Figuring out what a stock option is worth is more art than science, and it definitely goes beyond a simple "stock price minus exercise price" calculation. The real value is a blend of what it’s worth right now (intrinsic value) and what it could be worth in the future (extrinsic value). Understanding how to value stock options starts with grasping this fundamental concept; it's the first and most important step to valuing them like a pro.

Understanding What Drives an Option's Value

At its core, an option's total price (often called its premium) is made up of two distinct parts. Before we even touch a valuation model, you have to get comfortable with this split.

First up is intrinsic value. This is the straightforward, in-the-moment profit you’d pocket if you exercised the option today. For a call option, it's the amount the current stock price is above the strike price. If a stock is trading at $50 and your strike price is $40, the intrinsic value is $10 per share. Simple. If the stock is at or below the strike, the intrinsic value is zero.

The second piece of the puzzle, and often the more powerful one, is extrinsic value. You’ll also hear this called "time value." This represents the option's potential to become more profitable down the road. It’s the premium someone is willing to pay for the chance that the stock will make a favorable move before the option expires.

To make this crystal clear, here’s a quick breakdown of the two components.

The Two Pillars of an Option's Value

These two elements combine to create the total premium you see in the market.

The Power of Potential

So, what drives that extrinsic value? It's all about uncertainty and opportunity. The more time an option has until it expires, the higher its extrinsic value. More time simply means more chances for the stock price to climb.

Likewise, higher stock price volatility—how much a stock's price swings around—pumps up the extrinsic value. A highly volatile stock has a much better shot at making a huge price move, increasing the odds of a big payoff for the option holder. To really nail down how these components work together, it's worth understanding the nuances of Intrinsic vs Extrinsic Option Value.

An easy way to think about it is this: Intrinsic value is about the present reality, while extrinsic value is about future possibility. An option's total worth is the sum of both.

Different Perspectives on Value

It’s also crucial to remember that "value" isn't a universal number; it can be subjective. An employee who received stock options as part of their compensation package will look at them very differently than a public market trader. The employee's view is shaped by things like vesting schedules, their belief in the company's long-term growth, and their own financial planning.

A trader, on the other hand, is probably more focused on market volatility, liquidity, and short-term price action. Getting a handle on how stock options work in these different contexts gives you a much clearer picture of their true worth.

Before we jump into the valuation models, make sure you're solid on these fundamental drivers—time, volatility, and the stock-to-strike price relationship. That foundation will make the number-crunching part feel a lot more intuitive.

Getting Your Hands on the Key Valuation Inputs

Before you can nail down just how to value stock options, you have to gather the essential pieces of the puzzle. Famous models like Black-Scholes are incredibly powerful, but they're only as good as the data you feed them.

Think of it like gathering ingredients before you start cooking. If you miss one, the final dish is going to taste off. This process involves tracking down six key data points—some are easy to find, while others require a bit more digging and judgment. Let’s walk through each one so you can build your valuation on a solid foundation.

The Foundational Data Points

First, let's grab the three most straightforward inputs. You can usually find these right in your option grant agreement or with a quick online search.

- Current Stock Price: This is simply the current market price of the company's stock. For a public company, just pull it from a site like Bloomberg or Yahoo Finance. If it’s a private company, you'll typically use the most recent 409A valuation price.

- Strike Price (or Exercise Price): This is the fixed price you'll pay to buy the stock with your option. It’s spelled out clearly in your option grant paperwork.

- Time to Expiration: This is the lifespan of the option, measured in years. If your option expires in two years, you’ll use 2.0. If it's six months, you’ll use 0.5.

These three inputs set the stage. The gap between the stock price and the strike price gives you the option's intrinsic value, while the time to expiration is a huge driver of its extrinsic, or "time," value.

Inputs That Need a Little More Analysis

The next few inputs require a bit more thought and a real understanding of market dynamics. Honestly, these are the variables that often have the biggest impact on the final number you get.

Risk-Free Interest Rate

This input represents the return you could get on an investment with virtually zero risk over the life of your option. It’s how we account for the time value of money. The gold standard here is the yield on a U.S. Treasury bill or bond with a maturity date that's closest to your option's expiration.

For instance, if your stock option expires in five years, you’d look up the current yield on a 5-year U.S. Treasury note. This rate sets a baseline for the opportunity cost of having your capital tied up.

Dividend Yield

If the company pays dividends, you absolutely have to factor that in. Dividends actually reduce the stock price on the ex-dividend date, which hurts the value of a call option. You can usually find a company’s dividend yield on most financial data sites. A more thorough approach is to review past payments; our guide on how to analyze financial statements can show you exactly where to look.

The Most Critical Input: Volatility

Finally, we get to the most challenging—and most influential—input of them all: volatility. This metric is all about how much a stock's price is expected to swing around over the option's life. Higher volatility means a greater chance of big price movements, which increases the potential upside and, therefore, the option's value.

You'll encounter two main types:

- Historical Volatility: This is calculated from the stock's past price behavior. It’s a decent starting point but isn't always the best predictor of what's to come.

- Implied Volatility (IV): This is the market's real-time forecast of future volatility, which is derived from the prices of options currently trading on that stock. It’s a direct reflection of market sentiment and expectations.

Implied volatility is arguably the most crucial input because it directly impacts option premiums. When uncertainty surges, options reprice in a hurry. Just look at the March 2020 market crash. The implied volatility for S&P 500 options (measured by the VIX) spiked to a historic high of 82.69—miles above its long-term average near 20. It's a perfect example of how quickly fear can get priced into the market.

Choosing the Right Valuation Model

With your key inputs gathered, you're standing at a fork in the road. Knowing how to value stock options effectively now comes down to selecting the right mathematical tool for the job. Two models have dominated financial analysis for decades: the Black-Scholes model and the Binomial model.

While they both aim to find an option's fair value, they approach the problem from different angles. One is a precise, elegant formula for a single moment in time, while the other maps out a series of potential future paths. Your choice will hinge on the type of option you hold and the level of flexibility you need.

The Black-Scholes Model: A Formula for a Specific Moment

The Black-Scholes model is arguably the most famous method for valuing stock options. It's a single, powerful formula that calculates a theoretical price based on the six inputs we just discussed. Its primary advantage is speed and simplicity—once you have your inputs, you can get a price almost instantly.

This model is the go-to standard for a very specific type of option: European options. These can only be exercised on their expiration date. Since there's only one possible exercise date, a single, direct calculation works perfectly.

- Best for: European-style options that cannot be exercised early.

- Pros: It's fast, widely accepted, and relatively easy to implement in a spreadsheet.

- Cons: Its biggest weakness is its rigidity. It assumes volatility and interest rates are constant, and it doesn't account for the possibility of early exercise.

Because of these assumptions, the Black-Scholes model can struggle with the nuances of certain real-world scenarios, particularly when valuing employee stock options that often have unique features.

The Binomial Model: Mapping Out Future Possibilities

If Black-Scholes is a snapshot, the Binomial model is a flipbook. Instead of a single formula, it breaks down the time to expiration into many discrete steps, creating a "tree" of potential future stock prices. At each step, the price can move up or down by a specific amount.

The model then works backward from the expiration date, calculating the option's value at every possible price point along the way. This step-by-step approach makes it far more flexible and intuitive.

Its key advantage is its ability to handle American options, which can be exercised at any time before expiration. The Binomial model can check at each "node" of the tree whether exercising the option early is more profitable than holding it. This is a critical feature that the standard Black-Scholes model simply cannot accommodate.

The Binomial model's strength lies in its adaptability. It's the superior choice for options with flexible exercise dates or complex features like vesting schedules, which are common for employee stock options (ESOs).

Which Model Should You Use?

Making the right choice comes down to the specifics of your option grant. Here’s a quick comparison to guide your decision:

For most employees holding standard incentive stock options or non-qualified stock options, the Binomial model is the more appropriate tool. The ability to factor in early exercise decisions is not just a theoretical benefit—it can have a material impact on the calculated value, especially when a company pays dividends or undergoes significant price changes.

While 72% of top companies granted performance shares in 2011, stock options remain a key component of compensation, and valuing them correctly is essential. Using a model that mirrors their actual structure is the only way to get a truly reliable estimate of their worth.

A Real-World Valuation Walkthrough

Theory and models are great, but the real test is seeing them in action. To truly get a feel for how to value stock options, we have to roll up our sleeves and work through a practical example. Let's value a grant for a fictional tech company, "Innovate Solutions Inc.," using the well-known Black-Scholes model.

This exercise will take all those abstract concepts and turn them into hard numbers, showing you exactly how each input pulls the final value up or down.

Setting the Scene at Innovate Solutions

Let's say you've been granted 1,000 stock options at Innovate Solutions. To kick off the valuation, we need to lay out the terms of the grant and the company's current financial picture. We'll use the six key inputs we gathered earlier.

Here are the details for our scenario:

- Company: Innovate Solutions Inc. (a publicly-traded tech firm)

- Current Stock Price (S): $100 per share

- Strike Price (K): $90 per share (This is the price you'll pay to exercise)

- Time to Expiration (t): 2 years

- Stock Price Volatility (σ): 30% (or 0.30)

- Risk-Free Interest Rate (r): 4% (0.04), based on the 2-year U.S. Treasury yield

- Dividend Yield (q): 1% (0.01), as Innovate Solutions pays a small dividend

With these variables locked in, we have everything the Black-Scholes formula needs to do its job and calculate a theoretical value for a single call option.

Plugging the Numbers into the Model

The Black-Scholes formula itself is pretty gnarly, full of cumulative distribution functions and natural logarithms. The good news? We don't need to solve it by hand. Dozens of free online calculators and spreadsheet functions can do the heavy lifting in an instant.

Our goal here isn't to become mathematicians. It's to understand what the formula is doing conceptually. At its core, it's balancing the immediate, locked-in profit (intrinsic value) against the future potential (extrinsic value), while making smart adjustments for the time value of money and any dividends.

When we feed our Innovate Solutions data into a Black-Scholes calculator, it spits out a theoretical value of approximately $21.40 per option.

Key Takeaway: Each of the 1,000 options you hold is theoretically worth $21.40. This means the total grant has a current estimated value of $21,400 ($21.40 x 1,000 shares).

This isn't just some random number. It's a carefully calculated estimate of fair value based on today's market conditions. It's what an informed investor might be willing to pay for the right to buy Innovate Solutions stock at $90 over the next two years.

Interpreting the Valuation Result

Let's tear apart that $21.40 figure. We know the stock is trading at $100 and our strike price is $90.

- The intrinsic value is $10 ($100 - $90). This is the "in-the-money" profit you'd make if you exercised today.

- The remaining $11.40 ($21.40 - $10) is the extrinsic value.

That extrinsic value is the premium the market is placing on the stock's potential over the next two years. It's the value of time, opportunity, and uncertainty, driven mostly by that 30% volatility and the 4% risk-free rate.

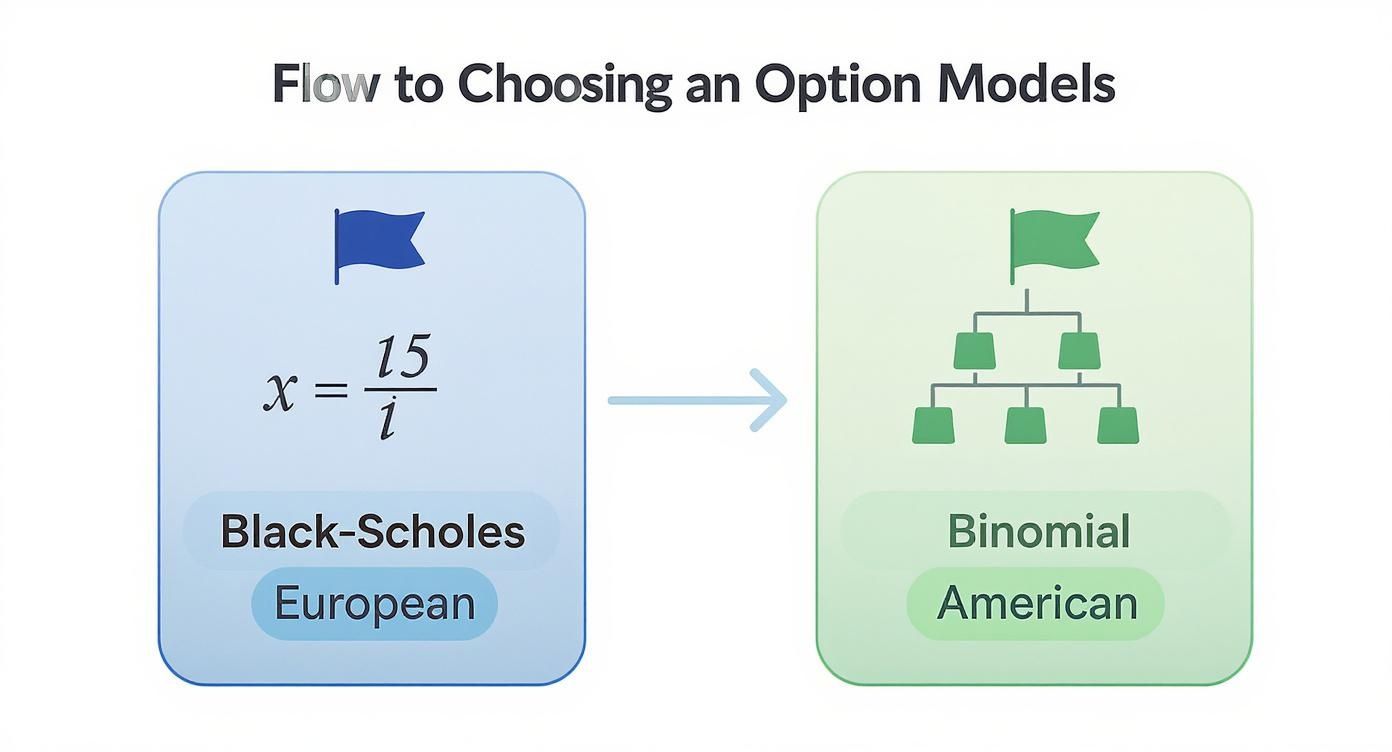

Picking the right model is a critical first step to getting a number that actually means something, as different situations call for different tools.

This infographic shows a simple decision tree for choosing between the Black-Scholes and Binomial models based on the option type.

As you can see, European options (which can only be exercised at expiration) are a perfect fit for the Black-Scholes formula. The more flexible American options, however, are often better handled by the Binomial model's tree-based approach.

How a Single Change Impacts Value

Valuations are not set in stone; they're a snapshot in time. To see just how sensitive the price is, let's tweak just one input: volatility.

Imagine some market-moving news causes Innovate Solutions' volatility to spike from 30% to 45%. Everything else stays the same. Running the calculation again, the option's value jumps from $21.40 to around $28.50.

That's a 33% increase in value from changing a single variable. This is exactly why volatility is often called the most important input in option pricing. More uncertainty creates a wider range of possible future stock prices. Because an option's downside is capped (you can't lose more than you paid for it) but its upside is theoretically unlimited, that extra uncertainty makes it more valuable.

This kind of hands-on walkthrough gives you a framework for not just calculating a number, but for understanding the story it tells.

Going Beyond Price with The Greeks

A calculated price from a model like Black-Scholes gives you a valuable snapshot, but it doesn't tell the whole story. To really get a feel for an option's personality and how it will behave in the real world, you need to look past a single price tag and meet "the Greeks."

These five key metrics are like a dashboard for your option, showing you how its value is likely to react to shifts in the market. Think of them less as abstract numbers and more as a powerful set of risk management tools that reveal the forces acting on your option's price. Understanding them is what moves you from static valuation to proactive, dynamic analysis.

Delta: The Speed of Your Option

Delta is the first and most fundamental Greek. It tells you exactly how much your option's price is expected to change for every $1 move in the underlying stock. It’s the most direct measure of an option's sensitivity to the stock's price.

For example, a call option with a Delta of 0.60 should theoretically increase in value by $0.60 if the stock price rises by $1. On the flip side, it would lose $0.60 if the stock falls by $1.

Key Takeaway: Delta is more than just a sensitivity metric; it's also a rough approximation of the probability that an option will finish in-the-money at expiration. A Delta of 0.60 suggests roughly a 60% chance of that happening.

Gamma: The Accelerator

If Delta is the speed, Gamma is the acceleration. It measures how fast an option's Delta changes. In simpler terms, Gamma tells you how much your Delta will change for every $1 move in the stock.

Options with high Gamma are highly responsive. Their Deltas will change rapidly as the stock price moves, which is a common trait for options that are near the strike price and close to expiration. A high Gamma can lead to explosive gains or rapid losses, making it a critical metric for active traders to watch.

Vega: The Volatility Gauge

Vega is the Greek that measures an option's sensitivity to changes in implied volatility (IV). It tells you how much the option's price will change for every 1% change in IV. Since volatility is a massive driver of an option's extrinsic value, Vega is an incredibly important metric.

If an option has a Vega of 0.15, its price will increase by $0.15 for every 1% rise in implied volatility, all else being equal. This is exactly why options get more expensive during uncertain market conditions—investors are pricing in a higher chance of big price swings.

The Greeks are universally recognized statistical measures for assessing option risk. Vega's impact is tangible; a 1% increase in IV can boost the price of a one-month at-the-money SPY option by about $0.25. Meanwhile, Delta shows how directly an option's price is tied to the stock. You can explore more insights on option pricing to see these metrics in action.

Theta: The Time Decay Clock

Theta is the one Greek that is always working against the option buyer. It quantifies the rate of time decay, showing how much value an option loses each day as it creeps closer to expiration. This erosion of extrinsic value is relentless and predictable.

An option with a Theta of -0.05 will lose $0.05 of its value every single day, just from the passage of time. Theta's effect accelerates dramatically as the expiration date gets closer, which is why long-dated options are less susceptible to its immediate impact. For anyone holding options, understanding Theta is crucial for timing your trades.

Rho: The Interest Rate Sensor

Finally, Rho measures an option's sensitivity to changes in interest rates. It shows how much an option's price will change for every 1% move in the risk-free interest rate. Of all the Greeks, Rho generally has the least impact on an option's value, especially for shorter-term contracts.

Higher interest rates tend to make call options slightly more valuable and put options slightly less so. While it's a factor in formal valuation models, Rho is often a secondary consideration in day-to-day risk management unless you are dealing with very long-term options.

Connecting Models to Market Realities

Valuation models are fantastic for giving you a clean, theoretical number. But the real market? It's a far messier place. Once you’ve figured out how to value stock options with a model, the next critical step is understanding why the market price might be telling a completely different story. These models are powerful, but they operate in a vacuum, completely ignoring the gritty, real-world forces that shape an option's true tradable value.

The market doesn't run on pure math; it's driven by supply, demand, and raw human sentiment. A sudden news event, an earnings report that misses expectations, or just a shift in investor mood can send an option's price soaring or crashing, totally disconnected from its model-derived value. Think of the model's output as a baseline—a starting point that you have to adjust for real-world friction.

The Impact of Liquidity and Spreads

One of the biggest disconnects between theory and reality comes down to liquidity. In a perfect model, you can trade an option at its "fair value" in an instant. But in the real world, you have to deal with the bid-ask spread—that gap between the highest price a buyer is willing to pay (the bid) and the lowest price a seller is willing to accept (the ask).

For thinly traded options, especially on smaller companies, this spread can be massive. It’s a significant hidden cost. Your model might tell you an option is worth $2.50, but if the bid is $2.20 and the ask is $2.80, the immediate, practical value is far from what the theory suggests.

The truth is, most options on major U.S. exchanges rarely trade at their exact model-derived value. Liquidity, those bid-ask spreads, and the very structure of the market play decisive roles. For highly liquid options on the S&P 500, the spread can be as tight as 1–5 cents. But for less liquid contracts, it’s not uncommon to see spreads of $0.10–$0.50.

Bringing Theory to the Trading Floor

Ultimately, a valuation model gives you a critical piece of the puzzle, but it’s not the whole picture. For private company employees, this often circles back to knowing what the underlying asset is actually worth, which is where learning about what is a 409A valuation becomes absolutely essential. For public market traders, it's about seeing the model's output through the lens of live market mechanics.

Key Takeaway: A valuation model tells you what an option should be worth in a perfect world. Market analysis tells you what it is worth right now, given all the real-world complexities.

To see how these concepts connect to actual trading, exploring specific options strategies like bull put spreads can offer some great insights into practical application and risk management. Fusing a solid theoretical valuation with a sharp understanding of market dynamics is what separates a novice from an expert.

Common Questions About Valuing Stock Options

Even after you've got a handle on the valuation models and market dynamics, a few tricky questions always seem to pop up when you're learning how to value stock options. Getting clear on these finer points is what builds real confidence in your numbers and helps you make smarter financial moves. Let's tackle some of the most common ones I hear.

How Do I Value Options in a Private Company?

This is a big one. Valuing options in a private, pre-IPO company is a unique challenge because there’s no public stock price to plug into your model.

The whole valuation really hinges on the company's most recent 409A valuation. This is a formal appraisal that establishes the fair market value (FMV) of the company's common stock, and it becomes the "Current Stock Price" you need for a model like Black-Scholes.

But what about volatility? That's much harder to pin down without public trading data. The standard practice is to look at the historical volatility of comparable public companies in the same industry. It’s an estimate, but it's a well-established, reasonable approach.

What Is a Fair Percentage of Equity to Receive?

This is probably the most frequent question I get from startup employees. The truth is, "fair" depends entirely on context.

A few factors make all the difference:

- Company Stage: An early hire (say, one of the first 10 employees) should expect a much larger equity stake than someone joining a well-funded, late-stage startup with hundreds of employees.

- Your Role and Level: A VP of Engineering or a key machine learning hire is going to command a higher equity grant than a junior-level employee. Seniority and impact matter.

- Industry Norms: Tech startups are known for offering more generous equity packages than companies in more traditional sectors.

Don't get fixated on the raw number of shares. The number that really matters is your ownership percentage. Always ask for the total number of fully diluted outstanding shares to figure out what you truly own.

Here’s a pro tip: Ask a potential employer how they determine their option grants. A well-run company should have a structured, transparent process that maps roles and levels to specific equity bands. This ensures fairness across the board.

How Does Vesting Affect an Option's Value?

This is a subtle but crucial point. A vesting schedule doesn't technically change the theoretical value of a single stock option calculated by a model. That number is what it is.

However, vesting has a massive practical impact on the total value of your grant. Unvested options are worth exactly zero to you because you don’t own them yet. Simple as that.

If you leave the company before your grant is fully vested, you walk away from the unvested portion. So, when you're sizing up the total potential worth of your compensation, you have to factor in the timeline over which you'll actually earn the right to those shares.

At Commons Capital, we help clients cut through the complexity of equity compensation and make it a core part of their financial strategy. If you need an expert to help you value your stock options or plan for the future, contact Commons Capital today.