Yes, you can absolutely hold physical real estate in your IRA, but you can't use the standard account from your typical brokerage. This powerful strategy requires a special account called a Self-Directed IRA (SDIRA), which allows sophisticated investors to move beyond stocks and bonds into alternative assets like property. When done right, this approach unlocks the potential for tax-deferred or even tax-free growth on rental income and appreciation, making it a cornerstone of modern retirement planning.

Unlocking Property Wealth Inside Your Retirement Account

For many high-net-worth individuals, the idea of diversifying a retirement portfolio can feel disappointingly limited by what’s available in the public markets.

The good news is, the rules governing retirement accounts are more flexible than most people realize. They open the door to tangible assets that can generate consistent cash flow and build real, long-term wealth. Investing in real estate in your IRA is a calculated move to hedge against stock market volatility and capture growth in a completely different sector.

This isn't just some niche tactic; it's part of a broader trend of investors seeking greater control over their financial futures. The explosive growth of IRAs as a whole highlights this shift. In the first quarter of 2025, Individual Retirement Accounts held an astonishing $16.8 trillion in assets.

That figure shows IRAs are growing faster than defined contribution plans like 401(k)s. In fact, a March 2024 study revealed that 44% of U.S. households now own an IRA. You can dig into more of these retirement asset trends from the folks at 401k Specialist.

Why Consider Real Estate For Your IRA

The primary motivation here is the unique tax advantage. Just imagine collecting rental income year after year without getting hit with an annual tax bill on it.

Every dollar earned—from rent checks to the final profit on a sale—remains sheltered within the IRA. That protection from taxes allows your investment to compound much more rapidly than it could otherwise.

Let’s take a look at the key components in a quick reference table.

Real Estate in Your IRA At a Glance

This strategy offers several distinct benefits that are hard to replicate with traditional investments:

- Tax-Advantaged Growth: All rental income and property appreciation grow either tax-deferred (in a Traditional IRA) or completely tax-free (in a Roth IRA), maximizing your long-term returns.

- Portfolio Diversification: Real estate often has a low correlation to the stock market, which can be a lifeline for your portfolio during economic downturns.

- Passive Income Stream: A well-chosen rental property can provide a steady stream of income directly into your retirement account, funding future investments without new contributions.

- Inflation Hedge: As a hard asset, real estate values and rental rates tend to rise with inflation, helping to protect the purchasing power of your retirement savings.

By placing real estate within a tax-advantaged structure like an SDIRA, you are essentially creating a powerful engine for wealth accumulation, shielded from the annual tax drag that affects traditional property investments.

This guide is designed for serious investors ready to explore exactly how to structure these investments, navigate the tricky IRS rules, and build substantial, tangible wealth for retirement.

How a Self-Directed IRA for Real Estate Works

If you want to hold property in a retirement account, you can't just call up your standard brokerage firm. Those IRAs are built for the usual suspects: stocks, bonds, and mutual funds. To invest in real estate in your IRA, you need a completely different tool—a specialized account known as a Self-Directed IRA (SDIRA).

This isn't your average retirement account. An SDIRA puts you squarely in the driver's seat, opening up a world of alternative assets that Wall Street doesn't touch. But with that control comes a heavy dose of responsibility. You have to play by a strict set of IRS rules, which is why a specialized custodian is absolutely essential.

The Role of the SDIRA Custodian

Think of your SDIRA custodian as the official treasurer for your IRA's real estate ventures. They are an IRS-approved financial institution, but they don't act like a traditional broker who might offer you investment advice.

Their job is purely administrative and compliance-focused. They won't help you find a deal or tell you if a property is a good buy. Their mission is to make sure every dollar that moves in or out of your account follows IRS regulations, keeping your IRA's tax-advantaged status safe and sound.

A good custodian handles several crucial tasks:

- Holds the Title: When your SDIRA buys a property, your name won't be on the deed. The title is held in the custodian's name for the benefit of your IRA. It will look something like this: "ABC Custodian FBO [Your Name] IRA."

- Manages Funds: Every financial transaction—from the initial purchase price to collecting rent checks and paying the plumber—must flow through the SDIRA. The custodian is the one who cuts the checks and deposits the income on your behalf.

- Ensures IRS Compliance: They handle the critical record-keeping and reporting required by the IRS. This helps you steer clear of "prohibited transactions" that could blow up your account.

In essence, the custodian is the gatekeeper. They execute your investment decisions while ensuring every move aligns with federal law. This creates the necessary arm's-length distance between you and your retirement funds.

Funding Your Real Estate IRA

So, you've picked a custodian and opened your SDIRA. Now you need to get money into it. You can't just write a personal check to buy that duplex. The capital has to come from existing, qualified retirement funds.

Fortunately, moving the money is pretty straightforward. As you map out your plan, remember that financing investment property within an IRA has its own unique rules, often requiring special non-recourse loans that protect your personal assets.

Here are the three main ways to fund your SDIRA:

- Annual Contributions: Just like any other IRA, you can contribute up to the annual limit. For 2025, that's $7,000 if you're under 50, and $8,000 if you're 50 or older.

- Direct Transfers (Trustee-to-Trustee): This is the cleanest and most common method. You simply instruct the custodian of your current IRA to wire the funds directly to your new SDIRA custodian. It's not a taxable event, and you can transfer as much as you want.

- Rollovers: You can also move money from a former employer's plan, like a 401(k) or 403(b). In a rollover, the check is sent to you, giving you 60 days to deposit it into your SDIRA. Miss that deadline, and you'll face taxes and penalties.

Using these methods, you can consolidate your retirement savings into a powerful account ready to deploy into real estate, making the path to owning property within your IRA clear and achievable.

Alright, you've got the mechanics of setting up and funding an SDIRA down. Now for the exciting part: what can you actually buy with it?

When people hear real estate in your IRA, they often picture a single-family rental. But the reality is so much bigger. You have a whole spectrum of options, from hands-on property ownership to completely passive, institutional-grade deals. The key, no matter what you choose, is that your IRA—not you personally—is the one making the investment.

Direct Property Ownership

This is the most straightforward route. Your SDIRA buys a physical property, and the title is held in the name of your IRA custodian. It gives you a ton of control over a single, tangible asset.

You’ve got a few common choices here:

- Residential Properties: Think single-family homes, duplexes, or small apartment buildings you intend to rent out long-term.

- Commercial Properties: Your IRA can own anything from an office building or retail strip to an industrial warehouse.

- Raw Land: This is a pure appreciation play. You buy undeveloped land hoping it will be worth more down the road, but don't expect any rental income along the way.

Going direct gives you control, but it also puts management and due diligence squarely on your shoulders. If you’re considering this path, you absolutely need to know how to properly assess a property.

Indirect and Passive Investing Options

Maybe you love the idea of real estate returns but shudder at the thought of late-night calls about a broken water heater. If that's you, indirect investing is a game-changer. These structures let you pool your IRA funds with other investors to get into larger, professionally managed deals that would otherwise be out of reach.

Real estate syndications and funds offer a compelling path to diversification and passive income. It’s a way to get all the benefits of property ownership without the day-to-day operational headaches—perfect for busy professionals.

These are designed to be completely hands-off for you, the investor.

- Real Estate Syndications: Here, you and other investors fund a specific project, like buying a large apartment complex or developing a new shopping center. A professional sponsor handles everything from start to finish.

- Private Placements and Funds: These work like syndications, but instead of backing a single asset, you’re investing in a whole portfolio of properties. A fund might own dozens of assets across different cities and property types, giving you instant diversification.

Understanding Potential Returns

Let's talk numbers. When you're investing in real estate in your IRA, it’s critical to set realistic financial expectations. The returns can swing pretty wildly depending on the deal—from a stable, income-producing property to a more aggressive ground-up development.

The potential for strong, tax-advantaged returns is exactly what draws high-net-worth investors to this strategy. Industry analysis shows that for low-risk "core" assets—like a fully-leased apartment building in a major city—targeted internal rates of return (IRR) can be a steady 6% to 9%. For more opportunistic development projects, those targeted returns can jump to 18%-25%.

Looking ahead to 2025, the projections for institutional-grade, cash-flowing properties are an annual average return of 6%-8%. That breaks down into cash-on-cash yields of 4%-6% and equity multiples of 1.5x-1.7x over a typical 5-7 year hold period. It’s a compelling picture.

This range of returns gives you the flexibility to build a portfolio inside your IRA that matches your personal risk tolerance and retirement timeline, whether you’re after stable cash flow or more explosive growth.

Navigating Critical IRS Rules and Prohibited Transactions

Tapping into your IRA for real estate deals unlocks some incredible tax advantages, but that power comes with a heavy dose of responsibility. You have to follow the IRS rules to the letter.

Think of your IRA as a protected financial bubble. The IRS is adamant that this bubble remains completely separate from you, your family, and your personal finances. If you blur those lines, the consequences are severe—you could even get your entire IRA disqualified, triggering a massive tax bill and penalties.

Compliance isn't optional; it's the bedrock of this entire strategy. The single most important principle to grasp is the prohibition against self-dealing. In plain English, this means your IRA's assets must work exclusively for the benefit of the retirement account itself. They can't be used to directly or indirectly benefit you or certain family members.

Understanding Disqualified Persons

So, who can't you do business with? The IRS has a specific list of "disqualified persons" who are strictly forbidden from transacting with your IRA. This list is probably broader than you think, and it's essential to know it cold.

These individuals and entities include:

- You and your spouse. This one’s the most obvious.

- Your lineal descendants. That means your children, grandchildren, and their spouses.

- Your lineal ascendants. This covers your parents and grandparents.

- Fiduciaries to the IRA. This could be your financial advisor or anyone else providing investment advice for the account.

- Entities controlled by disqualified persons. If you own 50% or more of a business, that company is also considered a disqualified person.

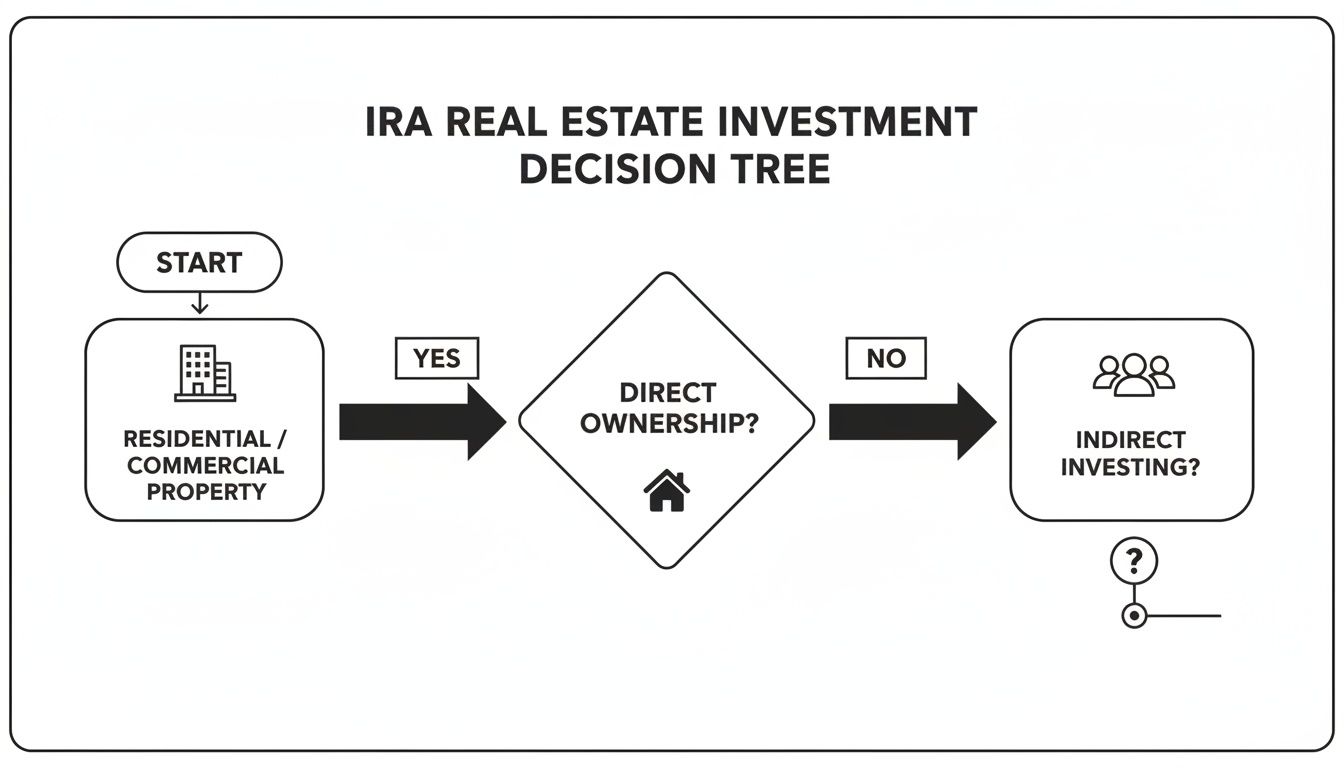

This flowchart can help you visualize the first big decisions you'll face, which immediately set you on a path where these rules come into play.

As you can see, the path splits early between owning a property directly versus investing indirectly, and each route has its own compliance hurdles to clear.

Common Prohibited Transaction Scenarios

Let's make this real. Here are a couple of common, seemingly innocent mistakes that can blow up an investor's strategy.

The Vacation Home Mistake

Imagine your IRA owns a beautiful beach house. You think, "What's the harm in letting my daughter and her family use it for a week as a birthday gift?" That's a classic prohibited transaction. A disqualified person (your daughter) just received a personal benefit from an IRA asset. The IRS sees that as a major violation.

The Sweat Equity Trap

Let's say the rental property your IRA owns needs a new deck. You're pretty handy, so you figure you'll save the IRA some cash by spending a weekend building it yourself. Big mistake. This contribution of personal labor, or "sweat equity," is strictly forbidden. The IRA has to pay a third-party, non-disqualified contractor for all work.

The core test is simple: Does the transaction provide a current, personal benefit to a disqualified person? If the answer is yes, it's almost certainly prohibited. The only beneficiary of the IRA's assets can be the IRA itself.

The Challenge of UBTI and UDFI

Beyond self-dealing, two other tricky tax concepts can catch investors by surprise: Unrelated Business Taxable Income (UBTI) and Unrelated Debt-Financed Income (UDFI). These can actually trigger taxes inside your tax-sheltered IRA.

UBTI usually only applies if your IRA is running an active business (like a hotel), which is pretty rare for most real estate investors. UDFI, however, is far more common.

UDFI Explained with an Analogy

Think of it this way: The IRS gives you tax breaks on your retirement money. But if you use a loan to buy a property, a portion of that asset is technically being paid for with the bank's money, not yours. The IRS wants its cut from the income generated by the bank's money.

Let's say your IRA buys a $500,000 property. You put down $200,000 in cash from the IRA and get a $300,000 non-recourse loan. In this case, 60% of the property is debt-financed. That means 60% of the net rental income would be subject to UDFI tax. This calculation is critical, as it directly impacts your net returns and how you plan for distributions down the road.

Getting these rules right is non-negotiable. One small misstep can undo years of smart planning. Mastering the concepts of disqualified persons, self-dealing, and UDFI is the only way to keep your real estate IRA strategy both compliant and successful.

Strategic Financial Considerations for Investors

Once you've wrapped your head around the basic rules, it's time to dig into the strategic financial planning that separates a good real estate IRA investment from a truly great one. This is where sophisticated investors shine, carefully managing financing, valuation, and long-term liquidity to squeeze every drop of value from their tax-advantaged accounts.

Getting these advanced concepts right is what truly maximizes growth and helps build a durable legacy.

One of the most powerful tools in real estate is leverage, but using it inside an IRA is a whole different ballgame. You can't just walk into your local bank for a conventional mortgage. Why? Because that would require a personal guarantee, which is a textbook prohibited transaction.

The only way to finance property inside your IRA is with a non-recourse loan. This is a special kind of loan secured only by the property itself. If the loan goes south, the lender can take the property, but they have no recourse—no claim—on your other IRA assets or your personal finances. This keeps that strict wall between you and your IRA that the IRS insists on.

Mastering Leverage with Non-Recourse Loans

A non-recourse loan lets your IRA punch above its weight, acquiring a much more valuable asset than it could with cash alone. This can seriously amplify your returns.

Imagine instead of buying a $200,000 property outright, your IRA uses that same $200,000 as a down payment on a $600,000 property. Suddenly, you're controlling a much larger, more valuable asset.

But this kind of leverage comes with a critical tax string attached: Unrelated Debt-Financed Income (UDFI).

While your IRA is a tax-sheltered vehicle, the IRS looks at income generated from borrowed money—the "debt-financed" part—a little differently. A portion of your net income and capital gains that can be traced back to the loan will be subject to Unrelated Business Income Tax (UBIT).

Let’s go back to that $600,000 property financed with a $400,000 non-recourse loan. In that scenario, roughly two-thirds of the net rental income would be taxable. This doesn’t kill the deal, but it means you have to run the numbers carefully. You need to be sure the after-tax returns still hit your investment targets.

Annual Valuation and Long-Term Planning

Unlike stocks, your rental property's value isn't flashing on a screen every second. But the IRS still requires you to determine its Fair Market Value (FMV) at least once a year. This isn't just busywork; it's essential for accurate reporting and becomes critical as you near retirement age.

- Accurate Reporting: Your SDIRA custodian relies on an updated FMV to report your account's total value to the IRS each year on Form 5498.

- RMD Calculations: When you have to start taking Required Minimum Distributions (RMDs), the amount is based on your IRA's total value. A bad valuation could mean you take out too little (and face penalties) or too much.

- Strategic Conversions: If you're thinking about a Roth conversion, a precise valuation is non-negotiable for figuring out the correct income tax you'll owe.

This yearly requirement makes working with qualified appraisers and keeping meticulous records a must. It also ties into understanding the various property investment tax benefits, which can be supercharged inside an IRA with the right plan.

Liquidity and Distribution Strategies

Finally, you have to plan for liquidity—or the lack thereof. Real estate is famously illiquid. You can't just sell a few bricks from an apartment building to meet your RMD. This means you need to think ahead.

Will you sell the property inside the IRA before RMDs start, turning the asset into cash? Or will you do an "in-kind" distribution, transferring a percentage of the property's title into your personal name? Each choice has very different tax consequences. This foresight also connects to broader wealth management, which is why it's smart to consider how your IRA assets are protected from creditors as part of your overall plan.

Carefully navigating these financial details—from the loan you choose to how you'll eventually take distributions—is what elevates holding real estate in your IRA from a clever idea into a cornerstone of multi-generational wealth.

Let's get practical and walk through what this looks like for a real investor.

A High-Net-Worth Investor's Playbook

To see how investing in real estate through an IRA works in the real world, let's follow a hypothetical, but very typical, client journey.

Meet Dr. Evelyn Reed. She's a 55-year-old surgeon with a sizable 401(k) from a previous job just sitting there, not really doing much for her. Like many of our clients, she's tired of being completely exposed to the whims of the stock market and wants to put her money to work generating passive income in a tax-sheltered way.

After a deep dive with her advisor at Commons Capital, they land on a private real estate syndication. It’s the perfect fit. She gets access to a professionally managed, institutional-grade property without any of the headaches of being a landlord.

Step 1: Funding the Self-Directed IRA

First things first, Evelyn can't use her old 401(k) directly. Her advisor helps her open a new Self-Directed IRA (SDIRA) with a custodian that knows the ins and outs of alternative assets.

She then greenlights a direct rollover of $300,000 from the old 401(k) into her new SDIRA. This is a crucial step: because the money moves straight from one retirement account to another, it's a completely tax-free event. Just like that, her SDIRA is funded and ready to deploy.

Step 2: Finding and Vetting the Deal

Her advisor brings a compelling private placement to her attention—a syndicate raising money to buy a top-tier, Class A apartment complex in a booming Sun Belt market. The deal is structured to provide an 8% preferred return (a first-priority payout to investors) and is targeting a total internal rate of return (IRR) of 14-16% over five years.

This isn't a blind leap of faith. Evelyn and her advisor roll up their sleeves and do their homework:

- Sponsor's Track Record: Who's running the show? They dig into the sponsoring firm's history, looking at how their past deals performed, what returns they delivered to investors, and—importantly—how they handled market downturns.

- The Investment Memo: They tear apart the deal's financial projections. Are the underwriting assumptions realistic? How do the rents compare to similar properties? Is the budget for capital improvements adequate?

- The Fine Print: They meticulously review the legal documents, like the Private Placement Memorandum (PPM), to fully grasp the investment structure, fee schedule, and all potential risks.

Step 3: Pulling the Trigger

After a thorough review, Evelyn feels confident and decides to invest $150,000. She can't just write a personal check, though. Remember, the IRA is the investor.

She formally instructs her SDIRA custodian by filling out a "direction of investment" form and providing the signed subscription agreement from the syndicate.

The custodian isn't an advisor; they're an administrator. They check the paperwork to make sure it's all in order and then wire the $150,000 directly from Evelyn's SDIRA to the syndication's bank account. The investment is now officially held in the name of "ABC Custodian FBO Dr. Evelyn Reed IRA."

It doesn't take long for the investment to start paying off. Within a few months, the property is throwing off cash, and the first quarterly distribution of 2% ($3,000) is wired directly back into her SDIRA.

This income is completely tax-deferred. It lands in her account, ready to be compounded and reinvested into the next deal, all shielded from the taxman inside her IRA. This is how real wealth is built.

Your Questions Answered: A Real Estate IRA FAQ

The idea of putting a rental property into your retirement account is powerful, but let's be honest—it also brings up a lot of questions. This is where the rubber meets the road. We'll tackle some of the most common things investors ask to make sure you're moving forward with your eyes wide open.

Can I Just Use My Current IRA to Buy a House?

Not a chance. Your standard IRA from a big-name brokerage is built for stocks and bonds, not for holding the title to a duplex. To do this, you absolutely must open a Self-Directed IRA (SDIRA).

Think of it this way: a normal IRA is like a sedan—great for the highway, but you wouldn't take it off-roading. An SDIRA is the 4x4 of retirement accounts, specifically designed for "alternative" terrain like real estate. You'll need to work with a specialized custodian who knows how to handle these assets. Once that account is open, you can move money into it through a direct transfer from another IRA or by rolling over an old 401(k).

What Happens to the Rent Checks?

This is critical: every single dollar of rental income must go directly back into your SDIRA. Not your personal checking account. Not even for a day.

That rental income is then sheltered inside the IRA, where it can grow tax-deferred (in a Traditional SDIRA) or completely tax-free (in a Roth SDIRA). The reverse is also true. Any expense—from property taxes and insurance to a new water heater—has to be paid straight from the SDIRA's funds.

The golden rule here is that the IRA is the owner. It collects all the money and pays all the bills. The IRS demands a strict wall between your personal finances and your retirement account, and this is how you maintain it.

What's the Easiest Way to Mess This Up?

The absolute biggest landmine is something called a "prohibited transaction." It’s a fancy term for any kind of self-dealing where you or a "disqualified person" (think immediate family) gets a personal benefit from the property your IRA owns.

It’s surprisingly easy to trip over these rules. Some classic mistakes include:

- Personal Use: You can't stay at the property. Not for a vacation, not for a weekend, not even for one night to fix a leaky faucet.

- Renting to Family: Your kids can't be your tenants. Neither can your parents, spouse, or grandkids.

- Sweat Equity: You're a great handyman? Too bad. The IRS forbids you from doing your own repairs or renovations on the property. You have to hire a third party.

Break these rules, and the consequences are brutal. Your entire IRA could be disqualified, forcing an immediate distribution and hitting you with a massive tax bill and penalties.

How Do I Actually Get Money Out of a Real Estate IRA?

When it comes time to take distributions, especially once you hit the age for Required Minimum Distributions (RMDs), you can't just withdraw a few thousand dollars like you would from a stock portfolio. Real estate is illiquid, so you have two main paths.

The first is an "in-kind" distribution. This involves legally transferring a percentage of the property's ownership from the IRA's name to your name. If you transfer 10% of the title to yourself, you'll owe income tax on 10% of the property's current fair market value.

The simpler route? Have the IRA sell the property. The cash from the sale lands back in your SDIRA, and from there, you can take normal cash distributions just like you would from any other IRA.

Navigating the world of real estate IRAs isn't something you want to do alone. It demands careful planning and a team that’s been down this road before. At Commons Capital, we specialize in helping high-net-worth individuals weave sophisticated strategies like this into their complete financial picture. If you're ready to see how alternative assets could strengthen your retirement plan, let's connect and start the conversation.