Navigating a turbulent market isn't about perfectly timing the peaks and valleys—it's about implementing robust asset allocation strategies for a volatile market designed to withstand the swings. The goal is to combine long-term, strategic diversification with intelligent, tactical adjustments. This approach helps you manage risk effectively without sacrificing the potential for future growth. It’s the key difference between making emotional, reactive decisions and confidently staying on course toward your financial objectives.

Why Your Asset Allocation Strategy Matters More in Turbulent Times

In a calm, steadily rising market, almost any asset allocation can look good. It's easy to get complacent. But when volatility spikes, a thoughtfully constructed strategy becomes the firewall between disciplined investors and those who take a serious hit. Market turbulence isn't just a threat; it’s a stress test for your portfolio’s design and your own resolve.

The biggest challenge is fighting the instinct to do something—anything—when things get scary. Knee-jerk reactions, like dumping all your stocks in a panic, are a classic way to lock in losses and miss the inevitable recovery. The market’s best days often come right on the heels of its worst.

History shows us just how costly it is to try and time the market. In years with more than 10 high-volatility days (where the S&P 500 swung +/- 2%), average returns were basically flat. But in calmer years with fewer than 10 of those volatile days, the S&P 500 averaged annual returns closer to 20%.

The Foundation of Volatility Management

Navigating these conditions requires a proactive approach, not a reactive one. A solid plan, built before a crisis hits, is your best defense. This boils down to a few core principles:

- Defining Risk Tolerance: You need to know, honestly, how much of a dip your portfolio can take before you lose sleep and abandon your strategy.

- Setting Clear Goals: Your asset mix isn't arbitrary. It should be a direct reflection of what you're trying to achieve, whether that's preserving wealth, generating income, or pursuing aggressive growth.

- Maintaining Discipline: Sticking to your plan is everything. It’s what prevents you from making emotionally-charged mistakes that can do permanent damage to your capital.

Building an All-Weather Approach

Think of your asset allocation as the architectural blueprint for your financial life. It’s supposed to provide stability when the ground starts shaking.

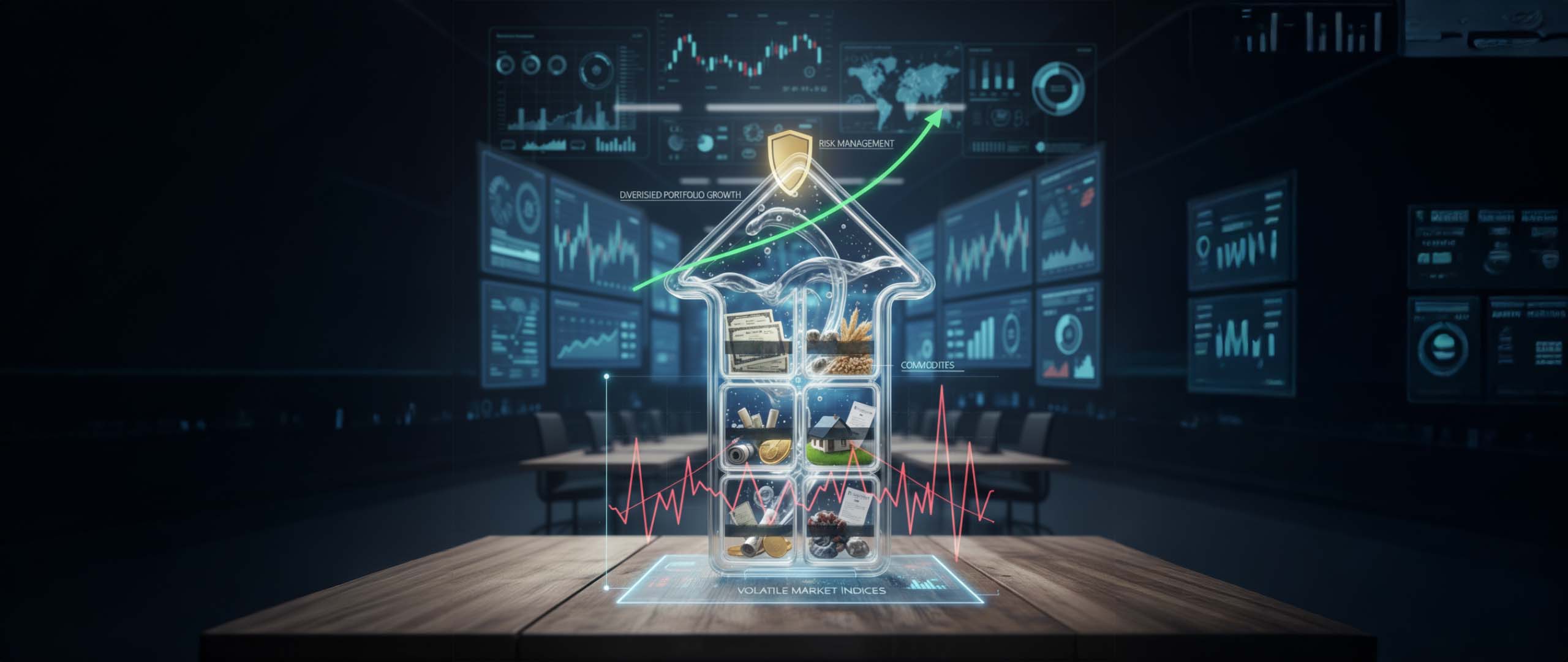

By spreading investments across different asset classes that don’t always move in the same direction—things like stocks, bonds, real estate, and alternatives—you cushion the blow from a downturn in any single area.

This diversification is the bedrock of any successful long-term investment strategy, especially when uncertainty is the new normal. The idea is to build a portfolio that not only survives the storms but is also positioned to find the opportunities they leave behind.

To help put these concepts into a clear framework, here’s a quick overview of the key strategies we’ll be exploring.

Key Strategies for Volatile Markets at a Glance

Each of these plays a unique role in fortifying a portfolio against the unpredictable nature of volatile markets.

Building a Resilient Foundation with Strategic Diversification

Think of your portfolio as a ship designed to navigate any weather the market throws at it. In that picture, strategic diversification is the hull—the core structure that gives your ship stability and integrity. It’s a concept that runs much deeper than the old adage about not putting all your eggs in one basket.

Proper diversification isn't just a suggestion; it's a disciplined science. It's about deliberately combining assets that react differently to the same economic forces. The goal is simple: when one part of your portfolio is down, another should be holding steady or even rising, creating a powerful shock absorber for your wealth.

This is the bedrock of any sound investment plan, especially when markets get choppy. Before you even think about more advanced tactics, getting this foundation right is non-negotiable.

The Power of Non-Correlated Assets

The secret sauce behind diversification is a concept called correlation. In simple terms, it measures how closely the prices of two different assets move together. For decades, stocks and high-quality government bonds have been a classic example of low, or even negative, correlation.

When economic fear sends stocks tumbling, investors typically run to the perceived safety of government bonds, which pushes bond prices up. This see-saw relationship is what helps smooth out returns over the long haul. It's what prevents the kind of gut-wrenching drops that can cause even the most seasoned investors to panic and make poor decisions.

The data backs this up. Portfolios that blend stocks and bonds have shown remarkable strength, handily beating cash during turbulent times. In fact, a classic 60/40 portfolio has outperformed cash holdings over 70% of the time in one-year periods since 1990, delivering an average excess return of 7 percentage points.

Diversification Beyond Stocks and Bonds

The stock-and-bond mix is a great start, but a truly resilient portfolio goes much further. You need to think about spreading investments across multiple dimensions to build several layers of protection.

Here are the key layers to consider:

- Across Asset Classes: This is the most basic layer. It means owning a mix of equities, fixed income, real estate, and alternatives.

- Within Asset Classes: Don't just own "stocks." You should hold a blend of large-cap, small-cap, growth, and value stocks to tap into different market dynamics.

- Geographic Diversification: Spreading your investments globally helps insulate you from a downturn that hits just one country's economy.

- Sector Diversification: Avoid piling into one industry—like tech or financials—by investing across a wide range of economic sectors.

This multi-layered approach is designed to ensure that a crisis in one specific area doesn't torpedo your entire portfolio. To explore this further, you can review these essential investment diversification strategies.

A Practical Example of Diversification in Action

Let’s look at two hypothetical investors, each starting with $1 million at the beginning of a volatile year.

- Investor A is highly concentrated, with 90% of their portfolio in a handful of popular tech stocks.

- Investor B is diversified: 40% in global stocks, 20% in U.S. government bonds, 15% in international bonds, 15% in real estate, and 10% in commodities.

An unexpected economic shock hits, and the tech sector plummets by 30%. Investor A watches their portfolio value drop by hundreds of thousands of dollars, almost overnight. The emotional pressure to sell and stop the bleeding is immense.

Meanwhile, Investor B’s portfolio weathers the storm much better. Their global stocks take a hit, sure, but their government bonds and certain commodities likely rise in value, cushioning the blow. The loss is far smaller, making it much easier to stay calm and stick with their long-term plan.

This scenario gets right to the heart of what diversification is for. It's not about chasing the highest possible returns in a bull market. It’s about preserving capital and keeping your cool when things get rough. To learn more about this foundational approach, read our guide on what is strategic asset allocation, which sets the stage for the more nimble tactics we'll discuss next.

Using Advanced Tactics to Navigate Market Choppiness

Once your portfolio's foundation is set with smart, long-term diversification, it's time to add more responsive tools to your kit. Think of it like this: your strategic allocation is the sturdy hull of your ship, built to withstand any storm. These advanced tactics are the rudder and sails—they let you actively steer through turbulence instead of just riding it out.

This isn't about setting and forgetting. These moves demand active monitoring and a real feel for what's happening in the markets. While your core strategy remains your anchor, these tactics are all about making calculated, nimble adjustments to capitalize on changing conditions.

Mastering Tactical Asset Allocation

Tactical asset allocation (TAA) is the art of making deliberate, short-to-medium-term shifts away from your baseline portfolio mix. The entire goal is to take advantage of what you see as temporary market mispricings or opportunities.

Let's say a specific sector gets hammered by a market overreaction you believe is unwarranted. A tactical tilt would mean temporarily increasing your exposure to that sector, betting on a rebound. This isn't old-school market timing—you're not trying to guess the S&P 500's every move. It’s about making informed shifts based on solid economic data, valuations, and market sentiment.

- Underweighting: You might do this by trimming your position in an asset class that looks overheated or is facing serious headwinds.

- Overweighting: This means beefing up your exposure to an area that seems primed for a near-term run.

The key word here is temporary. Once the opportunity you identified has played out, you bring your portfolio back to its original strategic targets. It's a disciplined way to add a layer of active decision-making without abandoning your core principles.

To help clarify how these sophisticated strategies differ, here’s a quick comparison.

Comparison of Advanced Allocation Tactics

As you can see, each of these tools serves a distinct purpose. They aren't mutually exclusive; in fact, they often work best when used in concert to navigate different types of market weather.

The Role of Dynamic Rebalancing

Most people rebalance their portfolios on a set schedule, like once a year. Dynamic rebalancing, on the other hand, is driven by market movements, not the calendar. You set specific triggers, and when an asset class drifts too far from its target, you act.

For instance, if your target for U.S. stocks is 40% of your portfolio, you might set a rule to rebalance anytime it climbs above 45% or drops below 35%. This forces a disciplined, systematic process of selling what's done well and buying what's cheap—the holy grail of investing.

This approach is incredibly powerful because it prevents your portfolio's risk level from creeping up without you realizing it. To dig deeper into the mechanics, our guide on what is portfolio rebalancing breaks down the core principles of keeping your asset mix on track.

Using Cash as a Strategic Weapon

Too many investors see cash as dead weight—a safe but boring asset that drags down returns. In a choppy market, that view is completely wrong. Cash becomes one of your most powerful strategic tools.

Holding a healthy cash reserve gives you two massive advantages:

- Dry Powder: It provides the liquidity to pounce on incredible opportunities when high-quality assets go on sale during a downturn.

- Emotional Stability: Knowing you have cash on the sidelines can be a powerful antidote to the anxiety of watching your portfolio value swing, helping you avoid the classic mistake of selling at the bottom.

The right amount of cash is personal, but it should never be viewed as a drag. Think of it as an option on future opportunities, one that holds immense value when uncertainty is high.

Why Alternative Investments Matter for Portfolio Stability

For years, the classic stock-and-bond portfolio was the bedrock of sound investing. It worked because when stocks took a hit, high-quality bonds usually went up, acting as a reliable shock absorber. But what happens when that dependable relationship falls apart?

We’ve seen it happen. During recent bouts of high inflation and rising interest rates, both stocks and bonds fell in unison. Suddenly, the old playbook wasn't working. This is precisely why alternative investments have shifted from a "nice-to-have" to a core part of any truly resilient portfolio. They open up a world of opportunities beyond the public markets, giving you a powerful way to build stability when traditional assets just can't.

Exploring Assets Beyond the Public Markets

"Alternatives" isn't one single thing; it's a broad category of different opportunities, each with its own rhythm. The common thread? Their performance is driven by factors far removed from the day-to-day mood swings of the S&P 500. This creates an invaluable buffer when markets get choppy.

Getting a handle on what counts as an alternative is the first step. These aren't assets you can buy and sell with a click of a button. They often require more in-depth due diligence and are less liquid, which is why they’re particularly well-suited for sophisticated investors with longer time horizons.

By venturing beyond conventional stocks and bonds, investors can access return streams that are insulated from the emotional swings of the public markets. This can be crucial for preserving capital during periods of extreme stress.

Let's break down the main types and the specific jobs they can do within a portfolio built for both stability and growth.

Key Types of Alternative Investments

- Private Equity: This is where you invest directly into private companies before they ever hit a stock exchange. The potential for high growth is huge, but it's a long-term game—you’re typically locked in for years.

- Private Credit: Think of this as being the bank. It involves direct lending to companies, and it often provides better yields than you'd find in the public bond market. The real appeal is the steady, contractually obligated cash flow that’s less rattled by interest rate hikes.

- Real Assets (Real Estate & Infrastructure): Putting capital into physical assets like commercial buildings, airports, or toll roads can create incredibly stable, inflation-protected income. Infrastructure, especially, can behave like a utility with predictable demand, making it a fantastic defensive play.

- Commodities: There’s a reason people have turned to gold for centuries. It’s a classic safe haven during economic turmoil. Its value isn't tied to corporate earnings reports, making it a truly effective diversifier when fear is driving the market.

Each of these categories brings something different to the table, from hedging against inflation to unlocking growth that has nothing to do with the stock market. For a deeper dive, you can learn more about what is alternative investment in our comprehensive guide.

The Strategic Value of Low Correlation

The single most important reason to include alternatives in your asset allocation strategies for a volatile market is their low correlation to public stocks. It's a simple but powerful concept.

When a major sell-off hits and stock prices are in a free-fall, the value of an office building or a private business loan doesn't react in real-time. Their worth is tied to fundamentals—like rental income or contractual debt payments—not the panic of the trading floor.

This insulation is what creates genuine portfolio stability. While your public stock holdings might be down, the alternative sleeve of your portfolio can act as a steadying anchor, smoothing out the ride and reducing the depth of any downturns. That's what allows you to stay invested and avoid the panicked decisions that so often derail long-term success.

Putting Your Volatility Strategy into Action

A brilliant strategy on paper is worthless without disciplined execution. This is where the rubber meets the road, where we turn well-crafted ideas about asset allocation into real-world results. It’s less about making brilliant tactical moves and more about mastering the psychological grit to stick with the plan when markets feel chaotic.

Successfully implementing your strategy comes down to the practical details that can make or break your bottom line. We're talking about managing costs, being smart about taxes, and making sure every single action ladders up to your long-term goals.

Maximizing After-Tax Returns with Tax-Loss Harvesting

When markets take a nosedive, one of the most powerful tools in a high-net-worth investor's toolkit is tax-loss harvesting. It sounds complicated, but the concept is straightforward: you sell an investment that has lost value to intentionally "realize" that loss on paper.

You can then use that loss to offset capital gains you’ve cashed in elsewhere in your portfolio, which can meaningfully lower your tax bill. The trick is to immediately reinvest the cash into a similar—but not identical—asset. This keeps you in the market and on-plan while steering clear of the IRS's "wash-sale" rule. Suddenly, a market dip becomes a tax-saving opportunity.

Managing Costs and Maintaining Discipline

Every trade costs money, from brokerage fees to the tiny slice you lose on the bid-ask spread. When you're actively rebalancing, these costs can add up and silently erode your returns. It's just smart practice to be mindful of how often you trade and to do so in the most cost-effective way possible.

But honestly, the biggest "cost" most investors face comes from their own behavior. The psychological pressure during a steep market correction is immense.

The single most critical part of implementation is fighting the emotional urge to tear up your plan and run. A well-built strategy is designed for these moments. Sticking with it is what separates disciplined investors from those who just react to the noise.

Here are the essential guardrails to keep yourself and your strategy on track:

- Automate Your Decisions: Take emotion out of the driver's seat. Set up pre-determined rebalancing triggers—for example, when an asset class drifts 5% away from its target—to force yourself to systematically buy low and sell high.

- Focus on Your Goals: Pull out your long-term financial plan and review it. This simple act reminds you that short-term volatility is just a distraction from what truly matters—funding your retirement, your family's future, or your legacy.

- Avoid Constant Monitoring: Checking your portfolio every day is a recipe for anxiety and bad, reactive decisions. Schedule specific times to review and rebalance, whether that's quarterly or semi-annually, and then leave it alone.

Aligning Strategy with Your Unique Circumstances

Finally, and this is non-negotiable, the way you execute your strategy has to be a perfect fit for your personal financial reality. An asset allocation that works for a tech entrepreneur might be a disaster for a professional athlete with a shorter earning window.

The execution must be tailored to several deeply personal factors:

- Risk Tolerance: Your plan absolutely must let you sleep at night. If market swings are giving you ulcers, the risk level is too high, and you're bound to abandon the strategy at the worst possible moment.

- Time Horizon: An investor on the cusp of retirement will approach implementation very differently than someone in their early 40s. How soon you need the money dictates everything—from how aggressively you rebalance to how much risk you can afford to take.

- Liquidity Needs: Your strategy has to accommodate your real-world cash flow. This ensures you're never forced to sell good assets at a terrible time just to cover an unexpected expense.

By focusing on these practical elements—tax efficiency, cost control, behavioral discipline, and deep personal alignment—you close the gap between having a good plan and actually making it work for you. This is how you build a portfolio that’s truly designed to weather any storm.

Building Your All-Weather Investment Portfolio

When it comes to navigating choppy market waters, there's no magic bullet. The real key is building a robust, all-weather portfolio—one that's deliberately engineered to handle whatever the economy decides to throw your way. Think of it less as a single product and more as a carefully constructed system.

This approach brings together everything we've discussed so far, and it all starts with the non-negotiable foundation: strategic diversification. Spreading your investments across asset classes that don't move in lockstep is still the single most powerful defense against a sudden, sharp downturn. It’s the hull of your financial ship, providing the core stability you need to stay afloat.

From that solid base, you can make intelligent tactical adjustments, which act like the ship's rudder, letting you steer through rough seas. These aren't wild guesses or attempts to time the market; they're calculated, short-term shifts to manage risk or capitalize on clear opportunities that volatility creates. The stabilizing power of alternative investments adds another critical layer, providing return streams often insulated from the panic that can grip public markets.

The infographic below shows how all these pieces fit together into a cohesive plan of action.

As the visual lays out, a winning strategy is built in layers. It requires practical techniques built upon a foundation of behavioral discipline, which in turn guides how you execute your plan.

But here’s the thing—none of this matters without disciplined execution. A brilliant plan is absolutely worthless if you toss it overboard at the first sign of trouble. The psychological strength to stick with your strategy, rebalance when you're supposed to, and even see downturns as opportunities is what truly separates successful investors from the herd.

By mastering these core pillars—diversification, tactical agility, alternative assets, and unwavering discipline—market volatility transforms from something to be feared into a manageable challenge.

Ultimately, the best asset allocation strategies for a volatile market give you the power to protect your capital without giving up on long-term growth. You gain the confidence to stay the course, knowing your portfolio was built not just to survive the storm, but to come out stronger on the other side.

Frequently Asked Questions about Volatile Market Strategies

When markets get choppy, it’s natural for questions to bubble up. Even the most carefully crafted plan can feel uncertain when headlines are screaming. Here are a few of the most common questions we hear from clients, along with some straight-talking answers.

How often should I rebalance my portfolio in a volatile market?

This is the big one. In a turbulent market, the temptation is to either react to every headline or just freeze and do nothing. The right answer isn’t about picking a date on the calendar; it’s about sticking to a pre-agreed discipline.

Forget the rigid quarterly or annual review for a moment. A much smarter way to handle this is with a tolerance-band approach. You simply set a percentage "drift" for each asset class—say, a 5% or 10% band around your target allocation. The only time you rebalance is when a holding strays outside that band.

This method is brilliant in volatile markets for two reasons:

- It stops you from over-trading. You won’t be churning your account and racking up costs based on every little market hiccup.

- It forces you to act decisively. It gives you a clear, unemotional signal to take profits (sell high) or buy into weakness (buy low) when a real, significant move happens.

The key, of course, is to set these bands before the storm hits. That way, logic drives your decisions, not fear.

Should I move everything to cash during a downturn?

The gut reaction to run for the hills and pile into cash during a sell-off is incredibly strong. It's also one of the most damaging mistakes an investor can make. While keeping a strategic cash reserve to pounce on opportunities is smart, dumping your entire portfolio is just market timing in disguise—and that’s a game almost no one wins.

Why is it so bad? Two big reasons:

- You turn paper losses into real ones. Selling after a big drop crystallizes your losses, making them permanent.

- You have to be a genius twice. Getting out is the easy part. The impossibly hard part is knowing exactly when to get back in. History shows the market's best days often happen right after its worst, and missing just a few of those rebound days can cripple your long-term returns.

A better approach? Trust the plan. Your strategic asset allocation was built for moments just like this. The whole point of holding diversified assets like bonds and alternatives is to act as a cushion, giving your growth-oriented investments the time they need to recover.

How do alternative investments fit into a traditional portfolio?

Bringing alternatives into the mix is how you build a truly all-weather portfolio, but it’s a different ballgame than buying stocks and bonds. These assets are generally less liquid and demand a much deeper level of due diligence. That's why they're typically reserved for sophisticated investors with the capital and long-term perspective to match.

The core job of alternatives within your asset allocation strategies for a volatile market is to provide diversification that actually works. Their performance is often tied to fundamentals that have little or nothing to do with day-to-day stock market drama.

- Private Credit can generate steady income from loan payments, almost like a bond but with different risk drivers.

- Infrastructure projects, like toll roads or airports, produce consistent cash flow from essential services people use every day.

- Private Equity opens the door to high-growth companies that you simply can't access on the public markets.

The goal isn't to ditch your traditional holdings but to round them out. When you add a sleeve of assets that don't move in lockstep with your stocks and bonds, you create a portfolio that is structurally stronger and less prone to wild swings. Over the long run, this can make for a much smoother ride.

At Commons Capital, we build sophisticated, customized asset allocation strategies for high-net-worth families, athletes, and entrepreneurs. If you’re ready to build a portfolio that can confidently handle whatever the market throws at it, let's talk. Learn more about our private wealth management services.