The core difference between a bond fund and individual bonds boils down to a fundamental choice: do you want direct ownership and a predictable outcome, or pooled diversification with market-driven flexibility?

When you buy an individual bond, you're essentially making a direct loan to a government or corporation. In return, you receive regular, fixed interest payments over a set period. At the bond's maturity date, your original principal is returned to you (assuming the issuer doesn't default). Conversely, a bond fund is a professionally managed portfolio that holds hundreds or even thousands of different bonds. There is no maturity date for the fund itself, and its share price fluctuates daily, meaning there is no guarantee of principal return.

A High-Level Comparison of Bonds and Bond Funds

Weighing individual bonds vs. bond funds means choosing between the control of direct ownership and the convenience of pooled diversification.

With an individual bond, you are in complete control. You own a specific security and know the exact yield you will receive if you hold it to maturity. Barring an issuer default, your principal is safe. This direct ownership provides certainty over your future cash flows, making it an ideal tool for planning specific financial goals.

Bond funds offer a straightforward path to diversification. Instead of researching and purchasing dozens of individual bonds, you can buy shares in a fund that holds a vast, professionally managed portfolio. This is an efficient way to spread risk across various issuers, sectors, and maturities. However, this convenience comes at the cost of control and certainty. The fund's value, known as its Net Asset Value (NAV), changes daily with market fluctuations, and you have no say in the manager's buying or selling decisions.

The essential trade-off is this: Individual bonds provide a predictable income stream and a guaranteed return of principal at maturity. Bond funds offer broad diversification and easy trading but come with a constantly fluctuating value and no maturity guarantee.

To better understand these distinctions, let's compare them side-by-side.

Quick Comparison: Individual Bonds vs. Bond Funds

This table breaks down the fundamental differences between owning bonds directly and investing in a bond fund.

Ultimately, this table highlights the core dilemma: are you prioritizing the certainty and control of direct ownership, or the instant diversification and liquidity of a managed fund? Your answer will depend entirely on your specific financial objectives and risk tolerance.

How Each Investment Actually Works

To fully grasp the topic, we must look under the hood. The core difference between a bond fund and individual bonds is not just a matter of preference; it stems from their day-to-day operational mechanics. These mechanics are fundamentally different, leading to vastly different investor experiences.

An individual bond is one of the most straightforward financial instruments. It is a direct loan from you to an issuer. You purchase it at a price that could be at par (its face value), a discount (less than face value), or a premium (more than face value), depending primarily on prevailing interest rates.

From there, the key metric is its yield-to-maturity (YTM). Think of YTM as your total anticipated return — it includes all interest payments you'll receive plus the return of your principal if you hold the bond until it matures.

The Mechanics of an Individual Bond

What distinguishes an individual bond is its definitive end date. When you buy and hold, you are committing to a predictable journey with a clear destination.

- Fixed Payments: You receive consistent, typically semi-annual, coupon payments. This creates a reliable income stream.

- Principal Return: Upon maturity, the issuer is legally obligated to return your full principal. This is a cornerstone of any capital preservation strategy.

- Predictable Returns: As long as the issuer does not default, the YTM you locked in at purchase represents your total return. You can effectively ignore market noise.

This structure puts you in control with a high degree of certainty. A key part of success is knowing how to calculate bond yield, as this metric tells you exactly what to expect.

An individual bond operates like a fixed-term loan. You know exactly what you'll be paid, when you'll be paid, and when you'll get your money back. The mechanics are passive and defined from day one.

How a Bond Fund Operates

A bond fund, in contrast, is a dynamic, perpetual portfolio with no expiration date. Its value is tied to its Net Asset Value (NAV), which is the market price of all its underlying bonds, updated at the close of every trading day.

A fund manager is constantly working in the background, actively buying and selling bonds to adhere to the fund's mandate — such as maintaining a specific credit quality or an average portfolio duration. This continuous trading is a significant differentiator.

For example, a fund aiming for a 5-year average duration must constantly sell bonds nearing maturity (which shortens their duration) and replace them with new, longer-term bonds. This creates several critical realities for investors:

- Fluctuating NAV: Your principal is never guaranteed. The fund’s value rises and falls daily with interest rates, credit markets, and investor sentiment.

- Variable Income: The income distributions you receive can change. As the manager buys and sells bonds in different rate environments, the fund's yield shifts.

- No Maturity Date: There's no set date when you're promised your original investment back. To access your cash, you must sell your shares at the prevailing NAV.

Because of this, a bond fund behaves more like a stock than a simple loan. Its value reflects the market's real-time pricing of its entire portfolio, making it a vehicle for total return, not guaranteed principal repayment.

Comparing Risk And Return Profiles in the Real World

The practical difference between a bond fund and individual bonds becomes clear when you observe their behavior in actual market conditions. While both are fixed-income assets, their performance can diverge significantly depending on the economic climate and your investment horizon.

The most commonly discussed risk is interest rate risk. When market rates rise, the value of existing, lower-yielding bonds falls. For a bond fund, this impact is immediate, reflected as a drop in the fund's Net Asset Value (NAV). This means your principal is exposed to daily market whims.

For an individual bondholder, the situation is entirely different. While the bond's market price will also dip, this is largely irrelevant if you hold it to maturity. You will continue to collect your fixed coupon payments and are set to receive your full principal back on schedule. You are effectively insulated from this daily market volatility.

Credit Risk: The Concentration vs. Diversification Dilemma

Credit risk — the chance an issuer could default — highlights a fundamental trade-off. Even a well-constructed portfolio of 10-20 individual bonds carries concentrated exposure. A single default can significantly impact your overall return.

A bond fund, on the other hand, dramatically mitigates this risk through massive diversification. By owning hundreds or even thousands of bonds, a single default becomes a minor event, barely affecting the fund's total value.

This forces a critical decision for investors:

- Individual Bonds require due diligence on each issuer's financial stability but offer the potential for higher yields from specific credits you've personally vetted.

- Bond Funds provide a built-in safety net against any single company's failure, making them a simpler way to gain broad market exposure without becoming a credit analyst.

For affluent investors, the choice often depends on their willingness to conduct research. If you have the confidence to build a portfolio of high-quality issuers, individual bonds offer more control. If you value simplicity and risk diversification, a fund is the more direct path. As you develop your fixed-income strategy, you may find that it could be a great time for bonds.

Reinvestment Risk And Total Return Potential

Reinvestment risk is another key area of comparison. This is the uncertainty about where to invest your money when a bond matures or is called by the issuer. With a bond ladder, this risk is predictable. You know exactly when each bond comes due, allowing you to plan for reinvesting the principal at the prevailing market rates.

Bond funds are in a constant state of reinvestment. The manager is always buying and selling bonds to keep the fund aligned with its target duration and strategy. This constant activity exposes the entire portfolio to fluctuating interest rates, which affects both the fund's NAV and its income distributions.

While individual bonds offer a predictable return of principal, a bond fund’s total return is a combination of its fluctuating NAV and its income distributions. This makes funds a total return vehicle, not a capital preservation tool.

That is a crucial distinction. An individual bond is designed to return a specific amount of money on a specific date. A bond fund is designed to provide exposure to a segment of the bond market, and its success is measured by its total return over time.

To see how this plays out, let's examine how these two approaches handle risk differently.

Risk Profile Comparison: Individual Bonds vs. Bond Funds

This table shows there’s no single "safer" option — the risks are just different. The choice depends entirely on which risks you're more comfortable managing.

A striking 20-year analysis from April 2000 to April 2020 revealed how a bond fund could outperform. Starting with $100,000, a rolling 5-year Treasury bond ladder grew to $152,246, a 2.11% compound annual growth rate. In contrast, the VFITX Treasury fund grew to $178,278, a 2.93% CAGR. During that specific period of falling interest rates, the fund's ability to constantly reinvest in higher-yielding, longer-term bonds provided a significant performance advantage over the more rigid ladder strategy.

This history demonstrates that the "certainty" of individual bonds does not always lead to higher returns. In certain economic cycles, a professionally managed fund can adapt more nimbly to changing conditions and potentially deliver a better total return. It all comes down to your objective: a predictable outcome or the potential for higher, market-driven growth.

Analyzing Costs, Liquidity, and Diversification

When choosing between bond funds and individual bonds, the key differences emerge when you examine what impacts your bottom line: costs, liquidity, and the power of diversification.

These three factors not only shape your returns but also determine how quickly you can access your cash and how well your portfolio can withstand market shocks. Making the right choice here is critical.

Decoding the True Cost of Investing

The cost structures for individual bonds and bond funds are fundamentally different. For a bond fund, the cost is transparent: the expense ratio. This annual fee is easy to find and compare across different funds.

Individual bonds have costs embedded within the bid-ask spread. This is the gap between the price a dealer will pay for a bond (the bid) and the price they will sell it for (the ask). That spread represents the dealer’s profit and functions as a transaction fee for you. For retail investors making smaller trades, this spread can be surprisingly wide, sometimes consuming a significant portion of the bond's first-year yield.

The crucial takeaway on costs is this: A fund's expense ratio is a transparent, ongoing fee, while an individual bond's primary cost is a less visible, upfront transaction fee hidden in the bid-ask spread. For frequent traders or those investing smaller amounts, these spreads can make individual bonds a more expensive option than they appear.

Navigating Liquidity: The Ease of Cashing Out

Liquidity refers to how quickly you can convert an investment into cash without a significant price reduction. In this regard, bond funds have a clear and substantial advantage.

Cashing out of a bond fund is simple. You can sell your shares on any business day and receive the fund’s closing Net Asset Value (NAV). The process is predictable and market-priced, making bond funds an excellent tool if you need ready access to your capital.

Selling a single bond before maturity can be challenging. You must find a buyer on the secondary market, which can be difficult for less common municipal or corporate bonds. This often results in wider bid-ask spreads, and you might have to sell at an unfavorable price, especially if you need cash quickly. For many investors, this difference is a major consideration.

The Power of Diversification in Managing Risk

This is perhaps the most significant differentiator. Building a truly diversified portfolio with individual bonds is expensive and labor-intensive. Even with a portfolio of 10-20 bonds, you remain highly exposed to credit risk. If just one of those issuers defaults, it can create a substantial hole in your returns.

Bond funds solve this problem instantly. With a single purchase, you are invested in hundreds, sometimes thousands, of different bonds. Your risk is spread across a vast range of issuers, industries, and maturities. Understanding these broader strategies on how to diversify an investment portfolio is key to smart risk management.

Market data confirms this advantage. Bond funds, which often track major indices like the Bloomberg US Aggregate Bond Index, spread risk over thousands of securities. In a small portfolio of 10-24 individual bonds, a single default can wipe out 4-10% of your holdings. According to Moody's historical data, investment-grade defaults averaged just 0.13% per year from 1970-2024. However, during a crisis like 2008, when that rate spiked to 1.2%, a concentrated portfolio could have easily suffered a painful 5-10% loss. The same data highlights the cost advantage: retail bid-ask spreads on corporate bonds often run 50-100 basis points, while large funds can negotiate these down to just 5-10 basis points. In a fund, one default is merely a rounding error — a powerful shield against credit events.

Navigating Tax Implications for Your Portfolio

When you’re weighing the difference between a bond fund and individual bonds, tax implications are a critical factor. The tax treatment for each investment is fundamentally different, which can significantly impact your net returns. Managing these tax implications can be as important as the investment choice itself.

With an individual bond, the tax situation is relatively straightforward. The interest income you receive is generally taxed as ordinary income at your marginal rate. More importantly, you have complete control over when to realize capital gains or losses because you decide if and when to sell the bond before it matures. This provides a powerful tool for strategic tax planning.

The Complexity of Bond Fund Distributions

Bond funds operate in a more complex tax environment. Instead of receiving simple interest payments, fund investors receive distributions that are often a combination of different income types, each with its own tax treatment.

These distributions can include:

- Ordinary Income: From the coupon payments of the bonds within the fund.

- Short-Term Capital Gains: From bonds the fund manager sold at a profit after holding them for one year or less.

- Long-Term Capital Gains: From profitable bond sales where the holding period was over one year.

This mix not only complicates your tax reporting but also often leads to a less predictable tax bill compared to holding an individual bond.

Understanding Phantom Income and Tax Control

One of the most significant tax challenges with bond funds is the potential for "phantom income." This occurs when the fund manager sells bonds within the portfolio at a profit, generating capital gains. By law, these gains must be distributed to shareholders, creating a taxable event for you — even if you never sold a single share of the fund. This can be a frustrating scenario where your fund's value may decline, yet you still owe taxes on its internal trading activity.

For affluent investors, the lack of tax control in a bond fund can be a major issue. You are essentially a passenger, subject to the tax consequences of the fund manager's trading decisions, which may not align with your personal financial strategy.

In contrast, owning individual bonds puts you firmly in control. You decide when to realize a gain or a loss. This control is invaluable for strategies like tax-loss harvesting, where you sell underperforming bonds to realize a loss that can offset gains elsewhere in your portfolio. This level of precise tax management is impossible with a bond fund. For investors looking to optimize their fixed-income holdings, understanding the tax advantages of specific bond types is crucial. You can explore this further in our guide on whether municipal bonds are a good investment.

Ultimately, it comes down to a trade-off. Bond funds offer simplicity and instant diversification, but at the cost of tax efficiency and control. Individual bonds require more hands-on management but reward you with superior control over your tax outcomes, enabling more sophisticated wealth management strategies.

How to Choose the Right Strategy for Your Goals

Deciding between individual bonds and bond funds depends on your financial objectives. The question is not which is universally "better," but which tool is right for the specific job. The core difference between a bond fund and individual bonds becomes clear once you define your primary goal.

There is no one-size-fits-all answer. Your choice should be driven by whether you need predictability or flexibility. Are you funding a specific future expense, or are you diversifying a larger portfolio? Your answer will guide you to the right strategy.

When Individual Bonds Are the Superior Choice

Individual bonds are ideal when your goal is certainty. If you need a predictable stream of income to meet specific, date-driven liabilities, building a bond ladder is almost always the most effective approach.

Consider these common scenarios:

- Funding Retirement Income: You can structure a ladder of bonds to mature sequentially, providing a known amount of cash flow each year to cover living expenses.

- Paying for Education: If you have tuition payments due in five, six, and seven years, you can buy bonds that mature in those exact years, ensuring the principal is available when the bills are due.

- A Planned Major Purchase: Planning a down payment on a second home in three years? A single bond maturing at that time locks in both your principal and your yield, removing market risk from that specific goal.

Individual bonds are purpose-built for liability matching. Their fixed maturity dates and predictable cash flows allow you to align your assets precisely with future financial obligations, offering a level of control that funds simply cannot replicate.

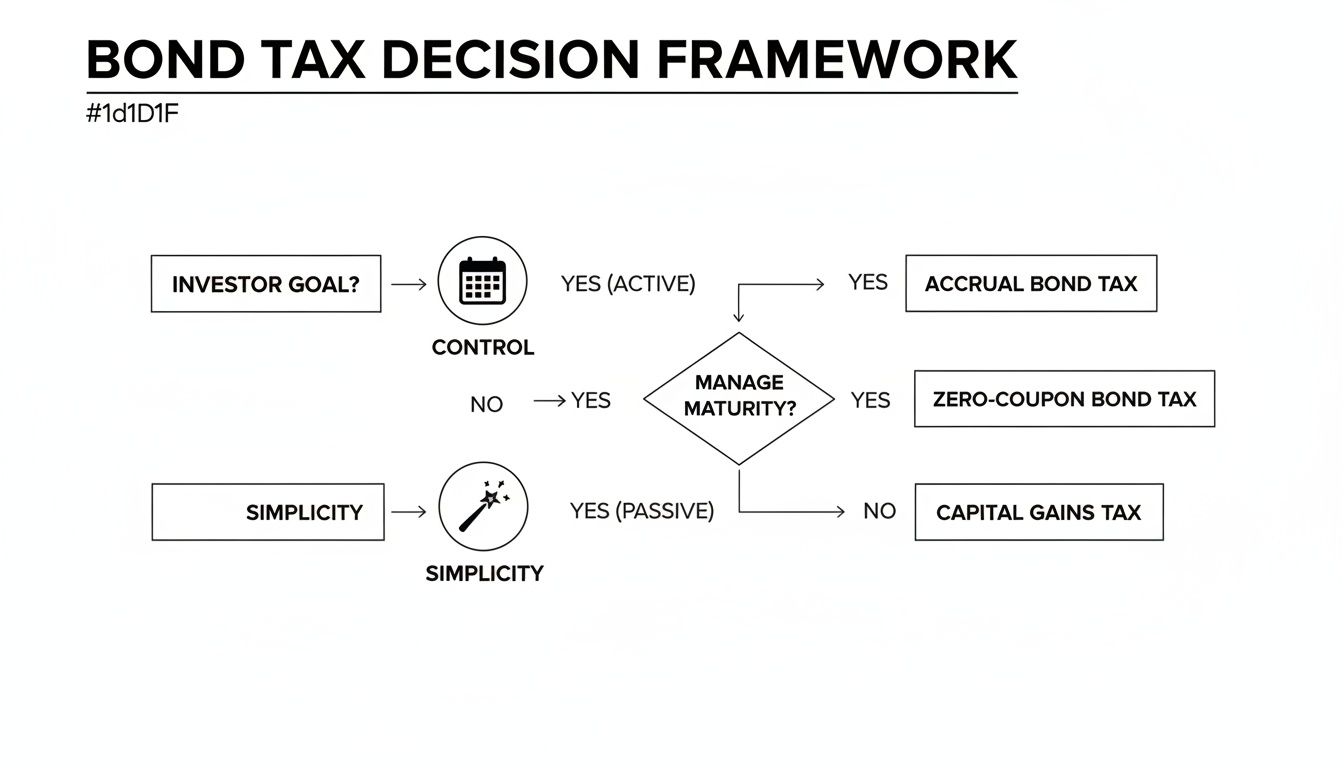

This decision-making process — whether your priority is control or simplicity — is illustrated well in this visual.

As the flowchart shows, investors who prioritize controlling maturity dates and tax events are better served by individual bonds. Those seeking ease of use will naturally gravitate toward funds.

When a Bond Fund Is the Logical Option

Bond funds are the ideal tool when your objective is broad diversification and liquidity within a larger, growth-oriented portfolio. They are not designed for funding specific future expenses but for gaining efficient exposure to the entire fixed-income market as an asset class.

A bond fund makes more sense when:

- You are building a diversified portfolio and want a simple way to allocate a percentage to fixed income.

- Your goal is total return from the bond market, and you are comfortable with daily fluctuations in the fund's principal value (its NAV).

- You prioritize the ability to buy and sell your holdings quickly, without worrying about the bid-ask spreads associated with individual bonds.

Interestingly, a comprehensive study comparing rolling bond ladders to bond index funds found that ladders can slightly outperform funds by up to 8 basis points a year over long periods. This small advantage comes from locking in yields without the constant duration changes that expose funds to reinvestment risk. For high-net-worth investors, a custom bond ladder proved far more effective at protecting principal during the Fed's aggressive rate hikes after 2022. You can read the full research about these performance findings for a deeper dive.

A Hybrid Approach for Sophisticated Investors

For many affluent households, the best solution is not an either-or choice but a hybrid model.

This strategy involves using a core holding of individual bonds to secure baseline income needs. This core is then complemented with specialized bond funds to target specific market opportunities or sectors, such as high-yield corporates or international debt. This approach can provide the best of both worlds: stability and predictability where it counts most, plus diversified growth potential.

A Few Common Questions

When exploring fixed-income investments, a few key questions consistently arise. Clear answers to these help in building a portfolio that aligns with your goals. Let's address some of the most frequent questions we hear from investors weighing the difference between a bond fund and individual bonds.

Can a Bond Fund Lose Principal Value?

Yes, absolutely. This is one of the most critical distinctions to understand. A bond fund can definitely lose principal value.

When you buy an individual bond and hold it to maturity, you know precisely what you will get back — the bond's full face value (assuming the issuer doesn't default). It is a predictable, scheduled return of your initial investment.

A bond fund operates differently. It never "matures." Its share price, the Net Asset Value (NAV), fluctuates daily with the market. If interest rates rise, the value of the older, lower-yielding bonds in the fund decreases, pushing the fund's NAV down. Your principal is directly exposed to market risk, which means you can lose money.

Which Is Better for Retirement Income?

The "better" choice depends on your objective. Are you trying to cover specific, known expenses, or are you aiming for overall portfolio growth and diversification?

- For Predictable Income: Building a bond ladder with individual bonds is hard to beat. You can schedule bonds to mature and provide cash exactly when you need it for major expenses, creating a reliable, known income stream.

- For Total Return and Diversification: A bond fund is typically the more efficient tool if you simply want broad exposure to the bond market as part of your asset allocation. It's simple, instantly diversified, and a great fit for the growth-focused portion of a retirement portfolio.

In practice, many retirees use a hybrid approach. They may use an individual bond ladder to cover essential living costs and then use bond funds for other goals like liquidity, growth, and diversification.

How Many Individual Bonds Are Needed for Proper Diversification?

There is no magic number, but most financial professionals suggest a minimum of 10 to 20 individual bonds. These should be from different issuers, in different industries, and with varying credit quality to achieve a basic level of diversification. However, it's crucial to understand the limitations.

Even with 20 different bonds, your portfolio remains highly concentrated compared to a bond fund that may hold hundreds or thousands of securities. If one issuer defaults in your 20-bond portfolio, you could lose 5% of your principal instantly. In a large fund, the same default would be a minor event.

Building a truly diversified portfolio of individual bonds — one that can genuinely absorb a default or two — takes a lot of capital, a ton of research, and constant monitoring. That reality really highlights the built-in risk management you get with a bond fund.

Ultimately, you are making a trade-off. You can have the control and predictability of individual bonds, or you can have the simplified, massive diversification that comes with a fund.

Figuring out the right fixed-income strategy requires a clear-eyed look at how these tools fit into your unique financial picture. At Commons Capital, we build custom fixed-income solutions for high-net-worth individuals and families, making sure every part of your portfolio is working toward your specific goals for income, growth, and capital preservation. To see how we can help you build a more resilient financial future, visit us at https://www.commonsllc.com.