Specialized wealth management for professional athletes is essential for turning a few high-earning years into a lifetime of financial security. Unlike a traditional 40-year career, an athlete's peak income window is intensely compressed. This reality demands a unique financial playbook—one focused on aggressive saving, smart risk management, and long-term planning from the moment you sign your first contract. This guide provides a comprehensive answer to the financial questions pro athletes face.

The Unique Financial Playbook Of A Professional Athlete

For most people, a career is a marathon. Income gradually builds over decades, allowing plenty of time to save, invest, and recover from mistakes. For a professional athlete, it’s a flat-out sprint.

This is the fundamental reason why standard financial advice often misses the mark. A dedicated approach to wealth management for professional athletes isn’t just a nice-to-have; it’s a critical part of your long-term survival strategy. The core challenge is simple but massive: managing sudden, immense wealth against a backdrop of career uncertainty. One bad injury, an unexpected trade, or a slump in performance can end it all in an instant. This high-stakes environment means every financial decision carries more weight.

The Pressure Cooker of Sudden Wealth

Going from amateur to a multi-million-dollar contract overnight is a seismic life change. It also brings a unique set of pressures that can evaporate wealth just as quickly as it arrived. Athletes often face intense demands from family and friends, the powerful allure of a lavish lifestyle, and the constant threat of being exploited by bad actors.

Without a solid game plan, it’s frighteningly easy to fall into common traps. These pressures are a key reason why so many athletes face financial distress after their playing days are over. The statistics are jarring: an estimated 75% of NFL players experience financial stress within just two years of retirement, and 60% of NBA players are broke within five years. You can explore more about these financial challenges for professional athletes and see why a proactive strategy is so important.

A Sprint, Not a Marathon

The condensed earning window leaves almost no room for error. A doctor or lawyer might have 40 years to save for a 20-year retirement. An athlete may have less than 10 years to fund a retirement that could easily last for 50 years or more. This requires a complete shift in financial thinking.

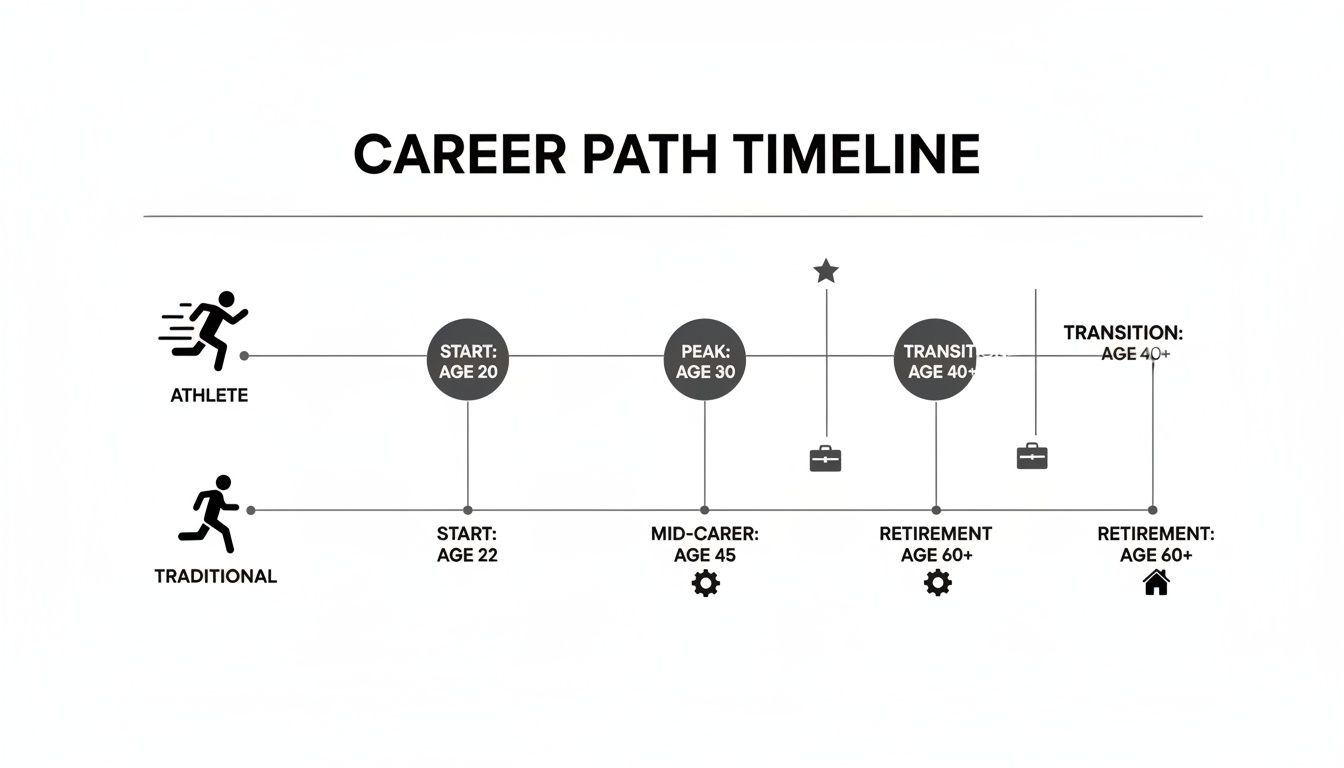

This infographic lays out the stark contrast between an athlete's compressed career timeline and a traditional one.

As you can see, an athlete has to accomplish in a few short years what most people have an entire lifetime to do. This makes early and disciplined wealth management an absolute non-negotiable.

The table below breaks down these timeline differences even further, highlighting just how different the financial journey is.

Athlete Career Vs Traditional Career Financial Timelines

This comparison drives home the point: the financial pressures and timelines are completely different worlds.

The goal is not just to get rich, but to stay rich. This means treating your athletic earnings as the seed capital for the rest of your life, not as a limitless spending account.

Building a financial game plan designed for this unique timeline is the first step toward long-term victory. The following sections will break down the key strategies needed to secure your financial future long after the final whistle blows.

Why a Short Career Demands a Long-Term Financial Strategy

A pro athlete’s career operates on a totally different clock. While most people have about four decades to build their nest egg, an athlete's peak earning window is often just a fraction of that. This reality of front-loaded income—making most of your lifetime wealth in a few intense, high-pressure years—is the single biggest factor that shapes an athlete's financial life.

Think of it like this: your career earnings are a reservoir. A typical professional fills that reservoir slowly and steadily over 40 years. An athlete has to fill it to the brim in maybe a decade, and then make that supply last for the next 50 years or more. That compressed timeframe leaves absolutely no room for error. A single bad injury or a sudden drop in performance can turn the tap off for good, leaving you with a half-full reservoir to get you through a very long retirement.

This dynamic demands a complete mental shift, away from thinking about yearly income and toward aggressive, long-term preservation from day one.

The Math on the Ticking Clock

The average career length in the major leagues tells a pretty stark story. For an NFL player, it's just 3.3 years. In the NBA, it’s a bit longer at around 4.5 years. Even for the stars who beat the odds and play for a decade or more, that peak earning window is still incredibly short. This is why a rock-solid financial plan isn't a luxury; it's a necessity.

Most athletes hang it up before they turn 30. That means their savings have to carry them for another half-century, often while they're figuring out a second career.

The stakes couldn't be higher. With about 17,000 professional athletes in the U.S. relying solely on what they make from their sport, the risk of hitting a wall is immense. The statistics are jarring: studies show 75% of NFL retirees face financial stress in just two years, and a staggering 60% of NBA players are bankrupt within five years of leaving the league. You can read the full research on these challenges to see just how critical early planning is. This isn't just about managing money—it's about building a financial fortress that can stand the test of time.

Your earnings aren’t an annual salary. They're the seed capital for the rest of your life. Every dollar you make during your playing years has to be viewed through the lens of what it needs to do for you decades from now.

Foundational Strategies for Long-Term Security

To win financially, an athlete’s game plan has to be disciplined from the moment that first contract is signed. We're not talking about complicated investments right away. It's all about laying a rock-solid foundation built on timeless, battle-tested principles.

A smart approach from the start rests on three core pillars:

- An Aggressive Savings Rate: A typical professional might save 15% of their income. An athlete needs to be saving 50% or more. This isn't just a suggestion; it's a requirement to fill that financial reservoir quickly and get the power of compounding working for you as early as possible.

- Disciplined Budgeting: Creating—and sticking to—a detailed budget is non-negotiable. It gives you a clear picture of your cash flow, stops lifestyle inflation from eating your future, and makes sure every dollar has a job to do.

- A Detailed Financial Blueprint: A comprehensive financial plan is your roadmap. It needs to lay out your goals, define your risk tolerance, and establish a clear path for investing, tax planning, and estate management right from the beginning.

These foundational strategies aren’t flashy, but they are the most powerful tools an athlete has to make sure a short career can fund a long and prosperous life. Without them, even the biggest contracts can vanish with alarming speed. The goal is simple: make your money work for you long after your playing days are over.

Navigating The Maze of Athlete Income And Taxes

An athlete's income statement looks nothing like a typical paycheck. A huge part of wealth management for professional athletes is simply getting a handle on the fact that money flows in from several different streams, each with its own set of rules and tax headaches. We're not just talking about a salary; it's a tangled web of signing bonuses, performance incentives, endorsement deals, and appearance fees that requires a seriously skilled hand to manage.

The complexity kicks in the second a contract is signed. That big signing bonus? It's often taxed differently than the regular salary that hits your account during the season. Performance bonuses for hitting specific benchmarks add another wrinkle. Then you have endorsement deals, which are basically business income and demand a whole different playbook.

Cracking The Code On The "Jock Tax"

One of the biggest—and most misunderstood—financial hurdles for pro athletes is the infamous "jock tax." It's not some special penalty tax, but the way it's applied to athletes is unique because they're constantly on the road for games, events, and appearances. If you're not planning for it, the jock tax can take a massive bite out of your actual take-home pay.

Here’s a simple way to think about it: imagine a traveling salesman having to pay income tax in every single state where they close a deal. That’s a pro athlete's reality. For every away game in a state with an income tax, a piece of their salary is subject to that state's tax laws. This can easily mean filing tax returns in 10 to 20 different states every single season.

The "jock tax" makes an already complicated financial life even more so. It’s the perfect example of why athletes need a specialized financial team that lives and breathes multi-state tax law to make sure they're not overpaying or, worse, falling out of compliance.

This multi-state tax burden means you have to meticulously track "duty days"—every single day spent practicing, playing, and traveling in each location. For athletes playing on the world stage, it gets even more tangled with foreign tax credits and international treaties thrown into the mix.

Getting Ahead With Proactive Tax Strategy

Just paying taxes as the bills come due is playing defense. Winning the financial game means playing offense. A proactive approach to tax planning can protect a huge chunk of an athlete's hard-earned money by structuring income and investments in the most tax-smart way possible.

Here are a few of the fundamental plays that should be in every athlete's game plan:

- Maxing Out Retirement Accounts: Funneling money into tax-deferred accounts like a 401(k) or a SEP IRA lowers your taxable income today while building your nest egg for tomorrow.

- Smart Deal Structuring: The way a contract or endorsement deal is written can have massive tax consequences. Deferring compensation or spreading payments out over several years can help you avoid getting pushed into a higher tax bracket.

- Residency Planning: Where an athlete officially calls home can make a world of difference. Establishing legal residency in a state with no income tax, like Florida or Texas, can lead to enormous savings.

These are just a handful of the many best tax strategies for high income earners available. The key is to get them in place early and stick with them. And for athletes who are building a real estate portfolio, understanding advanced strategies to minimize real estate capital gains tax is essential for keeping more of the profits from property sales.

A seasoned advisor can help turn these intimidating tax burdens into opportunities, ensuring more of your money stays where it belongs: in your pocket for the long run.

How To Build Your Championship Advisory Team

Just like on the field, winning the financial game requires a team of specialists who are masters of their positions. You'd never see a single coach handle the offense, defense, and special teams all by themselves. The same logic applies to your money—no single advisor should manage every part of your complex financial life.

Building a skilled and trustworthy advisory team is one of the most critical moves an athlete can make. You are the Head Coach of your financial future; it’s your job to go out and recruit the best talent.

Trying to consolidate roles, like letting your agent double as a financial advisor, is a classic mistake. It almost always creates conflicts of interest and leaves you vulnerable. Each pro brings a unique skill set to the table, and keeping their roles distinct ensures a system of checks and balances that protects your wealth. This separation of duties is non-negotiable.

Assembling Your Core Four

Your advisory team should have four key players, each a specialist in their field. They need to collaborate, of course, but their independence is what gives you unbiased guidance that always puts your best interests first. Think of them as your coordinators, each managing a critical part of the game plan you've set.

Here are the essential roles you need to fill:

- Financial Advisor (Offensive Coordinator): This is the pro who helps you design the overall financial game plan. They’re focused on investment strategy, retirement planning, budgeting, and making sure your money is working for you over the long haul. Their entire job is to turn your career earnings into lasting wealth.

- Certified Public Accountant (CPA) (Defensive Coordinator): The CPA is your tax strategist. Their role is to defend your wealth against unnecessary tax hits, manage the nightmare of multi-state filings like the "jock tax," and find every legal deduction and credit available to you.

- Attorney (Rules Official): An attorney is absolutely essential for contract reviews, setting up your estate plan (wills and trusts), and asset protection. They make sure all your legal documents are solid, protecting you from liability and ensuring your wealth is passed on exactly how you want.

- Agent (Scout & Negotiator): The agent’s primary job is to maximize your earning potential by negotiating contracts and locking down endorsement deals. They are experts in the sports marketplace, not in long-term financial planning or tax law.

This structure creates natural accountability. Your CPA reviews the tax implications of investments your advisor suggests. Your attorney reviews the legal structure of deals your agent negotiates. Everyone stays in their lane, focused on what they do best.

Before we move on, let's break down these roles and why they are so vital. It's crucial to understand who does what on your team.

Key Roles In A Professional Athlete's Financial Team

Having these distinct roles filled by independent experts creates a powerful system of checks and balances, safeguarding your financial well-being from all angles.

Vetting Your Advisors Like a Pro

Recruiting your team requires serious due diligence. The wrong advisor can be more damaging than a season-ending injury. You have to ask the tough questions and demand transparency before letting anyone near your money.

A critical first step is to confirm any financial advisor you consider is a fiduciary. This isn't just a buzzword; it's a legal standard that obligates them to act in your best interest at all times. This is a non-negotiable requirement. You can get a deeper dive into what to look for in our guide on selecting a financial advisor for athletes.

Building a team isn’t about finding friends; it’s about hiring credentialed experts. Your financial security depends on their competence, integrity, and specialized knowledge of the unique challenges professional athletes face.

When you're interviewing potential team members, use this checklist to guide the conversation:

- Experience: How many professional athletes have you worked with? What specific challenges have you helped them navigate?

- Credentials: What are your professional certifications (e.g., CFP®, CPA, CFA)?

- Compensation: How are you paid? Are you fee-only, fee-based, or commission-based? (Fee-only is usually the cleanest structure to minimize conflicts of interest).

- Fiduciary Duty: Will you sign a statement confirming you will act as my fiduciary?

- Communication: How often will we meet? What does your reporting look like?

By carefully selecting an independent team of specialists, you build a financial fortress around your wealth, making sure it’s protected and managed for a lifetime of security.

Essential Investment Strategies For Every Career Stage

A smart financial game plan for a professional athlete has to be dynamic, shifting and evolving right alongside their career. What works for a rookie fresh off their first contract just won't cut it for a 10-year veteran eyeing retirement. I find it helps to think of an athletic career like a full season—from training camp to the championship—to understand how your investment priorities need to change over time.

Your strategy has to adapt as your world changes. The whole point is to build a portfolio that works hard for you during your peak earning years and keeps supporting you long after you've hung up your cleats.

Early Career: Training Camp

Those first few years, from signing day through your first couple of seasons, are your financial training camp. The mission here isn't to hit home runs with risky investments. It's all about building a rock-solid foundation. Think capital preservation and disciplined saving.

At this stage, your approach to risk should be cautious. Yes, you have a long time horizon, but the immediate goals are simple: build up a serious emergency fund, knock out any high-interest debt, and start stacking capital without throwing it into the deep end of market volatility.

- Build a Deep Bench: Your emergency fund needs to be robust. I'm talking 12-24 months of living expenses. This liquidity is non-negotiable for weathering an unexpected injury or a shorter-than-expected contract.

- Conservative Plays: Stick to low-risk investments. High-yield savings accounts, money market funds, and short-term bonds are your best friends here.

- Establish Good Habits: This is the moment to lock in an aggressive savings rate—aim for 50% or more of your take-home pay.

This defensive playbook ensures that a sudden market downturn or a career hiccup doesn't take you out of the game before you've even really started.

Peak Earnings: The Regular Season

Once your financial footing is secure and you're entering your prime earning years, the strategy shifts gears. Welcome to the regular season. Now, the goal is aggressive but intelligent growth. With a solid capital base to stand on, you can afford to take more calculated risks to really expand your net worth.

Your asset allocation will naturally get more aggressive, with a greater emphasis on equities and even alternative investments. Diversification is the key play here. You want to spread your investments across different asset classes to blunt risk while still capturing growth opportunities.

This is also when things get more complex. For athletes with international ties or those looking for serious asset protection, learning how to open an offshore company and bank account in the UAE can provide some advanced strategic tools for managing global wealth.

Your peak earnings are the fuel for a lifetime of financial independence. The investment decisions you make during this period will have the most significant impact on your long-term wealth.

Transition And Retirement: The Championship Celebration

As you get closer to the end of your playing career, your investment strategy enters its final chapter: the championship celebration. The focus makes a hard pivot from wealth accumulation to wealth preservation and income generation. The mission now is to protect the capital you've worked so hard to build and turn it into reliable income streams that will fund the rest of your life.

Your portfolio's risk profile should dial way back, moving out of high-growth stocks and into assets that produce income. This transition is crucial for making sure your nest egg isn't vulnerable to big market swings right when you need it the most.

- Shift to Defense: Reallocate your portfolio toward fixed-income investments like municipal and corporate bonds.

- Generate Passive Income: Prioritize assets that provide a steady cash flow, like dividend-paying stocks, real estate investment trusts (REITs), and rental properties.

- Secure Your Legacy: This is the time to work closely with your advisory team to put the finishing touches on your estate plan, ensuring your wealth is protected for generations to come.

This final shift protects what you've earned, setting you up for a secure and prosperous retirement. And this kind of financial education is more critical than ever. With emerging trends like NIL deals, college athletes are suddenly handling huge sums of money. College football players earned an estimated $1 billion from NIL payments, and that number is only going up.

This influx of cash puts young athletes in a situation much like the pros, where they have to learn to manage big numbers fast. That's especially true when you consider that a shocking 60% of NBA players go broke within five years of retirement. As I always tell clients, if you can't manage $1,000, you have no business trying to manage $1 million.

Questions We Hear All The Time

Stepping into the financial big leagues brings up a lot of questions. From the moment you sign that first contract, you're not just an athlete; you're the CEO of your own enterprise. Getting straight answers is the first step toward making sure that enterprise is built to last. Here are some of the most common questions we get from professional athletes.

So, When Do I Actually Need a Financial Advisor?

Immediately. The second you sign your first pro contract or a major NIL deal, the clock starts ticking.

The goal isn't to wait until you've piled up some cash before getting advice; it's to have a game plan in place from day one. This is how you master the "sudden wealth" moment instead of letting it master you. Starting early lets you build smart habits, create a real budget, and harness the power of compound growth when you have the most time on your side. Waiting until you're at your peak earning potential is like waiting until halftime to come up with a game plan—you've already missed a massive opportunity.

What's The Single Biggest Mistake Athletes Make With Money?

Hands down, it's overspending based on today's income without a rock-solid plan for tomorrow. It’s a classic trap. The money feels like it will never stop rolling in, so the lifestyle expands to match—luxury cars, big houses, and financially supporting a huge entourage. This is fueled by the illusion that the high-earning years will last forever.

The most powerful defense against this is surprisingly simple: a disciplined budget, built with a wealth manager who gets it. This is the tool that ensures a big chunk of your income is automatically saved and invested for a future that will last a lot longer than your playing career.

This one habit—living on a plan, not just on your paycheck—is what separates athletes who build generational wealth from those who face financial trouble after the cheering stops.

How Do I Protect My Wealth From Scams and Bad Deals?

Because of your public profile and high earnings, you're a magnet for bad ideas and outright scams. Protecting your capital comes down to three things: serious due diligence, a healthy dose of skepticism, and a trusted team watching your back. Be extremely wary of any "can't-miss" investment promising crazy high returns, especially if it comes from someone without verified credentials.

Your financial advisor's job is to vet every single opportunity before you even consider it. The golden rule here is simple: never invest a dollar in something you don't completely understand.

A few non-negotiables for your defense:

- Work with a Fiduciary: This is critical. A fiduciary advisor is legally required to act in your best interest. No exceptions.

- Keep Your Team Separate: Your agent, financial advisor, and CPA should all be independent of one another. This creates a natural system of checks and balances that protects you.

- Question Everything: If an investment pitch sounds too good to be true, it is. Real wealth is built through a steady, disciplined process, not a moonshot.

Think of your advisory team as a firewall, filtering out the noise and the nonsense to protect what you’ve worked so hard to earn.

I'm in My 20s. Why Bother With "Legacy Planning"?

Legacy planning is really about deciding what you want your wealth to accomplish long-term, beyond just your own life. It covers everything from wills and trusts to charitable giving and setting up the next generation for success. It might feel a little strange to think about this in your 20s, but when you're dealing with sudden wealth, it's a day-one priority.

Putting a solid plan in place protects your assets and makes sure they're handled according to your wishes, not left up to a court to decide. Things like trusts can shield your wealth from potential creditors and ensure your family is taken care of in a structured, responsible way.

Thinking about your legacy early also changes your mindset. It shifts the focus from just earning and spending to building something meaningful that will last. This long-term vision is a cornerstone of successful wealth management for professional athletes.

Building a secure financial future requires a specialized game plan and a team that truly understands the pressures and opportunities of a pro career. At Commons Capital, we have the expertise to help you navigate this world, turning your success on the field into a lifetime of financial security. Learn more about how we can build your winning financial strategy.