When it comes to gifting assets to a minor, the core difference between UGMA and UTMA accounts lies in one critical detail: the type of assets you can contribute. Understanding this distinction is the first step in choosing the right path for your family's wealth transfer strategy.

A UGMA (Uniform Gifts to Minors Act) account is a straightforward vehicle designed for financial assets like cash, stocks, and bonds. However, if you plan to gift more complex assets such as real estate, valuable art, or intellectual property, you will need the expanded flexibility of a UTMA (Uniform Transfers to Minors Act) account.

Breaking Down Custodial Accounts

Both UGMA and UTMA accounts offer a simple, effective way to give a child a financial head start without the complexity and cost of establishing a formal trust. They function as custodial accounts, meaning an adult (the custodian) manages the assets on behalf of a minor beneficiary. It's crucial to understand that any contribution is an irrevocable gift—once transferred, the asset legally belongs to the child.

The custodian is bound by a fiduciary duty to manage the account in the child's best interest until they reach the age of majority as defined by state law. At that point, the custodian's role ends, and the beneficiary gains full, unrestricted control over all the assets in the account.

While these accounts are praised for their simplicity, they aren't the perfect solution for every situation. For individuals who require more control over asset distribution, it's wise to explore whether you need a trust instead.

Key Differences: UGMA vs UTMA at a Glance

To truly grasp the contrast, it helps to compare these two accounts directly. The most significant distinction is the type of property you can contribute, which often becomes the deciding factor for families planning their wealth transfer.

The choice between UGMA and UTMA almost always comes down to the nature of the gift itself. If you're gifting traditional securities, a UGMA works just fine. For anything else, from a plot of land to a family patent, a UTMA is the only way to go.

Here's a quick rundown of the primary features of each account.

As you can see, while they share a similar purpose, the UTMA provides significantly more flexibility in both the types of assets it can hold and, often, a later age for the final transfer of control.

When you’re weighing a UGMA vs. an UTMA, the single most critical question to ask is: what exactly are you planning to give? This isn't just a small detail—it's the fundamental distinction that can make or break your gifting strategy and dictates which account is even an option for you.

Think of it this way: UGMA is the specialist, designed for traditional financial products. UTMA is the generalist, ready to handle almost anything you can throw at it.

What You Can Put in a UGMA

The original Uniform Gifts to Minors Act (UGMA) had a very clear mission: make it simple to gift financial instruments to kids. That’s it. As a result, its scope is deliberately narrow, focusing on assets that a bank or brokerage can easily hold and manage.

Here’s what a UGMA account can hold:

- Cash: The easiest gift of all, ready to be deposited and put to work.

- Securities: This covers the classics—individual stocks, bonds, and mutual funds.

- Insurance Products: You can also contribute assets like life insurance policies or annuities.

This straightforward approach makes UGMA a fantastic choice if your strategy revolves around building a portfolio of traditional investments. If you want to gift shares of Apple or start a mutual fund for your grandchild, a UGMA is perfectly suited for the job.

But its limits become obvious the moment your family’s wealth includes non-financial assets. You simply can't use a UGMA to gift a piece of the family cabin or a valuable painting. And that’s precisely why the UTMA was created.

The All-Encompassing Nature of UTMA

The Uniform Transfers to Minors Act (UTMA) came later, and it was a massive upgrade. It recognized that wealth isn't just stocks and bonds, providing a framework to gift nearly any kind of property to a minor.

The history here is important. UGMA accounts were first established back in 1956, and their limitations were clear. While they were stuck with financial assets, the later-developed UTMA accounts can hold pretty much anything of value—real estate, cars, fine art, and even intellectual property. As detailed by experts at The College Investor, this evolution dramatically expanded planning options for families across the country.

This flexibility unlocks a world of possibilities for high-net-worth families with diverse assets.

For families with significant non-liquid assets, the UTMA isn't just an option—it's a necessity. It provides the only streamlined custodial path to transfer tangible property, business interests, or unique intellectual rights to the next generation without the complexity of a formal trust.

Just think about the real-world assets you could place in a UTMA:

- Real Estate: A partial interest in a rental property or a vacation home.

- Fine Art: Ownership of a valuable painting or sculpture.

- Intellectual Property: The rights to patents, trademarks, or music royalties.

- Private Business Interests: A minority stake in a family-owned company.

This makes UTMA an incredibly powerful tool for sophisticated estate planning. It allows families to pass down a legacy that reflects the true nature of their wealth, ensuring that unique and often illiquid assets are part of a minor’s long-term financial future.

How Age of Majority Rules Vary by State

Aside from the types of assets you can hold, the biggest real-world difference between a UGMA and a UTMA is when the child gets the keys to the kingdom. This isn’t some arbitrary date; it’s the “age of termination,” and it’s dictated entirely by state law. For anyone setting aside a serious amount of money, this is a detail you absolutely cannot afford to overlook.

Let’s be clear: this transfer of control isn’t a friendly suggestion. It's a hard-and-fast legal requirement. The day the beneficiary hits the state-mandated age, the custodian’s job is over. The assets become the sole property of the former minor, with no strings attached.

The Standard Ages for UGMA and UTMA

Generally, UGMA accounts track with the traditional age of legal adulthood. In most states, that means control of the account shifts when the beneficiary turns 18. This can be a double-edged sword, giving them cash for early life goals but also handing a lump sum to a teenager who might not have the financial discipline to manage it.

UTMA accounts, on the other hand, usually give you a longer runway. While UGMA accounts often terminate at age 18, UTMA rules typically push that out to 21, and some states even let it extend to 25. This is a critical planning point. In fact, a common piece of advice from financial planners is to never commingle UGMA and UTMA assets, because the earlier 18-year-old termination date from the UGMA could accidentally apply to the whole pot. You can find more on these crucial distinctions in this guide on custodial account regulations on lifetimeplanning.biz.

The extended timeline that many state UTMA laws offer is a massive strategic advantage. Pushing control out to age 21 or 25 gives a young adult invaluable time to mature and learn how to handle a significant amount of money responsibly.

This delay can mean the difference between a windfall arriving mid-freshman year of college versus after graduation, when they’re starting a career and thinking about the future.

State-by-State Nuances You Cannot Ignore

It’s crucial to remember that these are just general guidelines. The exact age of termination is set by the specific UTMA or UGMA statute in the minor's state of residence, creating a complex patchwork of rules across the country.

For instance, a state like California might allow a UTMA to be extended to age 25 if the donor specifies it, while a neighboring state could have a hard cap at 21. This variability makes doing your homework essential.

To see just how much these rules can differ, take a look at the table below. It offers a quick snapshot of the termination ages in a few key states, but remember that laws can and do change.

Typical Age of Termination by Account Type and State

This table provides illustrative examples and is not a substitute for legal advice. Always verify the current laws in your specific state before making any decisions.

The key takeaway here is simple: never assume. The details matter, and they can have a huge impact on when and how your gift is ultimately received.

Strategic Planning Around the Age of Majority

The age of termination should be a central part of your decision-making process. If the thought of an 18-year-old managing a large portfolio gives you pause, a UTMA in a state that allows termination at 21 or 25 is likely the smarter move.

Here are a few things to think through before you open an account:

- Verify Your State's Law: Don't guess. Before you do anything, confirm the specific age of termination rules for both UGMA and UTMA accounts in the relevant state.

- Consider the Beneficiary: Be honest about the minor's maturity and financial sense. Are they ready for this kind of responsibility at 18, or would a few more years make a world of difference?

- Evaluate the Amount: For smaller gifts, the risk of an earlier transfer might be acceptable. But for substantial six- or seven-figure accounts, delaying control is a critical risk-management tool.

Ultimately, the flexibility around the termination age is one of the most powerful features of a UTMA. It gives you, the donor, a much greater say in the timing of your gift, making it far more likely that the money will be used wisely.

Analyzing Tax Rules and Financial Aid Impact

Beyond the legal differences in asset types and state laws, the real financial impact of choosing between a UGMA and UTMA account comes down to taxes and college financial aid. This is where the rubber meets the road. These two factors can dramatically change the long-term value of your gift and need to be at the center of your planning conversations.

The moment you move assets into a custodial account, you've made an irrevocable gift. That's a critical point. The assets now legally belong to the minor, which kicks off a few immediate consequences. On the upside, your contributions typically fall under the annual gift tax exclusion, which means you can pass along significant wealth over the years without worrying about gift or estate taxes.

But once the gift is made, any income it generates—dividends, interest, capital gains—is taxable. And that’s where things get complicated.

Unpacking the Kiddie Tax Rules

Because the money belongs to the child, the investment income is subject to the infamous "kiddie tax." These rules were put in place to stop high-income families from parking investments in their kids' names just to get a lower tax rate. It’s an anti-loophole measure.

The kiddie tax has a tiered system that the IRS adjusts for inflation. For 2024, it breaks down like this:

- The first $1,300 of unearned income is completely tax-free.

- The next $1,300 is taxed at the child's own, usually very low, tax rate (often 10%).

- Anything over $2,600 gets hit with the parents' higher marginal tax rate.

What this means in practice is that while these accounts offer a small tax break for modest gains, a large account with significant earnings can quickly push the child into their parents' tax bracket. This can create a surprisingly large tax bill each year, wiping out much of the intended tax-shifting benefit.

The Critical Impact on Financial Aid Eligibility

This is the big one. Perhaps the most glaring financial drawback of UGMA and UTMA accounts is how they can torpedo a student's eligibility for college financial aid. It's a detail that many people miss, and it’s a massive differentiator when comparing these accounts to other options like 529 plans.

When a student fills out the Free Application for Federal Student Aid (FAFSA), the formula treats assets very differently based on ownership. Assets owned by parents only have a modest impact on the Student Aid Index (SAI), which determines aid eligibility.

But—and this is the key—assets in a UGMA or UTMA account are the legal property of the student. So, they have to be reported as student assets on the FAFSA.

The FAFSA formula comes down hard on student-owned assets. This single detail can dramatically reduce a student's financial aid package, often wiping out the very benefit the savings were intended to create.

Under the current FAFSA methodology, student assets held in UGMA and UTMA accounts are assessed at a rate of 20%. Compare that to parental assets, which are assessed at a maximum of 5.64%.

Let’s put that into perspective. If a student has $10,000 in a custodial account, it could increase their SAI by $2,000, reducing their aid eligibility by that much. That same $10,000 in a parent-owned 529 plan would only increase their SAI by a maximum of $564. You can dig deeper into these calculations with these insights on UGMA vs. UTMA custodial accounts.

This huge difference means that for every dollar saved in a custodial account, a student could lose a substantial amount in need-based grants, scholarships, and subsidized loans. For any family that even thinks they might apply for financial aid, this makes UGMA and UTMA accounts a risky choice for college savings. It's why many planners steer clients toward alternatives like 529 plans, where the funds are treated much more favorably in the aid formula.

Choosing the Right Account for Your Goals

Knowing the difference between a UGMA and a UTMA is one thing; applying that knowledge is another. The "right" choice isn't a universal answer—it comes down to what you're trying to accomplish, the specific assets you want to gift, and your long-term vision for the child.

Think of it this way: if your plan is to gift a straightforward portfolio of stocks and mutual funds, a UGMA account is your clean, simple, no-frills vehicle. It was designed for exactly that.

But what if a grandparent wants to pass down a 10% share in the family lake house? A UGMA account can't touch that. This is precisely where a UTMA steps in, built to handle tangible assets like real estate, art, or even intellectual property.

Scenarios Favoring UGMA or UTMA

The decision often boils down to a few key questions about your gifting strategy. When weighing your options, running through a comprehensive due diligence checklist can help clarify the financial and legal angles, ensuring you land on a well-informed decision.

Here are a few common situations:

- For a Simple Stock Portfolio: An aunt wants to gift her nephew $15,000 in blue-chip stocks. A UGMA is the perfect fit—it’s easy to set up and manage for these standard financial assets.

- For Gifting a Unique Asset: An artist wants her child to inherit the future royalties from her creative work. A UTMA is the only custodial account that can hold this type of intellectual property.

- For an Undecided Future Use: A family wants to build a flexible nest egg for their child that could become a down payment on a house, seed money for a business, or pay for college. The lack of restrictions makes either account a good choice, as long as the family understands the potential hit to financial aid eligibility.

The real power of a custodial account is its flexibility. Once the child takes control, that money can be used for anything. Unlike a 529 plan, the funds aren’t locked into educational expenses, giving them total freedom to pursue any life goal.

This flexibility is a massive draw, but it also brings a huge responsibility. It’s absolutely critical to teach the beneficiary about sound money management to ensure the gift is a launching pad, not a liability. Our guide on how to teach kids about money is a great place to start those conversations.

When to Consider Alternatives

While UGMA and UTMA accounts are solid tools, they aren’t a silver bullet. The major drawbacks—especially the hit to financial aid and the fact that you permanently give up control—mean other vehicles are often a much better fit for specific goals.

For Education-Focused Savings: The 529 Plan

If saving for college is the number one priority, a 529 plan is almost always the smarter move. Here’s why:

- Better for Financial Aid: As we've covered, 529s are considered parental assets on the FAFSA. This means they have a much smaller impact on aid eligibility compared to UGMA/UTMA funds, which are counted as student assets.

- Tax-Advantaged Growth: Your contributions grow tax-deferred, and withdrawals for qualified education expenses are 100% tax-free.

- You Keep Control: The account owner—usually a parent or grandparent—retains control of the funds indefinitely. You can change the beneficiary or decide when and how the money is used.

For Retirement Savings: The Custodial Roth IRA

If your child or grandchild has earned income from a summer job or part-time work, a Custodial Roth IRA is an unbelievably powerful tool for long-term wealth building.

- Decades of Tax-Free Growth: Contributions grow tax-free, and qualified withdrawals in retirement are also tax-free. It’s one of the best ways to harness the power of compounding.

- Contribution Limits Apply: You can only contribute up to the annual IRA maximum or the child's total earned income for the year, whichever is less.

- Built-in Flexibility: The original contributions (but not the earnings) can be withdrawn tax-free and penalty-free at any time. This gives the child a safety net for major goals, like buying their first home.

At the end of the day, the right account is the one that aligns with your specific objective. A UTMA is perfect for gifting a piece of property, a 529 is king for education funding, and a Custodial Roth IRA is an unmatched way to jump-start retirement savings.

How to Open and Manage a Custodial Account

Setting up a UGMA or UTMA is a fairly straightforward process, but your role as the custodian comes with serious responsibilities. Getting it right involves a few key legal and financial steps, all designed to ensure you’re acting in the minor’s best interest from day one until the day you hand over the assets.

First things first, you need to pick a financial institution. Most of the big names—brokerages, banks, and investment firms—offer custodial accounts. When you're weighing your options, look at the investment choices available, what the fees look like, and the quality of their customer support.

Once you’ve landed on a provider, it’s time to gather the necessary paperwork for both the child and yourself as the designated custodian.

Gathering the Necessary Information

To get the account open, you’ll need some basic details:

- For the Minor: You absolutely must have their full legal name, date of birth, and Social Security number.

- For the Custodian: You’ll provide your own name, address, date of birth, and Social Security number.

- Successor Custodian: This is a big one. It's incredibly wise to name a successor custodian who can step in if you're ever unable to manage the account.

For new parents, this initial setup phase is a perfect time to get all your ducks in a row. Our financial planning checklist for new parents can be a huge help in making sure you have all the essential documents organized.

Fulfilling Your Fiduciary Responsibilities

Here's where the rubber meets the road. As the custodian, you have a fiduciary duty to manage this account solely for the benefit of the minor. This isn't just a suggestion; it's a legal obligation that demands careful attention. You're on the hook for making prudent investment decisions, keeping meticulous records of every single transaction, and filing annual tax returns on any income the account generates.

A custodian's role is not just to grow the assets, but to protect them. Every decision must be made with the child's best interest as the only priority, free from any personal benefit or conflict of interest.

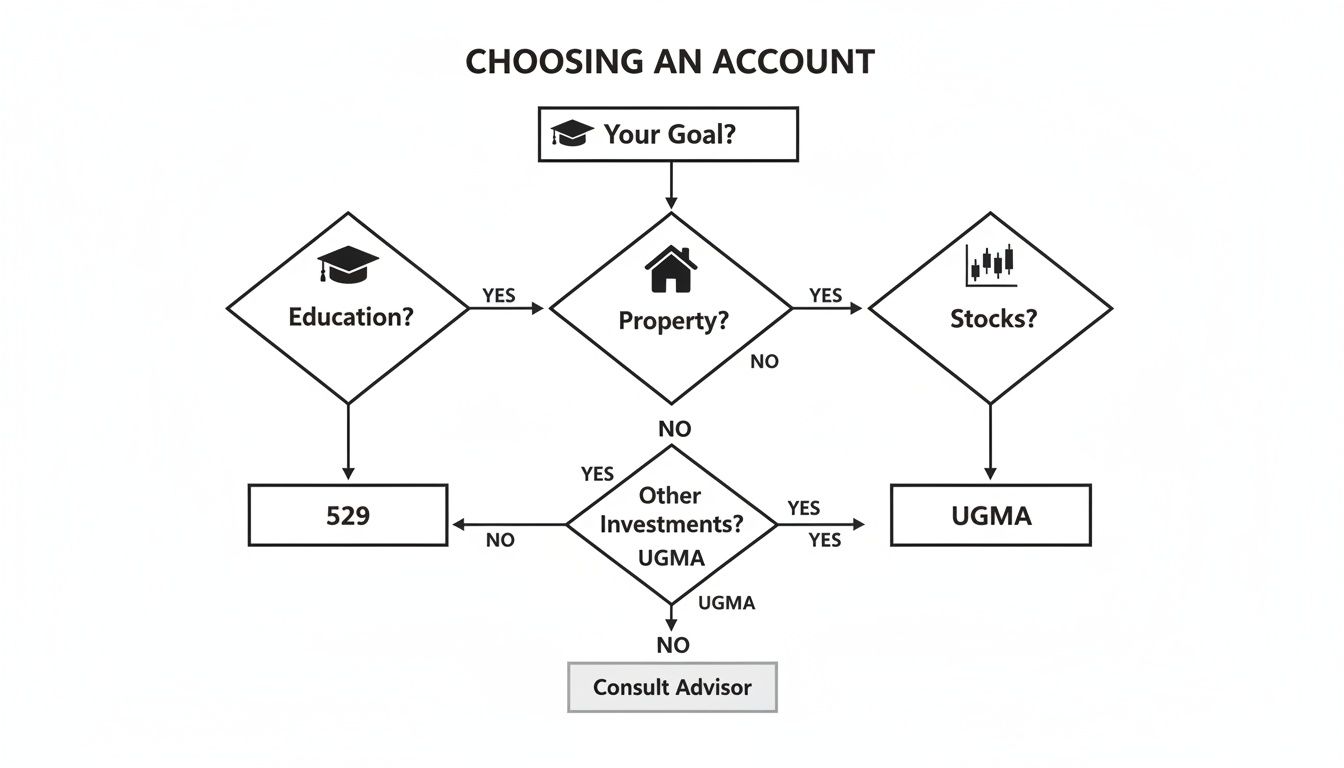

The flowchart below can help you visualize how your initial gifting goals might point you toward one account over another.

As the guide shows, the type of asset you plan to gift—whether it's cash and securities, real estate, or something else—is the fundamental factor that drives the difference between UGMA and UTMA.

Transferring Control at the Age of Majority

The final phase is perhaps the most critical: the transfer of assets. When the beneficiary hits the age of termination in your state, your job as custodian is officially over. At that point, you are legally required to hand over control of all account assets to them. This usually involves some paperwork with the financial institution to re-register the account in the beneficiary's name, giving them full, unrestricted access to the money.

Common Questions About UGMA vs UTMA

When you start digging into the details of custodial accounts, a few key questions always seem to pop up. Let's walk through some of the most frequent ones I hear from clients to clear up any confusion.

Can I Convert a UGMA Account to a UTMA Account?

The short answer is no—you can't just flip a switch and turn a UGMA into a UTMA. The assets were gifted under the specific legal rules of the UGMA, and that framework is pretty rigid.

The most straightforward approach is to wait until the minor hits the age of termination for that account. Once the assets are legally theirs, they can liquidate them and use the cash to open any new account they choose. Trying to force a conversion or combine accounts before then is a recipe for legal headaches, so it’s always best to talk it over with a financial advisor first.

What Happens If the Custodian Passes Away?

This is a critical "what if" scenario. If a custodian dies before the minor comes of age, a successor custodian needs to step in. Ideally, you named one right when you opened the account.

If a successor wasn't designated, the process gets messy. It often requires going to court to have a new one appointed, which is a slow, expensive ordeal nobody wants.

Naming a successor custodian from day one is one of the most important things you can do. It’s a simple step that ensures the account continues to be managed for the child’s benefit without any legal snags or costly delays.

Think of it as cheap insurance—a little bit of foresight that protects the child's assets and makes sure your original intentions are honored.

Are Contributions to UGMA and UTMA Tax-Deductible?

This is a common misconception. Contributions to UGMA or UTMA accounts are not tax-deductible for the person making the gift. The IRS views them as completed gifts to the minor, plain and simple.

However, these gifts do fall under the annual federal gift tax exclusion. For 2024, that means you can give up to $18,000 per person without even having to file a gift tax return. Over time, this makes these accounts a really effective way to transfer wealth to the next generation and strategically shrink the size of your taxable estate.

Can the Money in an UGMA or UTMA Be Used for Anything?

Absolutely. Once the beneficiary reaches the age of termination and the assets are turned over, they have total control. The money is theirs to use for a down payment on a house, a new car, a backpacking trip through Europe—anything at all. There are zero restrictions.

This is a huge departure from accounts like 529 plans, where the funds are earmarked strictly for qualified education expenses. While the custodian is legally bound to manage the funds for the minor's benefit during their childhood, all bets are off once the account terminates. That flexibility can be a massive benefit or a serious risk, depending entirely on the financial maturity of the young adult inheriting the money.

Figuring out the right vehicle for your family's legacy—whether it's a UGMA, UTMA, or something else entirely—is a complex decision. At Commons Capital, we specialize in building wealth management strategies that work for high-net-worth families. Let us help you match your gifting goals with the right financial tools.