is just as important as the manager vetting their borrowers.

Mitigating Risk Through Diversification

Finally, there’s concentration risk—the age-old problem of putting too many eggs in one basket. If a fund is heavily invested in a single company or a specific industry, a problem in that one area could jeopardize the entire portfolio.

The solution is smart diversification. A well-managed direct lending fund spreads its capital across dozens of loans to companies in different, often non-cyclical, industries. By doing this, the fund ensures that if one borrower defaults, the steady payments from the others will cushion the blow. It’s a foundational strategy for creating the stable, predictable income stream that investors seek.

How Banks and Private Credit Work Together

It’s tempting to picture banks and direct lending funds as rivals competing for the same deals. While they do compete, the real story is more nuanced—and far more collaborative. The modern financial landscape isn't about one replacing the other; it's about adaptation and finding new ways to work together.

Rather than trying to beat private credit at its own game, many banks have smartly shifted their strategy. They've realized it is often more efficient to provide large, stable credit lines to the funds themselves than to originate hundreds of smaller, more complex loans to middle-market companies directly.

This has forged a powerful, almost symbiotic relationship. Banks supply the high-octane fuel (liquidity and leverage) that makes the private credit engine run, while direct lenders handle the specialized, hands-on work of underwriting and managing loans for growing businesses.

The New Role of Banks as Fund Financiers

In this new ecosystem, banks have become indispensable partners to direct lending funds. They do this by offering large, flexible credit facilities, often called subscription lines or NAV (Net Asset Value) loans.

Think of these credit lines as a fund manager’s secret weapon. They allow the manager to act quickly on a deal without having to wait for the slower process of calling capital from all their investors. This speed and efficiency provide a massive operational advantage in a competitive market.

The numbers confirm this trend. Banks have been pouring capital into private credit entities.

As of the fourth quarter of 2024, the largest U.S. banks had extended about $95 billion in credit lines to private credit vehicles. That represents a staggering 145% increase over the last five years, a clear signal of just how intertwined these two sectors have become.

This explosion in bank financing, primarily through revolving credit lines, shows that private credit has evolved from a niche alternative into a major market force, one fully supported by the traditional banking system. For a deeper analysis, the Federal Reserve’s full report explores the financial stability implications of this trend.

A Mutually Beneficial Partnership

This teamwork creates a win-win-win situation that demonstrates the efficiency of modern credit markets.

- For Banks: They can deploy large amounts of capital with a single, sophisticated client—the fund. It's far more efficient and often less risky than managing a sprawling portfolio of smaller, individual business loans.

- For Direct Lending Funds: Access to bank credit gives them incredible flexibility. It helps them move faster, operate more smoothly, and even enhance returns through the strategic use of leverage.

- For Borrowers: Ultimately, this well-oiled machine means more capital flows to the mid-sized companies that are the backbone of the economy, funding their growth, acquisitions, and innovation.

So, the dynamic between banks and private credit is not one of conflict. It’s a story of strategic alignment where banks are now financing the financiers, creating a system where each party plays to its strengths.

Answering Your Questions About Direct Lending

As direct lending moves more into the mainstream, many of the same questions tend to arise. This is a positive sign—it means people are getting serious about understanding how this segment of the market truly works.

Let’s break down some of the most common questions to provide a clearer picture.

How Is Direct Lending Different From Private Equity?

The easiest way to remember the difference is to think debt versus equity. It’s the classic lender vs. owner distinction.

A direct lending fund acts as the bank, providing a loan (debt) to a company. The fund makes its money from the interest and fees that the borrower repays. The goal here is steady, predictable income.

Private equity funds, on the other hand, are buying a piece of the company (equity). They take an ownership stake with the goal of growing the business over several years and selling that stake for a significant profit. Their main objective is capital appreciation, not income.

What Is a Business Development Company?

A Business Development Company, or BDC, is a specific type of company created to provide everyday investors with access to private markets. Think of it as a publicly-traded wrapper for private investments.

Many BDCs are essentially direct lending funds that you can buy and sell on a stock exchange. This structure opened the door for retail investors to participate in private credit without being a large institution. It functions similarly to a Real Estate Investment Trust (REIT) for real estate—you can buy shares and get exposure without having to own the underlying assets directly.

What Is a Typical Minimum Investment?

This is a key question, and the answer depends on who you are and how you’re investing. The entry point can range from the cost of a single share of stock to a seven-figure check.

- Institutional Investors: Pension funds or endowments looking to invest directly are often looking at a minimum commitment of $1 million or more.

- Accredited Individual Investors: High-net-worth individuals can often invest through specialized "feeder funds" that pool capital. Here, minimums might drop to the $100,000 to $250,000 range.

- Retail Investors: Publicly-traded BDCs are by far the most accessible route. You can buy shares through any standard brokerage account, often for less than $100.

How Are Direct Lending Fund Fees Structured?

It is crucial to understand the fees. While the exact structure can vary, many funds have historically used a "2 and 20" model, though the industry is constantly evolving. For a deeper dive, our guide on understanding investment management fees is a great resource.

Most funds charge two main fees: a management fee, which is an annual charge of around 1.5% to 2% of the capital you’ve committed, and a performance fee. The performance fee is a share of the profits the fund earns above a pre-agreed minimum return, often called the "hurdle rate."

The idea is to give the fund manager skin in the game, tying their success directly to the investors' returns.

At Commons Capital, we guide our clients through complex opportunities like direct lending to help them build stronger, more diversified portfolios. If you're curious about how private credit could fit into your financial plan, let's connect.