One Big Beautiful Bill: What It Means for You

On July 4, 2025, the One Big Beautiful Bill (OBBB) was signed into law, ushering in sweeping tax changes that affect households, business owners, and retirees across the country. This new legislation makes permanent some of the most significant provisions from the 2017 Tax Cuts and Jobs Act, while also introducing new tax breaks for workers, families, and donors. However, not all changes benefit every group equally, and it’s important to understand how these provisions may impact your financial plan.

Key Tax Reforms and What They Mean for You

One of the most headline-grabbing components of OBBB is the formal extension of the 2017 tax bracket changes. Tax rates ranging from 10% to 37% are now locked in for the long haul, providing stability for many earners. The standard deduction has also been increased to $15,750 for single filers and $31,500 for joint filers, starting in 2025 and indexed for inflation. This benefits many middle-income families who opt not to itemize deductions.

Another major change is the introduction of new, targeted deductions for workers and seniors. For instance, income earned through tips (up to $25,000) and overtime (up to $12,500) is now deductible through 2028. Seniors also see a boost: individuals over retirement age can claim additional deductions—$6,000 per filer or $12,000 for couples filing jointly—until those provisions sunset in 2028. However, these deductions begin to phase out at income levels of $75,000 for individuals and $150,000 for couples.

Charitable giving has received special attention in this legislation. For the first time, non-itemizers will be able to deduct charitable donations starting in 2026, up to $1,000 for individuals and $2,000 for married couples filing jointly. This opens up new incentives for a broader range of households to give. However, itemizers may want to rethink their timing: beginning in 2026, the maximum deduction allowed for charitable gifts is capped at 35% of adjusted gross income (AGI), and only donations above 0.5% of AGI count toward the deduction. Corporations must exceed 1% of taxable income for deductions to apply. If maximizing charitable tax benefits is a goal, giving in 2025 may yield the best outcome.

The bill also increases the State and Local Tax (SALT) deduction cap from $10,000 to $40,000 for households earning under $500,000. This expanded cap lasts through 2029, providing temporary relief to taxpayers in high-tax states. After that, the cap will revert to previous levels.

Another significant piece of the legislation affects estate planning and family savings. The child tax credit remains at $2,200 and will continue to adjust annually. The estate and gift tax exemption increases to $15 million starting in 2026, with future inflation adjustments. Parents may also benefit from a newly introduced “Trump Account,” which provides a $1,000 initial deposit per child at birth and allows for tax-deferred contributions that can be used for education or a first home purchase—similar in spirit to 529 plans or Roth IRAs but with a broader use case.

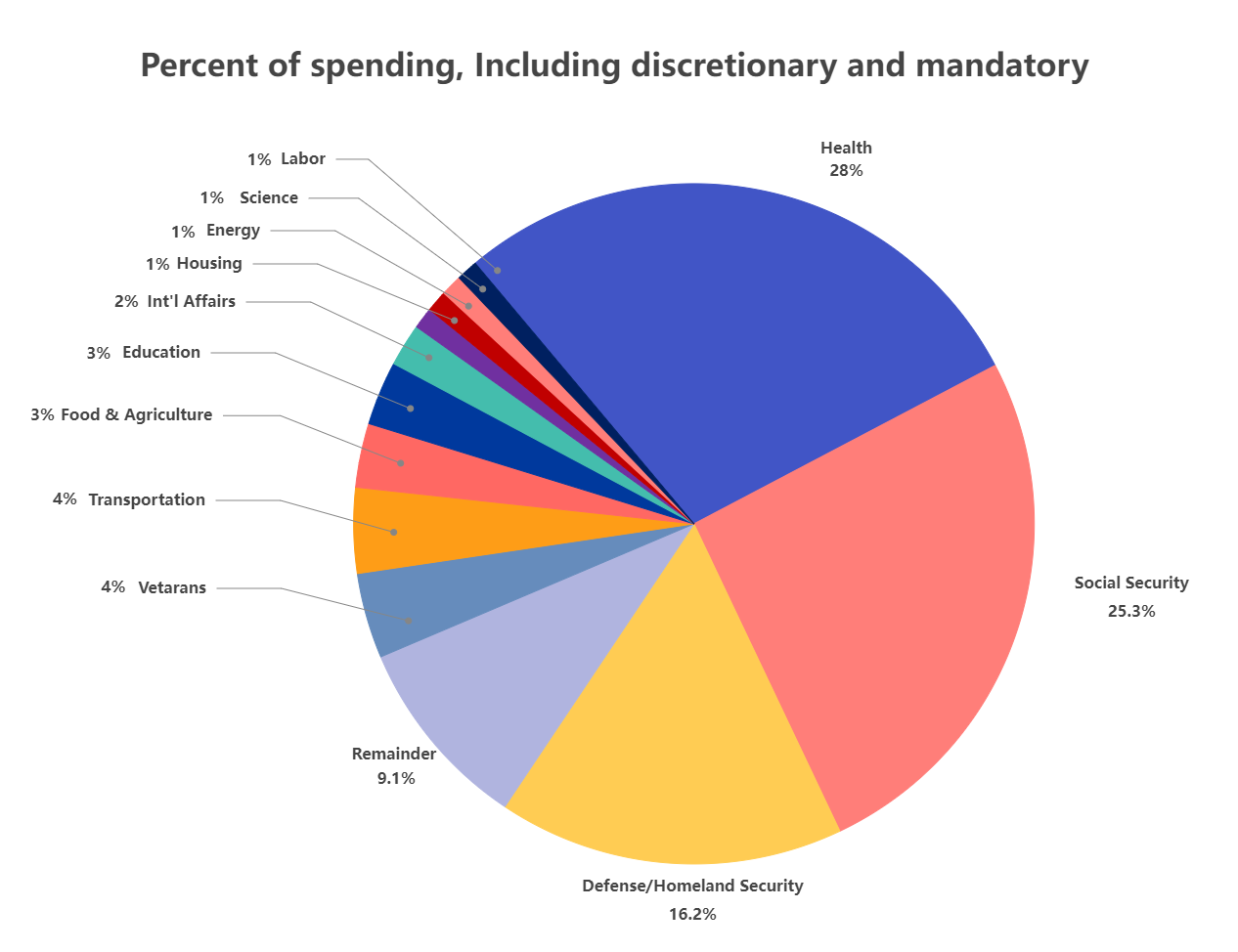

Visualizing the Federal Budget Impact

While these reforms offer benefits to many, they also carry a cost. The Congressional Budget Office estimates the bill will increase federal deficits by $2.8 trillion over the next decade. Below is a chart that helps visualize how the federal budget is divided—and why some programs like Medicare, Medicaid, and Social Security are harder to adjust year to year.

As the chart shows, a large portion of federal spending is mandatory, including entitlement programs and interest on the national debt. Discretionary spending (which Congress controls annually) makes up a smaller share.

Strategic Planning Considerations

Depending on your income level, charitable goals, and retirement timeline, the OBBB could create new opportunities—or necessitate changes to your plan. For example, high-income earners may want to bunch charitable contributions into 2025 to take advantage of the uncapped deduction before the new rules kick in. Non-itemizers can plan to begin giving in 2026 to benefit from the above-the-line deductions, and seniors should coordinate their deduction strategy alongside Social Security and Medicare planning while the temporary tax breaks are still in effect.

A Note of Caution

While these provisions can offer significant planning opportunities, it’s important to understand that not all impacts are positive. Medicaid reforms tied to this legislation could lead to a reduction in health care access for some, and the overall cost of the bill may have long-term implications for government services and taxes in the future.

Final Thoughts

The One Big Beautiful Bill is more than just tax reform—it’s a structural shift in how income, giving, and estate planning are treated in the tax code. While some households will benefit more than others, everyone can take proactive steps now to adapt to the changes. At Commons Capital, we’re here to help clients navigate these updates and develop personalized strategies that align with their values and financial goals.

This material is for informational purposes only and is not intended to provide, and should not be relied upon for, tax, legal, or investment advice. You should consult your own tax, legal, and financial advisors before making any decisions. Commons Capital, LLC is a Registered Investment Advisor.